Key takeaways

- Buffer ETFs partially shield investors from market selloffs but also limit upside gains, often underperforming the broader market.

- Their effectiveness is greatest during moderate market swings—when losses are limited to 15% or less and gains stay below 10%.

- A simple de-risking strategy may be a better alternative for investors who want to avoid big market drawdowns while still participating in market gains.

There’s FOMO—and then there’s fear of losing.

For many investors, the fear of missing out on market gains is usually second to the pain that comes from taking a loss in their portfolios. This is why many struggle to stay invested during rocky markets. Unfortunately, this tendency can lead to knee-jerk reactions like selling during a downturn—which means skipping out on the inevitable recovery.

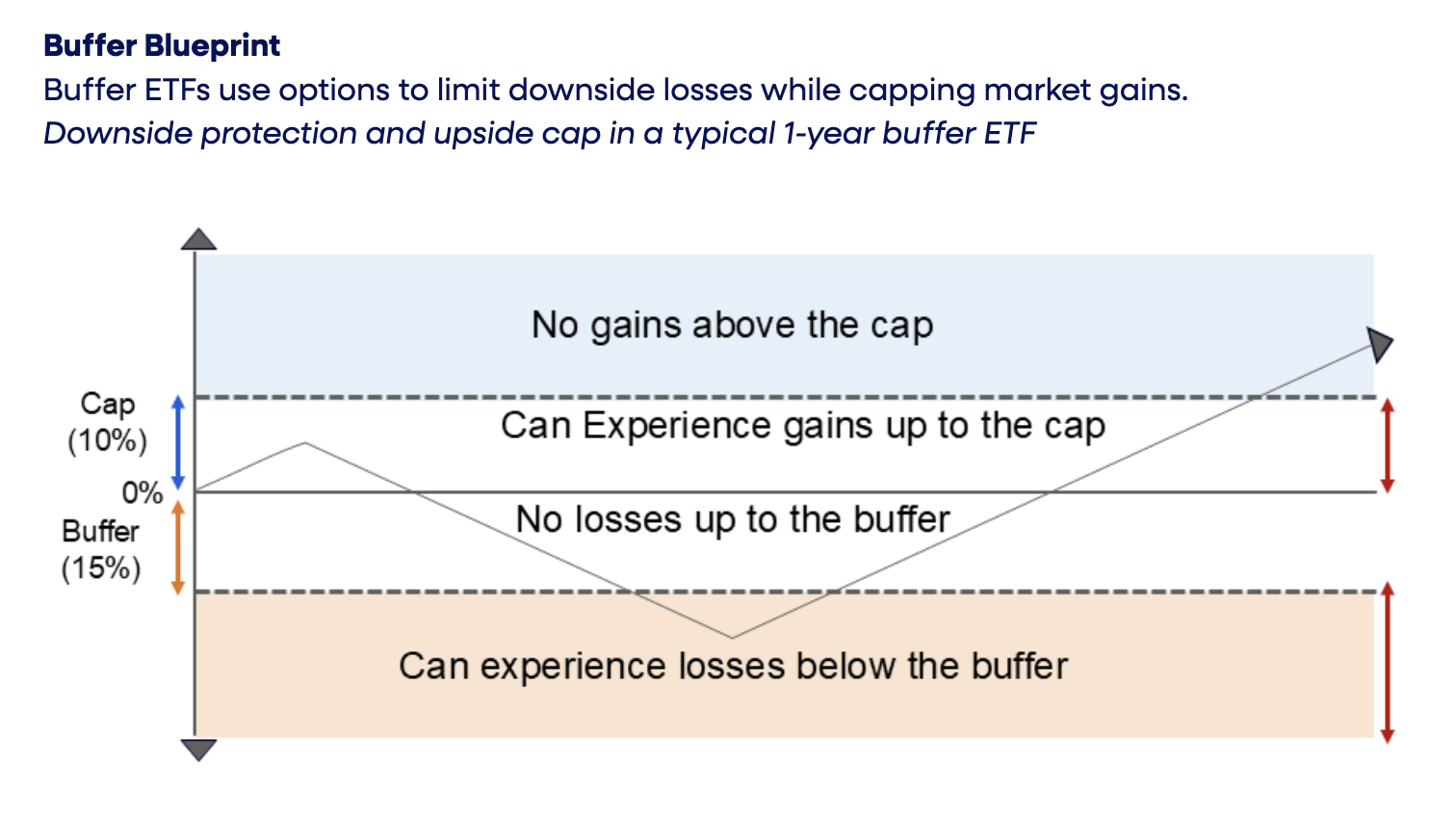

Enter buffer exchange-traded funds (ETFs). They aim to keep people invested by protecting investors from a certain percentage of market losses—the first 15%, in many cases. But there’s a trade-off: market gains are limited—usually to 10% or less.

This structure allows buffer ETFs to provide more predictable returns over time. The result is a smoother investment experience that can help investors stay the course during turbulent markets.

But is the sacrifice in returns worth it? Or is there another way for investors to minimize their losses while still getting meaningful returns? What about simply selling some stocks and moving to cash?

We’ll dive in and take a look shortly. But first, let’s go under the hood and learn the mechanics of buffer ETFs.

Creating the cushion

Buffer ETFs use a combination of options, or financial contracts, to limit market gains and losses over a period of time—typically 12 months. This is done in three key steps.

Step 1: Get Market Exposure

Buffer ETFs need exposure to the broader market. Most get this by purchasing a high-value “call” option to mirror the returns of a broad index like the S&P 500. Some funds may instead use futures or buy the index ETF directly, though that’s less common.

Examples:

- Buying a call option on SPY (the S&P 500 ETF) at a $600 strike price, covering 100 shares. This provides exposure similar to owning $60,000 of SPY.

- Buying 100 shares of SPY at $600 each, creating a $60,000 portfolio.

Step 2: Add Protection

A “put” option is bought to limit losses if the market falls. Because this is expensive, additional trades are used to offset the cost.

