Growth investors may be feeling the ground shifting beneath them. Traditional factor analysis shows quality and growth still lagging value—an apparent paradox when global growth itself is strengthening. Yet a closer look at what drives the so-called “value” factor reveals how today’s economic revival is rewarding a different kind of growth.

The Quarter in Review

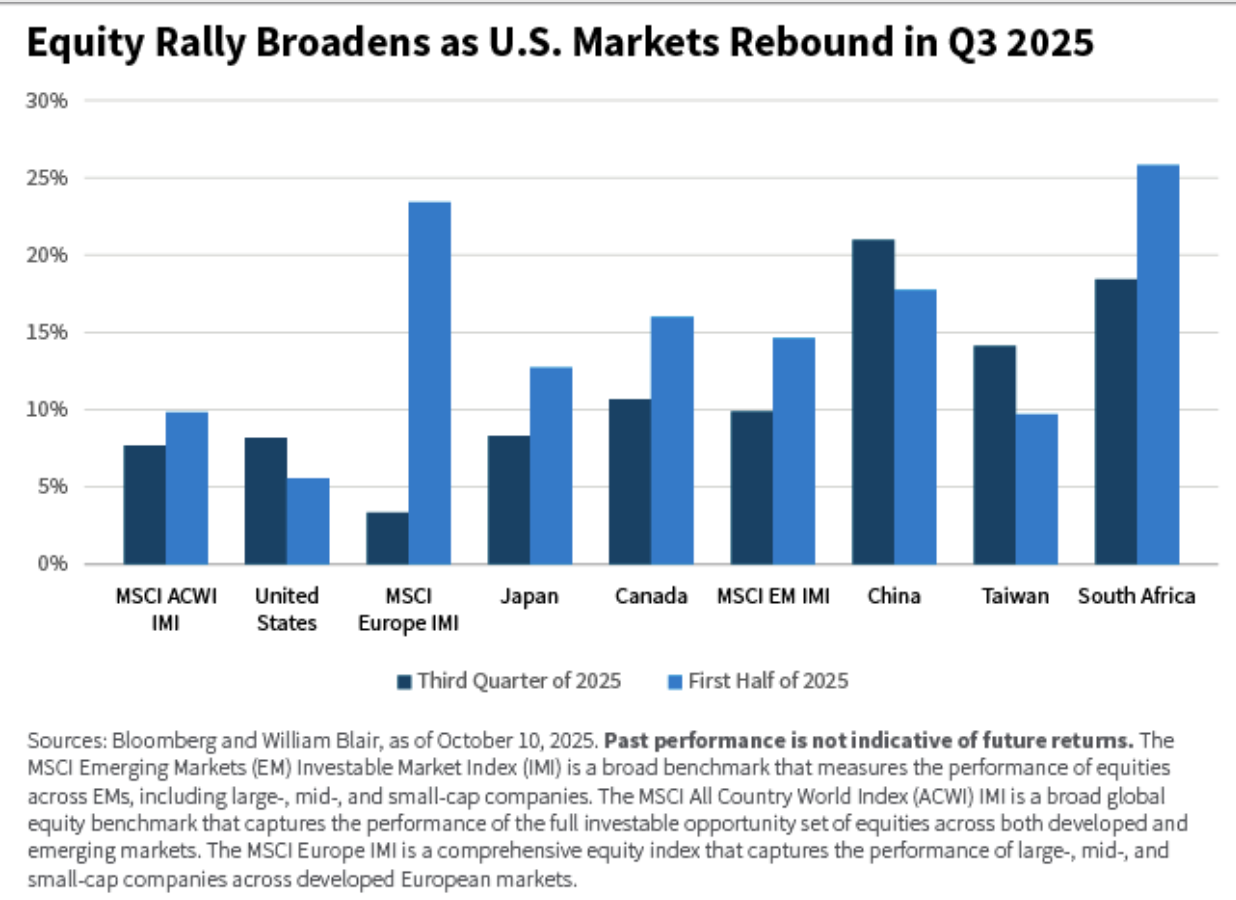

In continuation of the broad-based growth seen throughout 2025, public equities delivered strong performance in the third quarter of this year. Developed markets were up 7.4%, with Japan and Canada leading the charge and delivering 8.3% and 10.6%, respectively. In contrast to the first half of the year, U.S. equities roared back with returns in excess of 8%.

However, strong performance was not confined to only large caps in developed markets. For almost the first time in what seems like years, small-cap stocks kept pace with their large-cap brethren. China, Taiwan, and South Africa continued to post strong performance, gaining 20.9%, 14.1%, and 10.7%, respectively.

Notably, Chinese equities continued to surge, up over 42% year-to-date, with key outperformers linked to biotech and artificial intelligence (AI)-linked companies, reflecting investor confidence in China’s structural shift toward innovation and high-value industries.

The Growth-Value Paradox

Conventional factor analysis of the underlying performance consistently flags that both quality and growth have continued to underperform value. And it seems paradoxical to suggest that broadening and strengthening economic growth results in relative underperformance of growth as a factor.

However, this contradiction melts away on closer inspection. The MSCI Value Index[1] assesses a security’s price-to-book ratio, forward price-to-earnings ratio, and dividend yield to evaluate its inclusion in the index. Not surprisingly, financials stocks account for nearly a third of the value index by weight.

