Local Markets Shine in a Solid Quarter for EM Debt

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAs global rate pressures ease and fundamentals strengthen across key economies, conditions appear increasingly favorable for EM local bonds and currencies. The team remains constructive on select opportunities—from duration exposure in Hungary, India, and Malaysia to currency overweights in the Philippines and Brazil—while maintaining a disciplined stance in markets facing fiscal or political uncertainty such as Poland and Romania.

A Solid Quarter

As we discussed in our previous blog post, emerging markets debt continued to deliver in the third quarter of 2025, supported by resilient fundamentals and steady investor demand.

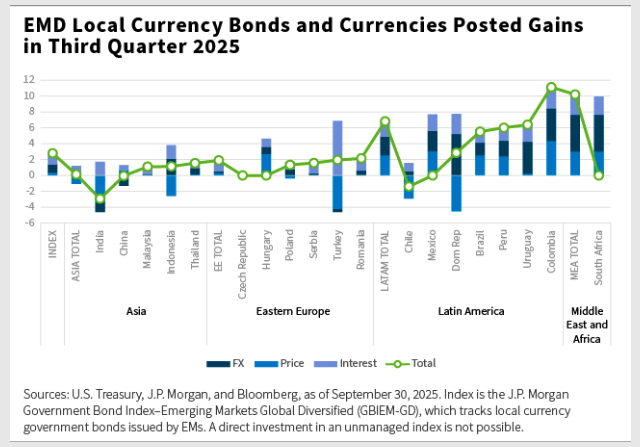

The J.P. Morgan Government Bond Index-Emerging Markets Global Diversified (GBI-EM Global Diversified) returned 2.80%, of which 0.37% resulted from EM currency appreciation against the U.S. dollar. Bonds also performed well, gaining 1.0% in price terms with yields declining by an average of 9 basis points (bps) across the index.

By region, Africa (+10.21%) and Latin America (+6.83%) performed strongly over the quarter, while Asia (+0.13%) and Europe (+1.89%) lagged.

Largest Active Positions

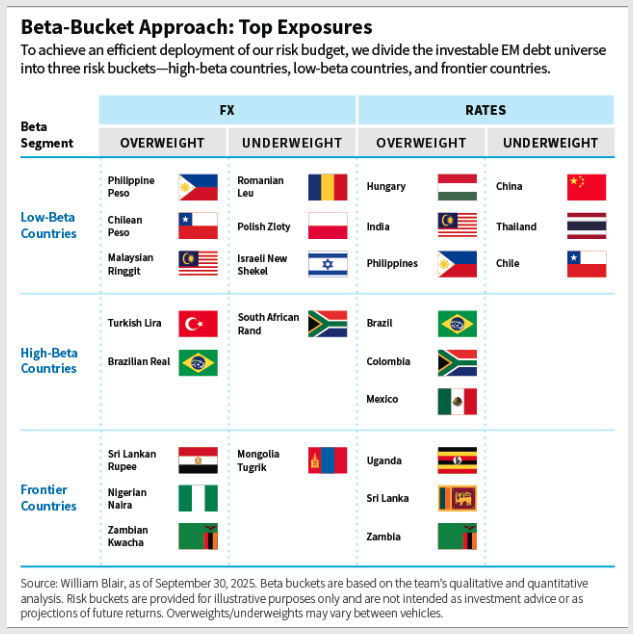

Below, we break down some of our largest active positions by beta bucket, which is how we allocate our risk budget.

Low-Beta Bucket

Within the low-beta segment, positioning remains focused on markets offering attractive real yields, credible policy frameworks, and manageable fiscal dynamics. The team optimistically views duration exposure in countries such as Hungary, India, and Malaysia, where disinflation trends and proactive central banks create scope for easing. Currency exposure is concentrated in markets with improving external balances, including the Philippines and Malaysia, while we remain cautious toward economies facing election-driven fiscal risk or overvalued exchange rates, such as Romania and Poland.

Hungary: Our overweight in duration was concentrated largely in the green bond. Real rates are attractive, in our opinion, and although they are now closer to the terminal rate, the central bank has been one of the most progressive in the region. A renewed European focus on meeting excessive deficit targets may help moderate the size of the fiscal deficit in the coming period despite the wider acceptance that Europe needs to raise defense spending. As we get close to next year’s election, an increased focus will be placed on who the market expects to win.