Example: Buying a put option for $3,400, which covers 100 shares of SPY.

Step 3: Set the Buffer and Limit Gains

To cover the cost of the protective put, two options are sold.

- Lower-strike put: Protects against losses up to a certain level in a “buffer zone.” Losses that go beyond this zone aren’t protected.

- Call option: Limits how much can be earned if the market rises above a certain level.

Together, these two options reduce or eliminate the cost of protection while defining the ETF’s range of returns.

Example: A 15% downside protection means selling a put option at a price that is 15% below SPY’s current level of $600. In this case, that’s $510. At $14 per share, that earns $1,400 total.

If SPY falls below $510, the protected put bought earlier and the sold call offset one another, leaving just exposure to SPY.

To cover the remaining cost of $2,000, a call option is sold at $660—earning $20 per share, or $2,000 total. This caps any gains if SPY rises more than 10% above the initial level of $600.

Combining steps 2 and 3 results in a zero-cost buffer that shields the portfolio from the first 15% of losses. However, if SPY falls below $510, the buffer no longer provides protection. On the upside, the portfolio participates fully in the first 10% of gains. Beyond that, the gains are limited because of the sold call option overlay, capping returns beyond a 10% increase in SPY.

At the end of the one-year period in this example, the buffer ETF resets. It starts a new set of options contracts with the same percentage buffer level and term length—but with a new upside cap, depending on current market prices.

Design School

The example above uses a one-year protection period, 15% downside protection and a 10% upside cap. In reality, these parameters can vary significantly from one buffer ETF to another. The length of the protection period, the size of the buffer and the upside cap all depend on how the fund is built.

Fund providers design buffer ETFs by adjusting three main variables:

-

How often they reset

Most buffer ETFs reset annually, but some reset every month or quarter, giving investors more flexibility and chances to re-enter the market.

-

Amount of protection

Common buffer levels range from 5% to 30%, depending on the fund. Higher protection typically means a lower cap on gains, as more money goes toward covering potential losses.

