At QuantStreet, we’ve had an allocation to gold across our portfolios for the last year and a half.1 Our investment thesis, laid out in our March 2024 investor letter, rests on five pillars. First, our machine learning model likes gold (then and now), mainly because short-term interest rates are relatively high and these historically forecast gold returns positively. Second, gold typically does well during Fed easing cycles (as we document in our March 2024 Substack piece), and a Fed easing cycle is now underway. Third, our allocation strategy pays attention to asset-class momentum, and gold’s price appreciation over the past few years makes it attractive. Fourth, gold is a hedge for bad economic times, typically doing well during periods of market turbulence, and has a low correlation with other risk asset classes. Finally, the dollar’s status as a reserve currency has come into question recently, which favors non-dollar stores of value, like gold.

With interest in gold hitting a fever pitch, we now revisit our gold investment thesis.

A tail of gold in nine charts

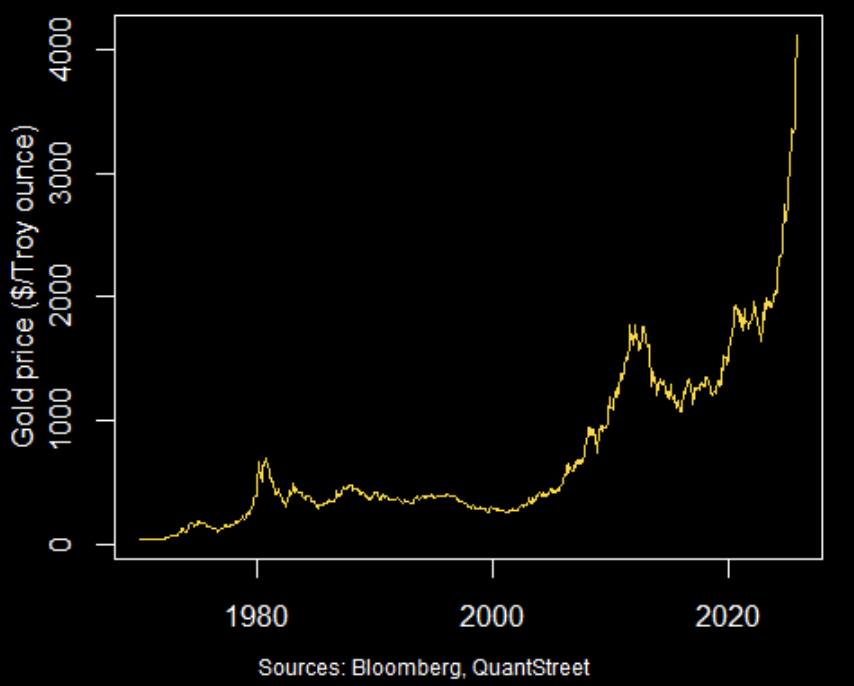

As the next chart shows, gold has rocketed upward since 2020, doubling over the last two years, and rising by over 50% so far in 2025.

As of the time of this writing, gold is trading north of $4,000 a troy ounce.