India: We are overweight Indian duration as we expect India’s services exports, remittances, foreign direct investment (FDI), and portfolio flows to support India’s balance of payments. Low inflation should enable the central bank to maintain favorable liquidity conditions throughout the year.

Philippines: We are overweight the Philippine peso as lower oil prices this year are likely to improve the country’s terms of trade. Remittance growth has been strong, and lower inflation has allowed the central bank to lower policy rates to support economic growth.

Chile: In Chile, we have maintained our underweight to the local curve in favor of higher-yielding regional peers. While Chile underperformed the benchmark over the past quarter, we expect peso performance to improve on higher copper prices as global supply shocks drive the market higher.

Malaysia: In Malaysia, we remain overweight the ringgit. Economic growth remains resilient, supported by private consumption. Fiscal consolation efforts are ongoing. The currency outperformed last year but remains inexpensive on a trade-weighted basis. We are overweight Malaysia duration as inflation is benign, and the central bank has room to ease policy rates should trade uncertainty spill over to dampen Malaysia’s economic growth.

Romania: In Romania, we hold an underweight position in the leu, as we have concerns about the twin deficits, particularly during an election cycle. We are awaiting a rerun of the presidential election this year, and the coalition has not delivered on a strong fiscal consolidation plan. The currency is also overvalued, in our opinion, and contributes to a lack of competitiveness in the region and a large current account deficit.

Poland: In Poland, we are underweight the zloty on valuations and expectations of some reversal of the strength we saw in 2024. At the same time, we are underweight rates on the back of a less supportive political outlook for fiscal consolidation.

Israel: The Israeli shekel has been strong in recent months in spite of elevated geopolitical risks; however, we believe there is likely to be less appetite for a significantly stronger shekel from current levels.

Thailand: We are underweight Thailand duration because valuations are unappealing. Rate cuts are already priced in, but financial stability concerns may lead to fewer central bank cuts than are currently priced in.

China: We are underweight the Chinese renminbi on uncertainty over U.S. tariffs and trade measures imposed on China. While the central bank has fixed the currency to lower volatility, the renminbi has weakened on a trade-weighted basis.

High-Beta Bucket

In higher-beta markets, positioning reflects a balance between attractive carry opportunities and sensitivity to shifting policy and political dynamics. We remain constructive on Brazil, where high real rates and credible policy settings continue to attract inflows, and maintain exposure to local bonds in Colombia and Mexico as inflation expectations stay anchored. In Turkey, disciplined monetary tightening has reinforced confidence in the reform trajectory despite persistent volatility, while in South Africa, we have adopted a more neutral stance following an oversold period in local rates.

Brazil: In Brazil, local assets have continued to outperform. With nominal policy rates peaking at 15% and with one-year-ahead consensus inflation edging down to 4.3%, Brazil has the second-highest real interest rate in the benchmark index after Turkey, which has supported portfolio flows into the country. Growth is also holding up well this year, while expectations for 2026 have slipped in recent months. Lower U.S. Federal Reserve (Fed) rates should give the central bank more scope to cut next year, which should help anchor expectations.

Colombia: We closed our overweight to the Colombian peso with valuations appearing stretched given a challenging macro backdrop. We have further increased exposure to local bonds, however, as the curve is steep and inflation expectations remain well anchored.

Mexico: Mexico outperformed the benchmark index over the quarter in both FX and rates, but we are growing increasingly concerned about deterioration in the growth outlook driven by the manufacturing sector and private consumption generally, with remittances from the U.S. falling. However, rate cuts, well-anchored inflation expectations, and slowing growth should support bonds in the coming months. We also hold an overweight position in Pemex bonds as the government increases direct support for the company, which should lead to narrower spreads to the sovereign.

Turkey: In Turkey, although political volatility has increased, the economic reform path remains intact, allowing for strong performance in many economic indicators, such as current account and FX reserve levels. We believe investors continue to be overcompensated by high yields, which we believe will not be fully eroded by currency depreciation. Investors may also take a closer look at local bonds, as the central bank raised rates in an emergency meeting to help fight currency flight.

