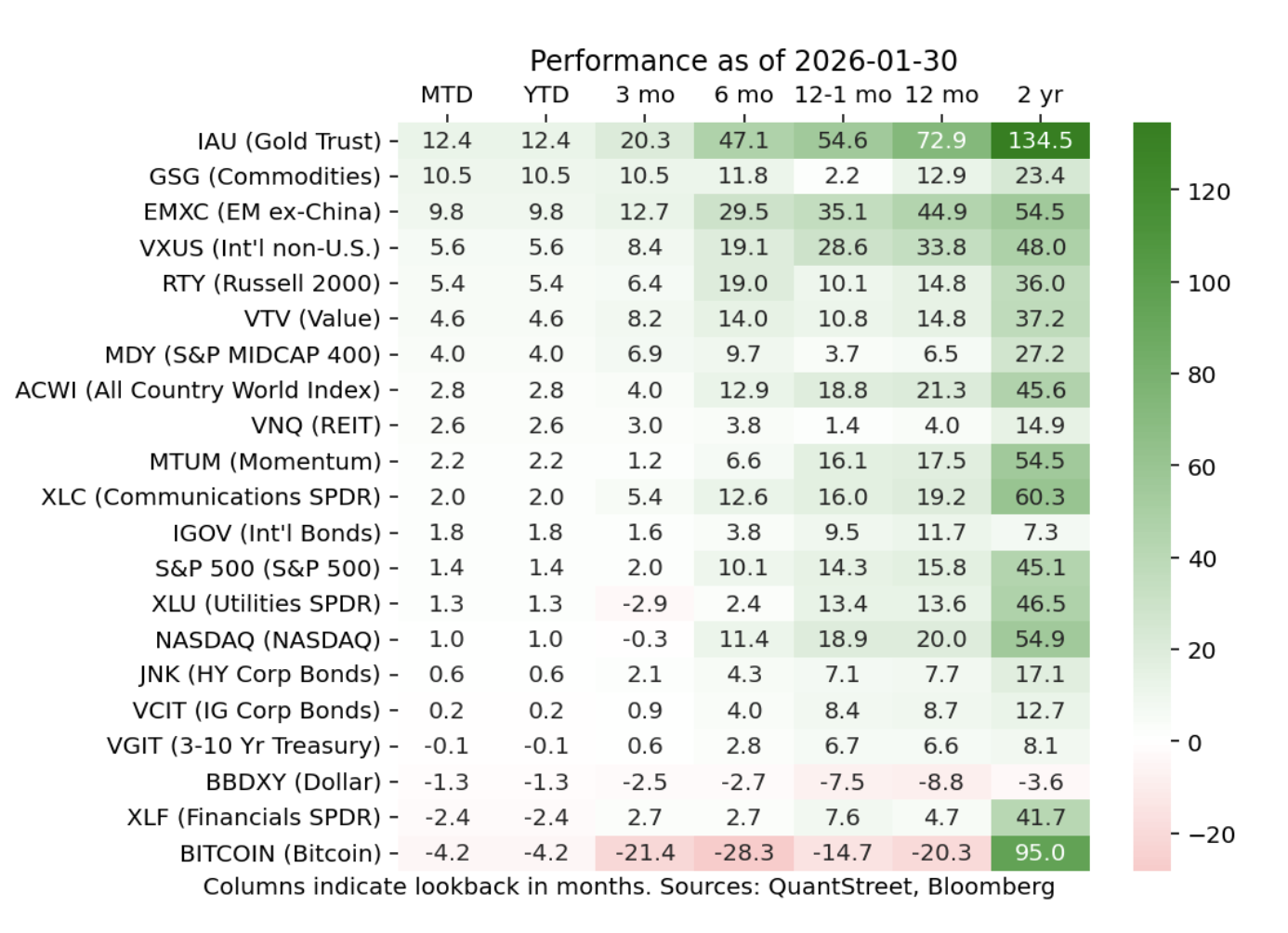

Our recent piece on the dollar neatly lays out much of what drove price action in January of 2026. Despite a disastrous last trading day in the month, gold carried its 2025 rally into 2026, and finished the month up over 12%. The dollar finished the month down 1.3% for a litany of reasons, including our progressively nastier spat with Canada and the Trump administration's insistence on liberating Greenland. Though cooler heads have prevailed with regard to the latter (at least for the time being), each episode of the usual DJT news cycle--President Trump making extreme claims, followed by everyone else freaking out, followed by his backing down and ultimately coming to a reasonable resolution--leaves the dollar a little bit weaker than it was before.

This is all well-summarized in a recent Financial Times article which argues that:

"The Greenland crisis has reignited concerns about the political risks of US assets — for a long time a safe harbour for global capital — that helped drive a 9 per cent decline in the US dollar last year in its steepest drop since 2017."

We agree. Our guess is that this will continue for the remainder of President Trump's second term, and whoever occupies the White House next will have a heck of a time restoring global trust in the dollar as an unquestioned store of value. Our second guess is the gold narrative as a refuge from all of this will also continue to build, alongside continued gold appreciation (Friday's ugly price action notwithstanding).

Looking across other asset classes, international led the way with small-caps (RTY) and midcaps (MDY) also catching a bid. Financials were weak on the back of the Trump administration's threat to cap credit card interest rates at 10%. The banking industry was less than excited about the proposal, and with some justification, argued that price caps on credit provision would restrict access to credit by making loans available only to the most creditworthy borrowers and pushing others into more costly credit instruments. Bitcoin continued is descent to earth--sub 80,000 at the time of this writing--and appears to have been overtaken (for the moment) by gold as the asset of choice for those not fond of the greenback.

Our pivot towards more international exposure at the start of January proved well timed, though as we mentioned last month, we still maintained a slight US overweight relative to target-date fund allocations. Given last month's price action, we wish we had gone all in on international, but no one has a crystal ball. As of this month, the US overweight disappears, and for the first time in our history as a firm, we are overweight international assets relative to benchmarks. This is not because we are bearish on US stocks--we are definitely not--but the dollar headwind will be a lot to overcome. You can see details of our performance here.

As an aside, we will write more about where these "benchmarks" come from soon on our Substack (please sign up if you haven't already). For those who don't want to wait, but need to know right now how one can use target-date funds to extract the "wisdom of Wall Street," you can check out our white paper on the topic here. It is not for the faint of heart.