Inflation and Real Yields: The Key to Treasury Duration Decisions

One of the most fundamental decisions facing fixed-income investors is determining the optimal maturity for their Treasury holdings. Should you stay in short-term Treasury bills, or extend duration by moving further out the yield curve to 2-year and 10-year notes? Data on real returns across different Treasury maturities provides crucial insights into when each strategy makes sense.

The Historical Case for Duration: Normal Yield Curves Reward Risk

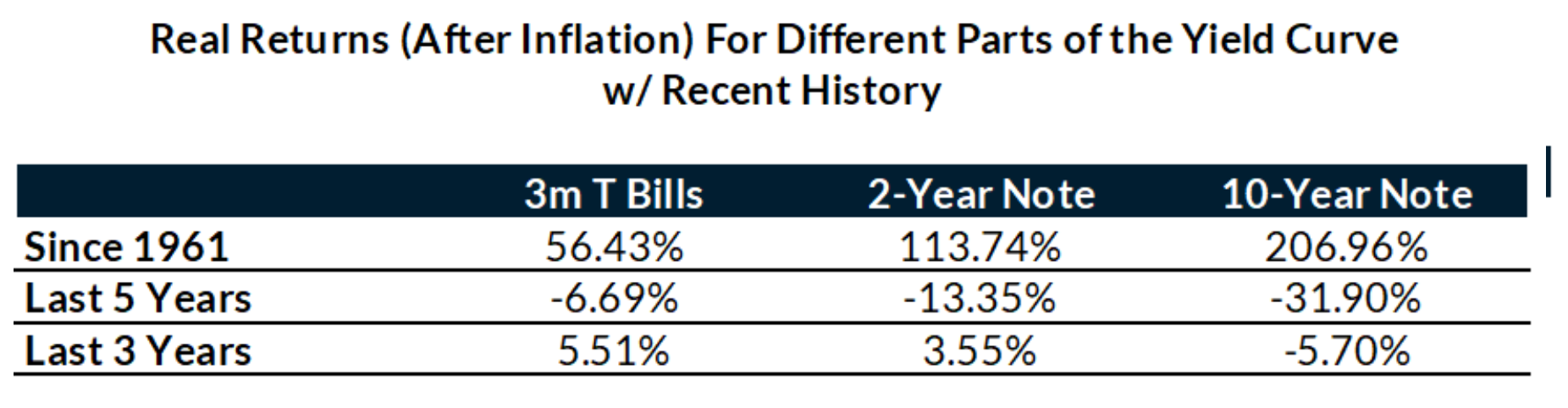

Over long periods, the mathematics of fixed-income investing support a clear principle: longer-dated maturities typically offer higher yields, carry greater risk, and deliver superior real returns. Since 1961, this relationship has held remarkably consistent. Ten-year Treasury notes have generated 206.96% cumulative real returns compared to 113.74% for 2-year notes and just 56.43% for 3-month Treasury bills.

Source: Bloomberg as of September 16, 2025

This performance differential translates to meaningful annual real returns: 10-year notes averaging 2.00% after inflation, 2-year notes at 1.29%, and 3-month bills at a modest 0.65%. The message seems clear: duration risk has historically been compensated with higher real returns, making the case for extending maturity when yield curves maintain their normal upward slope.

When the Rules Don’t Apply: Recent Outperformance of Cash

However, this conventional wisdom hasn’t held in recent years. Treasury bills have dramatically outperformed longer-duration securities over both the last three and five-year periods. Over the past three years, 3-month bills delivered 5.51% real returns while 10-year notes posted -5.70%. Even more striking, bills have been the only segment to generate positive real returns over the last five years at -6.69%, compared to devastating losses of -13.35% for 2-year notes and -31.90% for 10-year notes.

Source: Bloomberg as of September 16, 2025

This reversal explains why many investors have crowded into Treasury bills and money market funds, abandoning the traditional duration strategy that has worked for decades. The recent period demonstrates that when yield curves invert and monetary policy becomes aggressive, the conventional risk-return relationship can break down entirely.