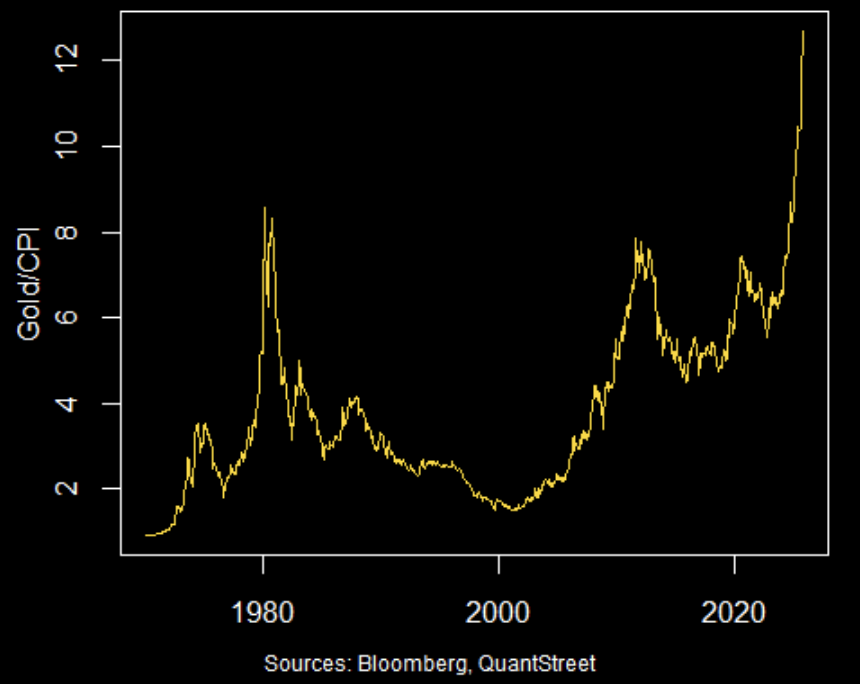

If gold were the perfect hedge for inflation—it isn’t—then gold prices divided by the overall price level would be constant over time. However, real gold prices (adjusted for inflation by dividing by the CPI price level) are currently at multi-decade highs.

Any time an asset price runs up this much this quickly, one wonders whether bubble dynamics are at play. More on this below.

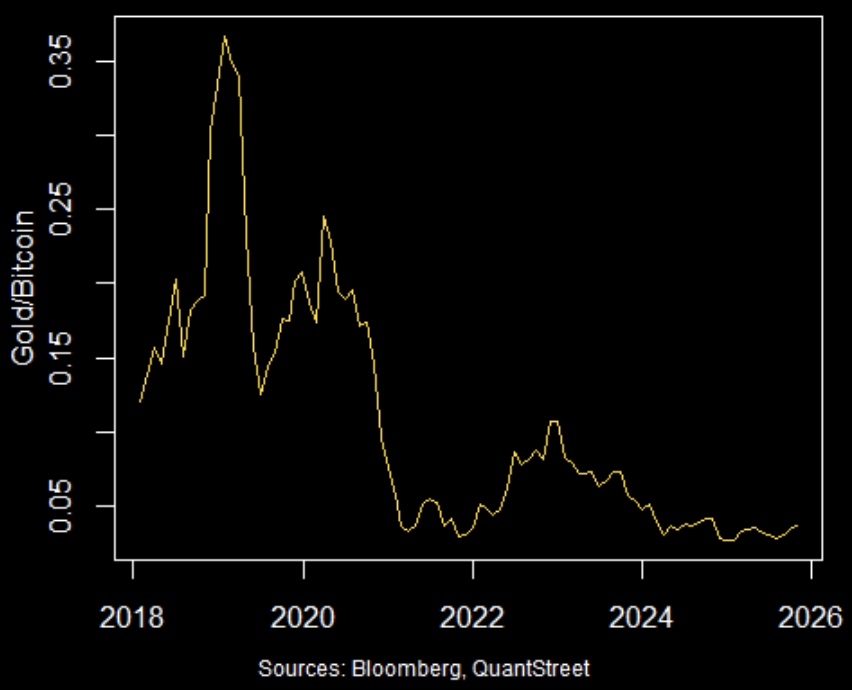

The next two charts examine the price of gold relative to two other valuation benchmarks. The chart on the left shows that the price of gold, when measured in units of bitcoin, is close to its all-time lows. Without getting into the debate about the merits and flaws of crypto investing, anyone holding bitcoin as a hedge against all manner of bad things might well consider switching part of that hedge into gold.