-

Fund structure

Some funds use set protection periods and reset on a specific date. Others offer continuous exposure, allowing investors to enter and exit at any time with a rolling options structure.

Price of Protection

While buffer ETFs offer a more controlled risk-return experience, it’s important to understand their drawbacks. Key among them is that investors may still see negative returns during the protection period—although these are typically smaller than what the broader market experiences. In addition, losses can be realized at the end of the protection period if the index falls below the buffer zone.

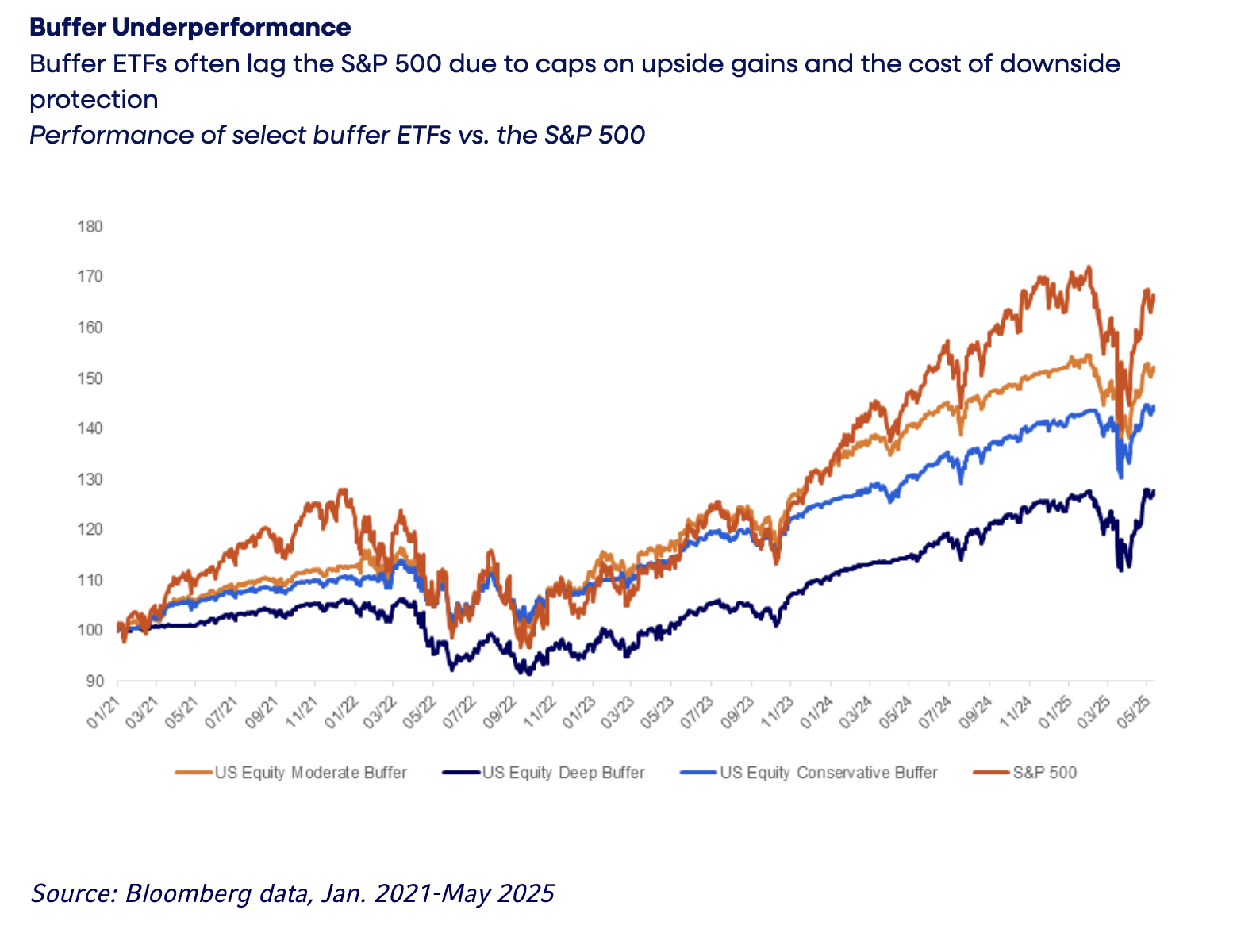

Most notably, because upside gains are capped, buffer ETFs often don’t keep up with the broader market. On average, they underperform by about 4% annually (below chart) due to this limitation, as well as the cost of downside protection. There is also a strong relationship between the size of the downside “buffer zone” and the degree of underperformance. The more protection offered against market losses, the greater the trade-off in returns.1

Buffer or Derisk?

With these limitations in mind, are there other, more robust ways to protect your portfolio against market drops?