South Africa: In South Africa, we moved to a more neutral position in rates as the sell-off related to the budget delay was overdone, in our opinion. Now that the budget has been passed, we expect a flattening of the curve, with the long end best-positioned to benefit from the rally on relative valuation; however, the scope for further compression is limited by the recent strong performance.

Frontier Bucket

In frontier markets, positioning remains guided by improving macro fundamentals and attractive real yields. We continue to optimistically view markets where reform momentum and external balances support currency stability—most notably Uganda and Sri Lanka—while maintaining exposure to Zambia, where disinflation and credible monetary policy create scope for further curve compression. In contrast, we remain cautious on commodity-dependent economies such as Mongolia, where weaker export prices and fiscal pressures may weigh on performance.

Uganda: We remain constructive on Uganda local currency assets, and the relatively mature local currency market allows us to express this view in longer-dated bonds. We hold a long bond position on attractive real rates. We removed our partial hedge of the currency risk, as we became more comfortable with the fundamental support to the exchange rate.

Sri Lanka: In Sri Lanka, strong remittances and resumption of FDI balances out U.S. dollar demand from the central bank to rebuild foreign exchange (FX) reserves and narrowing the current account surplus on increasing import needs. The combination of the above supports a stable outlook for the rupee, which offers attractive carry return.

Zambia: We maintain our long position in Zambian bonds given the scope for further disinflation in 2025 to support the performance. While the central bank is likely to remain hawkish in light of short-term risks from, among other things, the global backdrop, we see potential scope for the local currency yield curve to bull steepen.

Nigeria: In Nigeria, the disinflation process appears to be firmly in place, and we believe the authorities have done a good job in improving the potential for economic stability. Transparency in the local FX market has improved and there remains a strong capital flow of international money into the local Nigerian market to support the appreciation trend.

Mongolia: In Mongolia, we hold an underweight position in the Mongolian tugrik, as lower coal prices are likely to impact the country’s commodity export proceeds this year. Mongolia relies on commodity exports, and declining commodity prices should exert pressure on the country’s fiscal and external balances. Despite government and central bank efforts to stabilize the currency, the tugrik may still need further depreciation due to its rich valuation and the anticipated weaker terms of trade this year.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Lewis Jones, CFA, FRM, is a portfolio manager on William Blair’s emerging markets debt team.

Want more insights on the economy and investment landscape? Subscribe to our blog.

This content is for informational and educational purposes only and not intended as investment advice or a recommendation to buy or sell any security. Investment advice and recommendations can be provided only after careful consideration of an investor’s objectives, guidelines, and restrictions.

Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within William Blair Investment Management, LLC, or affiliates. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented.

Investing involves risks, including the possible loss of principal. Equity securities may decline in value due to both real and perceived general market, economic, and industry conditions. The securities of smaller companies may be more volatile and less liquid than securities of larger companies. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks. These risks may be enhanced in emerging markets and frontier markets. Different investment styles may shift in and out of favor depending on market conditions. Individual securities may not perform as expected or a strategy used by the Adviser may fail to produce its intended result.

Investing in the bond market is subject to certain risks including market, interest rate, issuer, credit, and inflation risk. Rising interest rates generally cause bond prices to fall. High-yield, lower-rated, securities involve greater risk than higher-rated securities. Sovereign debt securities are subject to the risk that an entity may delay or refuse to pay interest or principal on its sovereign debt because of cash flow problems, insufficient foreign reserves, or political or other considerations. Derivatives may involve certain risks such as counterparty, liquidity, interest rate, market, credit, management, and the risk that a position could not be closed when most advantageous. Diversification does not ensure against loss. The inclusion of Environmental, Social and Governance (ESG) factors beyond traditional financial information in the selection of securities could result in a strategy's performance deviating from other strategies or benchmarks, depending on whether such factors are in or out of favor. ESG analysis may rely on certain values based criteria to eliminate exposures found in similar strategies or benchmarks, which could result in performance deviating.

Collective Investment Trusts (CITs) are available to qualified retirement plans. For non-U.S. citizens or residents, William Blair offers a series of Luxembourg-domiciled SICAV products.

There can be no assurance that investment objectives will be met. Any investment or strategy mentioned herein may not be appropriate for every investor. References to specific companies are for illustrative purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future returns.

Privacy & Security | Cookie Policy | Social Media Disclaimer | FINRA’s BrokerCheck | Glossary

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All