Real Yields: The Compass for Duration Decisions

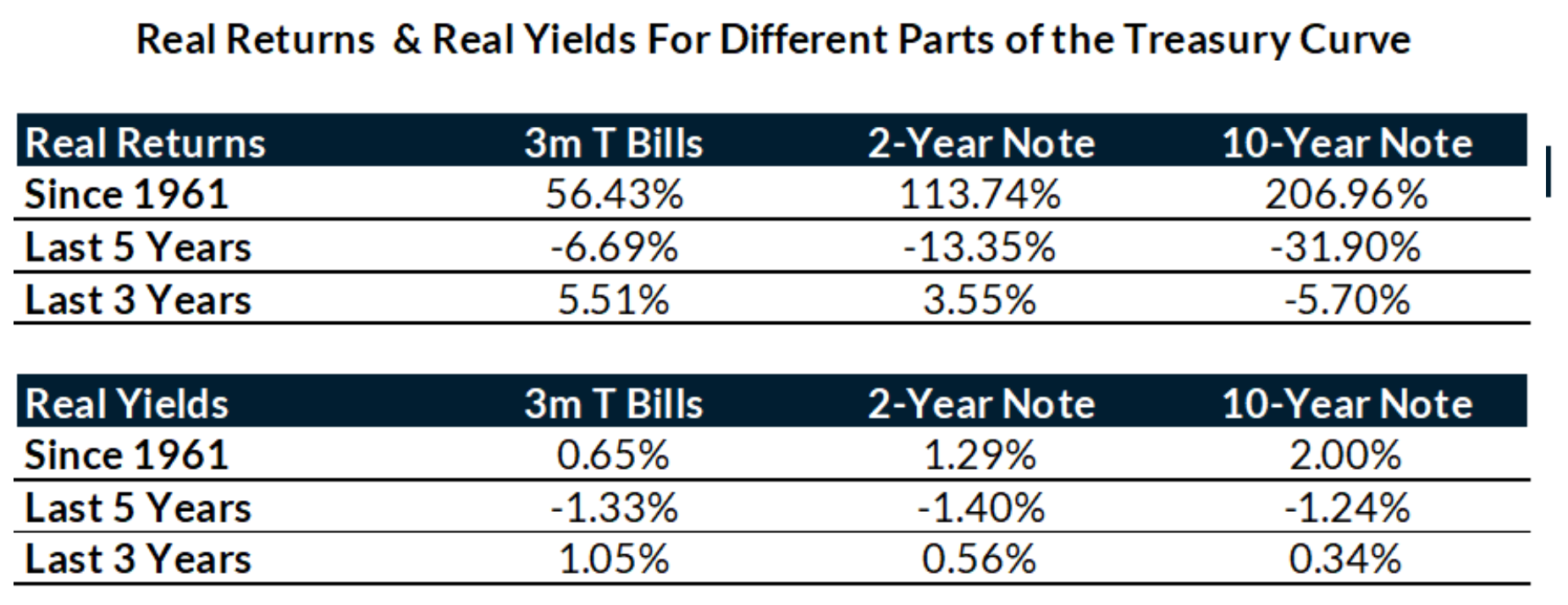

The key to understanding when to favor cash versus duration lies in analyzing real yields, the inflation-adjusted yields available today. Historically, real yields have followed the expected pattern: 0.65% for 3-month bills, 1.29% for 2-year notes, and 2.00% for 10-year notes since 1961. This normal real yield curve structure has corresponded directly with the superior historical real returns of longer-duration securities.

Source: Bloomberg as of September 16, 2025

However, yield curve inversions at the short end have fundamentally altered this dynamic. Over the past three years, real yields have actually been highest for 3-month bills at 1.05%, declining to 0.56% for 2-year notes and just 0.34% for 10-year notes. This inverted real yield structure has driven the superior performance of Treasury bills, as higher real yields translate directly into better real returns.

Takeaway: when real yields are higher for shorter maturities due to yield curve inversion, the traditional case for extending duration disappears. Investors are being compensated more for staying short than for taking duration risk.

Inflation: The Primary Driver of Treasury Bill Returns

Inflation emerges as the dominant factor determining Treasury bill real returns. The relationship is straightforward but crucial: real returns are positive (0.45%) when Treasury bill rates exceed inflation, and negative (-0.11%) when rates fall below inflation levels.