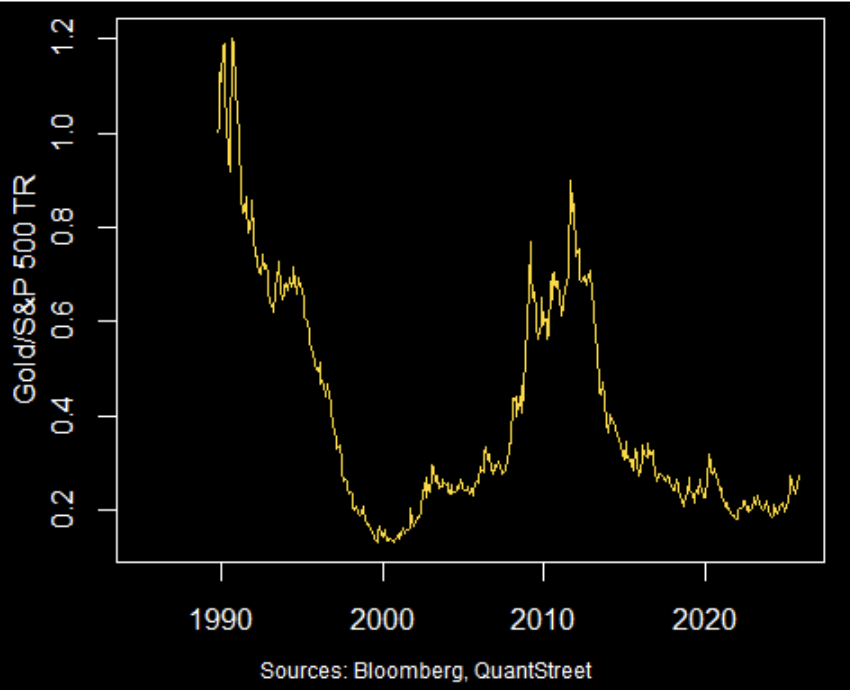

Similarly, the price of gold, when measured in units of the S&P 500 index (including reinvested dividends), is also near multi-decade lows. There is no particularly compelling reason to think that stocks—which entitle their owners to the earnings power of the underlying firms—should not outperform gold over long stretches of time, but at least we take some comfort in knowing that gold, even after its recent large price runup, has lagged equity returns over the last several decades.

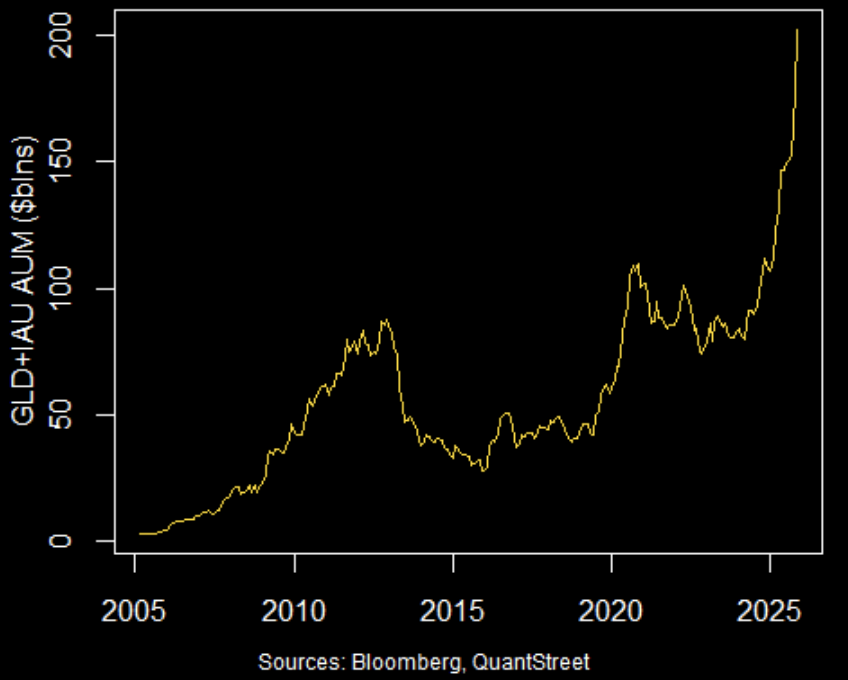

ETFs, because they enable investors to hold gold as a financial asset in their brokerage accounts and not as a physical commodity in their bank vaults, greatly increased access to the gold market.