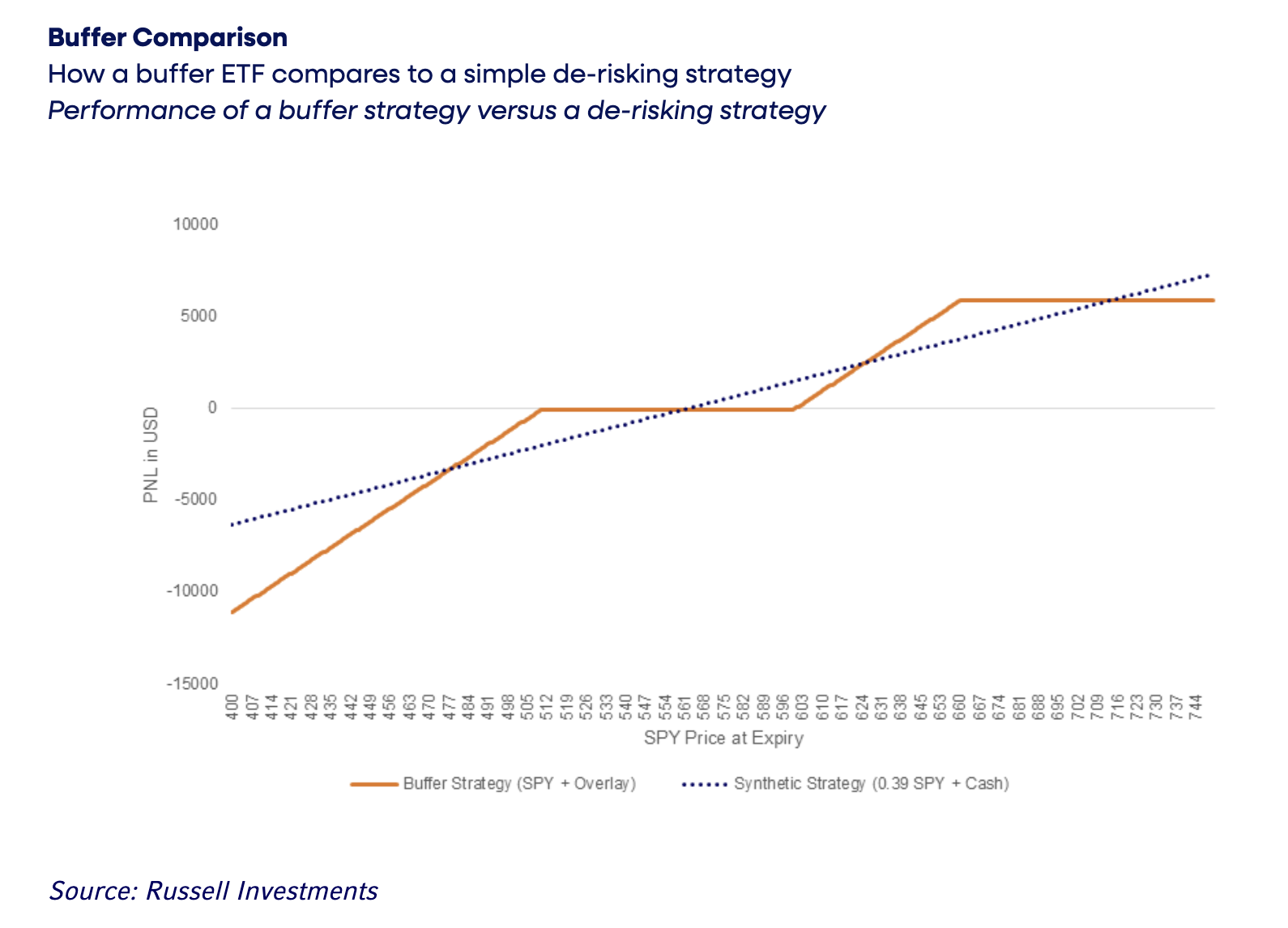

To explore this, let’s compare a one-year buffer strategy on 100 shares of SPY with a straightforward de-risking approach. This will show whether the complexity of buffer ETFs truly delivers better protection for defensive-minded investors—or if selling some stocks and moving to cash might be the smarter move.

Before we dive into the results, it’s important to understand that a buffer strategy is still partially sensitive to the stock market. In options terminology, this sensitivity is called “delta,” which measures how much a position's value changes in response when the price of SPY moves.

In the example we showed earlier, the buffer strategy has a delta of about 0.39. This means for every 1% move in SPY, the portfolio of options plus SPY is expected to move by about 0.39%. By comparison, a fully invested SPY position has a delta of 1.0, meaning it moves in step with the market.

Now, let’s consider an alternative approach: de-risking by moving part of the portfolio to cash. A portfolio with 39% in SPY and 61% in cash also has a delta of 0.39. This portfolio consists of 39 shares of SPY for $44,339—and $36,661 in cash.

The payoff after one year under different SPY outcomes for the buffer strategy and the de-risking strategy of 39% SPY and 61% cash2 is shown below.

Depending on how SPY moves over the year, either the buffer strategy or the de-risking strategy may come out ahead. Specifically:

- If the market moves above the upside cap or below the 15% buffer, the de-risking strategy generally performs better because the protection and gain limits no longer apply.

- If SPY ends the year flat at $600, the buffer strategy underperforms since the cash portion of the de-risking strategy earns a little interest.

- If SPY finishes the one-year period somewhere between a 15% loss and a 10% gain, the buffer ETF may outperform the de-risking strategy.