For much of the 2010s, global growth was anemic, interest rates were low, and real rates were outright negative in many places. Financials companies, which rely on the interest-rate spread, economic activity, and credit growth, delivered uninspiring returns and were shunned by investors. They became inexpensive, with no improvement optionality priced in.

Over the past several years, economic growth has broadened and the growth wedge between the United States and other major economies began to shrink, as we discussed in last quarter’s outlook, “Policy Reactions Narrow Global Growth Gaps.”

In addition, interest rates have risen across developed markets on the back of COVID-related inflationary supply disruptions; there is also a focus on growth in Europe and Japan, and banking stocks from these jurisdictions have delivered significant returns for investors.

In other words, improvement in economic growth has translated into earnings improvement for many companies in the MSCI Value Index.

More broadly, a key pillar of Japan’s corporate governance reform effort is to “name and shame” companies whose market value is below book value.

Specifically, since January 2024, the Tokyo Stock Exchange has published a monthly list of companies that have disclosed information regarding their capital efficiency initiatives to help improve overall capital allocation and raise return on equity for Japanese companies. As more and more companies succeed in improving their capital allocation and migrating to higher-growth end-markets, they offer rich investment opportunities for the skilled investor. And they are largely in the value indices.

Just as growth remains highly dynamic, so are the indices. When examining the composition of the broad indices, whether MSCI for global markets or Russell for the United States, we found that the constituents of the growth and value indices change regularly. In the past two decades, we have seen that 75% of the constituents have changed back and forth between growth and value, giving little merit to paying attention to the index when searching for where growth is inflecting.

Seeking Pockets of New Growth

As quality growth investors, we continue to look for growth and where it is changing, and we continue to find much to be excited about.

We have written extensively about European and broader defense, and it continues to be a rich growth area, as discussed in “Mapping the Future of EU Defense Spending.” While Russia’s invasion of Ukraine in early 2022 catalyzed the performance of defense stocks, the sector wide re-rating has likely played out. Now, it is up to those companies with earnings power that can deliver.

Defense remains at the technological frontier, and today, it means remotely operated equipment such as drones, which rely on ubiquitous and secure connectivity. Needs drive innovation, and we see tremendous activity in the buildout of low(er)-Earth-orbit satellite constellations that can provide low-latency connectivity over transregional and transcontinental distances.

For now, defense companies are building out the infrastructure—such as reusable rockets and engines—and satellite constellations necessary to deliver on this vision in the next handful of years. Over time, ubiquitous connectivity and surveillance will, for example, likely enable entirely new businesses in autonomous transport, banking, and healthcare delivery.

In addition, the AI buildout continues to pressure power generation demand in markets where electricity demand has not accelerated in years. Consequently, there are ample growth opportunities for power providers, utilities, and all those industrials that are involved in producing power, converting it into electricity, and delivering it securely to the end-consumer.

As ever, improving growth translates into stronger earnings streams, which at times are underappreciated. Asset price appreciation is the result, whether a company is classified in a value or growth index. This constant quest for improvement is at the core of what we do.

Hugo Scott‐Gall, partner, is the head of William Blair’s global equity team, on which he also serves as a portfolio manager.

1 The MSCI Value Index is a stock market index that represents the “value” segment of a broader MSCI equity index such as the MSCI World Index, MSCI USA Index, MSCI Europe Index, or MSCI EM index.

A message from Advisor Perspectives and VettaFi: Stay ahead of market changes with our daily updates on key market and economic indicators. Visit the AP Charts and Analysis site for our expert insights.

This content is for informational and educational purposes only and not intended as investment advice or a recommendation to buy or sell any security. Investment advice and recommendations can be provided only after careful consideration of an investor’s objectives, guidelines, and restrictions.

Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within William Blair Investment Management, LLC, or affiliates. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented.

Investing involves risks, including the possible loss of principal. Equity securities may decline in value due to both real and perceived general market, economic, and industry conditions. The securities of smaller companies may be more volatile and less liquid than securities of larger companies. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks. These risks may be enhanced in emerging markets and frontier markets. Different investment styles may shift in and out of favor depending on market conditions. Individual securities may not perform as expected or a strategy used by the Adviser may fail to produce its intended result.

Investing in the bond market is subject to certain risks including market, interest rate, issuer, credit, and inflation risk. Rising interest rates generally cause bond prices to fall. High-yield, lower-rated, securities involve greater risk than higher-rated securities. Sovereign debt securities are subject to the risk that an entity may delay or refuse to pay interest or principal on its sovereign debt because of cash flow problems, insufficient foreign reserves, or political or other considerations. Derivatives may involve certain risks such as counterparty, liquidity, interest rate, market, credit, management, and the risk that a position could not be closed when most advantageous. Diversification does not ensure against loss. The inclusion of Environmental, Social and Governance (ESG) factors beyond traditional financial information in the selection of securities could result in a strategy's performance deviating from other strategies or benchmarks, depending on whether such factors are in or out of favor. ESG analysis may rely on certain values based criteria to eliminate exposures found in similar strategies or benchmarks, which could result in performance deviating.

Collective Investment Trusts (CITs) are available to qualified retirement plans. For non-U.S. citizens or residents, William Blair offers a series of Luxembourg-domiciled SICAV products.

There can be no assurance that investment objectives will be met. Any investment or strategy mentioned herein may not be appropriate for every investor. References to specific companies are for illustrative purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future returns.

| | | |

Read more commentaries by William Blair