The two largest gold ETFs, GLD and IAU, together hold over $200 billion of physical gold at current market prices. The $200 billion assets under management (AUM) figure consists of two components: new inflows of investor dollars into the ETFs and appreciation in the value of existing holdings due to the runup of gold prices.

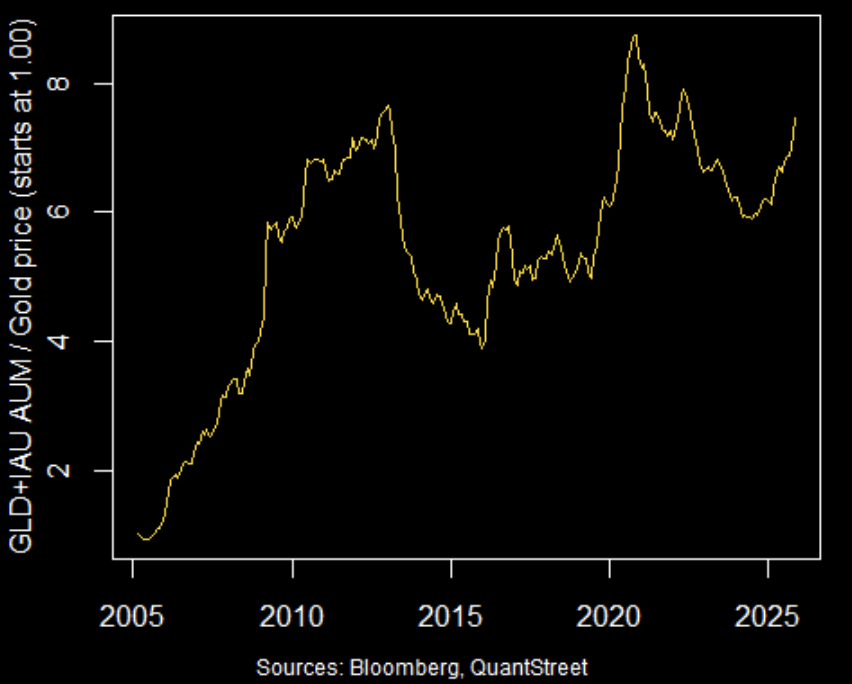

The next chart isolates the investor flow component of ETF gold holdings by dividing their AUM by the gold price level, normalizing the adjusted figure to start at one in early 2005, which is when the ETF holdings data become available.

An important feature of this year’s gold price runup is that it has been associated with large investor inflows into the two largest gold ETFs. Coupled with the multi-year trend of gold buying by global central banks, gold prices are not rising in a vacuum, but are doing so in response to strong investor demand. As the demand curve for gold shifts outward, unless the supply curve can shift outward equally quickly—which it cannot—gold prices will rise.

A similar observation about investor inflows into the gold market appears in a recent article by Nir Kaissar, of Bloomberg News, though he concludes that the gold trade in now long in the tooth and is best avoided.