Source: Bloomberg as of September 16, 2025

This dynamic explains why Treasury bills performed so poorly during the high-inflation period of recent years when nominal rates lagged inflation, and why they’ve recovered as real yields have turned positive. For Treasury bill investors, monitoring inflation expectations and the Federal Reserve’s response becomes paramount. When central bank policy keeps nominal rates below inflation, Treasury bills will deliver negative real returns regardless of other market conditions.

Yield Curve Shape: A Secondary but Notable Factor

While inflation dominates Treasury bill returns, the shape of the short end of the yield curve provides additional insight. Treasury bill real returns average 0.11% when 2-year yields exceed 3-month rates (normal curve) but only 0.05% when the curve is flat or inverted at the short end.

Source: Bloomberg as of September 16, 2025

This difference reflects market expectations about future rate policy. When 2-year yields are higher than Treasury bill rates, the market is signaling expectations for rising short-term rates, which benefits Treasury bill holders through reinvestment at higher rates. Conversely, when the curve is flat or inverted, markets expect future Treasury bill rates to decline, reducing the reinvestment advantage.

However, this yield curve effect is notably modest, just 6 basis points difference in annual real returns, making it a secondary consideration compared to the inflation relationship.

The Short-End of the Curve Tells You Nothing About Moving to Two Years

Interestingly, the data reveals that the shape of the short end of the curve provides virtually no guidance about whether to extend from Treasury bills to 2-year notes. Two-year note real returns are nearly identical whether 2-year yields are above (0.11%) or below (0.10%) 3-month Treasury bill rates.

Source: Bloomberg as of September 16, 2025

This finding challenges conventional wisdom about riding the yield curve and suggests that decisions about extending from 3-month bills to 2-year notes should be based on other factors, such as the absolute level of real yields available and broader portfolio considerations rather than curve positioning.

The Two-Factor Framework for Duration Decisions

The evidence points to a straightforward framework for Treasury duration decisions based on two primary factors:

Primary Factor – Inflation Relationship: When Treasury bill real yields are positive, favor short-term positioning. When real yields turn negative, consider extending duration to capture potentially higher real yields available in longer maturities.

Secondary Factor – Yield Curve Shape: Normal upward-sloping yield curves provide modest additional support for Treasury bill positions, while flat or inverted curves slightly favor duration extension, though this effect is minimal.

This framework explains both the historical outperformance of longer-duration Treasuries during normal economic periods and the recent success of Treasury bill strategies during yield curve inversions and high inflation. By focusing on these two factors, with inflation dynamics taking precedence, investors can make more informed decisions about when to stay short versus when to move out the curve.

Current Environment and Strategic Implications

Today’s environment provides a clear example of how these principles apply in practice. With positive real yields of approximately 1.23% available on Treasury bills, the inflation factor strongly favors staying at the short-end of the curve. Should 2-year yields move above Treasury bill yields, creating a normal curve slope, that would provide additional, though secondary, support for the Treasury bill position.

However, should the Federal Reserve push Treasury bill rates back into negative real yield territory, a scenario that could emerge if inflation re-accelerates while the Fed maintains accommodative policy, investors should seriously consider moving further out the yield curve where real yields might remain positive.

Originally published by Modelist

For more news, information, and strategy, visit the ETF Strategist Content Hub.

Make the most of these insights using Modelist. We create customized investment models for the fiduciary financial advisor. Get in touch with us at [email protected] for a personal consultation.

Modelist Inc. is a registered investment advisor. Registration with a regulatory authority does not imply a certain level of skill or training.

The information contained in this material is for educational and informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation of any security, investment, or investment strategy. All investments involve risks, including interest rate risks, inflation risks, and the risk of loss of principal, and are not guaranteed. Past performance is not indicative of future results.

Modelist Inc. believes, to the best of its knowledge, that this material does not contain any false or materially misleading statements or omit material facts.

This material includes information obtained from third-party sources. Modelist Inc. does not guarantee the accuracy, reliability, or completeness of such information and disclaims any liability for errors or omissions arising from its use. Returns cited are based on publicly available Treasury market data and may not reflect actual investment outcomes, fees, or expenses.

Each investor’s situation is unique; please consult with a professional financial advisor, tax accountant, or legal representative, as applicable, to develop an individualized plan or address any questions you may have.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Modelist

More Fiduciary Rules Topics >