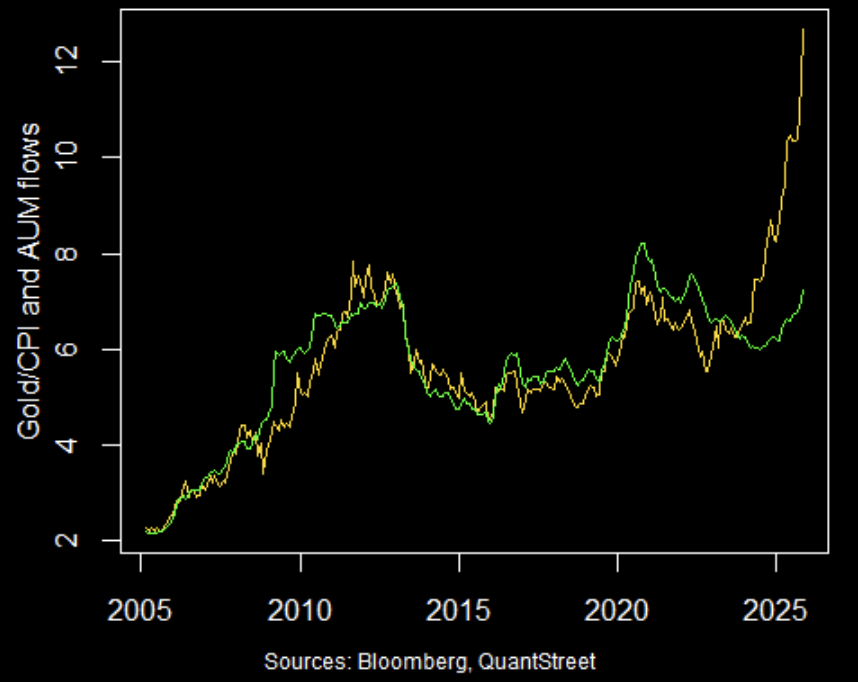

A natural question is the degree to which investor inflows into gold line up with gold price appreciation. The next chart—which first appeared in a very interesting LinkedIn post by Cam Harvey of Duke University—shows the real price of gold (i.e., after adjusting by inflation) plotted against a scaled version of the above investor inflows measure.

As Cam Harvey points out, the two series closely track each other up until the last few years, at which point the real gold price begins to diverge from the price level implied by investor inflows into gold ETFs. He refers to the underlying cause of this divergence as “de-dollarization,” with a promise to write more about this phenomenon soon.

Our own take is that the dollar’s status as a reserve currency has come into question over the last few years. Some of the well-known reasons for this—geopolitics, high deficit and debt loads, questions about the Fed’s independence, government shutdowns—are detailed in our recent investor letters (here and here). It is likely that central bank buying of gold is due to exactly these factors.

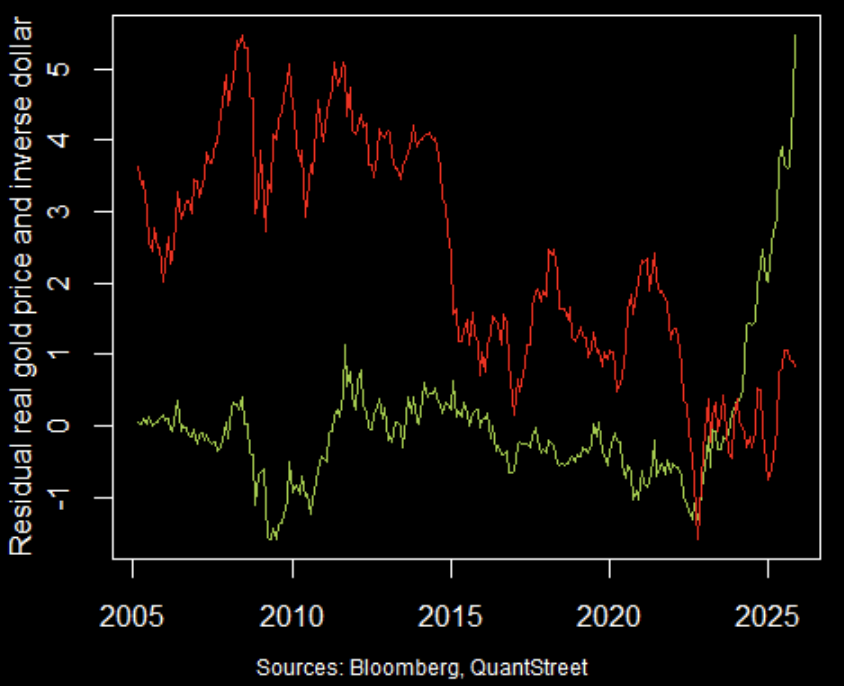

Looking at the part of the real gold price not explained by investor flows (the difference between the yellow and green lines in the above chart) and plotting this against the (negative) U.S. dollar price index (in red), reveals a striking pattern.

The gold price runup coincides almost exactly with the dollar’s peak (or trough of the negative dollar index) of September 2022. The gold price appreciates more than the dollar weakens, but the timing of the move lower in the dollar and move higher in gold is unlikely to be a coincidence.

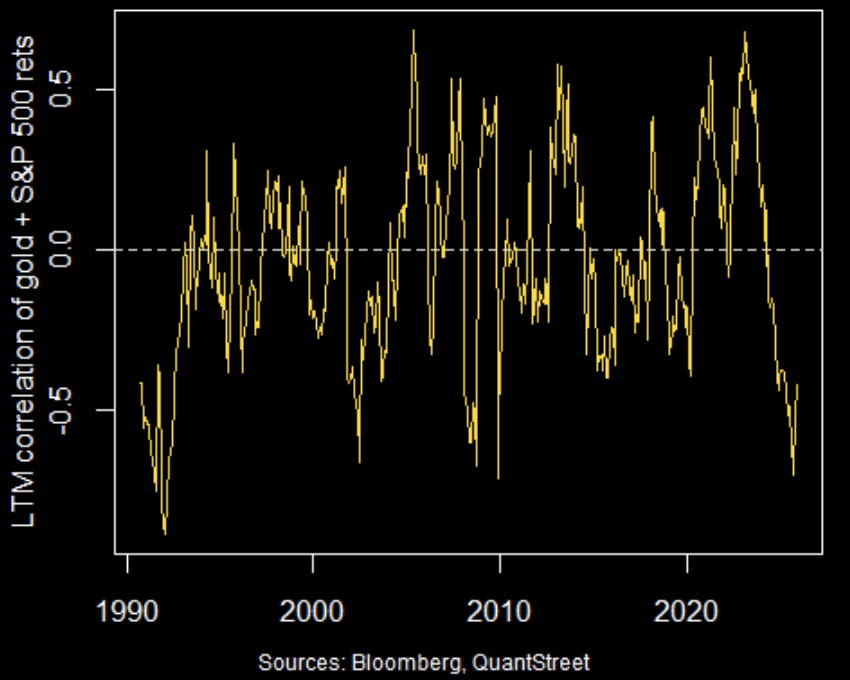

A key driver of investor demand is that gold often acts as a safe-haven asset in times of economic and market turmoil. One way to see this is to calculate gold’s average return in 12-month periods of large S&P 500 selloffs. We find that gold returns in such periods tend to be slightly positive. Another take on this question is the correlation between gold and stock returns.

The above chart shows the last 12-month correlation of monthly gold and S&P 500 returns, plotted over time. This correlation is often negative, which means that at times when the stock market sells off, gold frequently acts as a portfolio hedge. In recent years, the correlation of monthly stock and gold returns has been particularly negative, suggesting that gold has served as an effective hedge in investor portfolios.

Looking ahead

The currently high interest rate differential between U.S. rates and those of other countries (U.S. rates are higher) is dollar positive, as is America’s faster growth rate and lead in the AI revolution. If the dollar selloff were to reverse, and if questions around the dollar’s reserve currency status were to subside, gold may retrace a part of its recent rally. On the other hand, gold’s positive price momentum and tendency to appreciate during Fed easing episodes argues for continued strength. And with (geo)political uncertainty—the Russia-Ukraine war, China-U.S. jockeying for global influence, questions about Fed independence—still high, investor demand for gold is unlikely to subside overnight.

Whether or not gold makes sense for an individual investor depends on many considerations outside the scope of the present analysis. At QuantStreet, we will continue to evaluate gold in the context of our systematic portfolio allocation process, while considering the qualitative factors raised in this analysis.

Working with QuantStreet

QuantStreet is a registered investment advisor. It offers financial planning, separately managed accounts, model portfolios and portfolio analytics, as well as consulting services. The firm’s approach is systematic, data-driven, and shaped by years of investing experience. To work with or learn more about QuantStreet, contact us at [email protected] or sign up for our email list.

1 Details about QuantStreet’s performance are available here.

A message from Advisor Perspectives and VettaFi: Thinking about starting your own RIA, making a move to a different firm, or specializing in a new area? Read our latest articles on financial advisor transitions.

© QuantStreet Capital

Read more commentaries by QuantStreet Capital