The key takeaway: buffer ETFs only perform better when market losses are less than 15% and gains under 10%. In a sharp selloff, a simple de-risking strategy of moving some money from stocks to cash usually outperforms. Conversely, in a strong rally, staying fully invested in stocks usually delivers higher returns.

Food for thought

Buffer ETFs can smooth out moderate market swings, but the cost of protection and their restrictions on upside gains often hold back returns. Depending on risk tolerance, investors may prefer either a straightforward de-risking strategy or the built-in protection of a buffer ETF.

1 S&P 500 performance versus three annual buffer ETFs from Jan2021 – Apr2025. US Moderate Buffer: 10% buffer (FT Vest US Equity Moderate Buffer), Conservative Buffer: 15% Buffer (Innovator S&P500 Power ETF), US Deep Buffer: 5% to 30% Buffer (FT Vest US Equity Deep Buffer). We observe a direct relationship between the size of downside buffer and the extent of underperformance.

2 We assume a cash return of 4%.

A message from Advisor Perspectives and VettaFi: Looking for a way to gain exposure to the evolving digital asset landscape? Learn about CoinShares ETFs.

Important information pertaining to the hypothetical example: Past performance does not predict future returns. Return level is proportionately scaled in line with cash level to be overlaid. Source: Russell Investments. Assumptions: Average cash level 1.0%, 10-year history from 12/31/2023, gross of fees. Opportunity cost from not securitizing cash varies by asset allocation and time period, and is represented by horizontal bars as marked within the chart legend. Target asset allocation used: 0% cash, 74% MSCI World, 26% Global Aggregate (GBP Hedged). For illustrative purposes only. Does not represent any actual investment. Indexes are unmanaged and cannot be invested in directly. Performance benefit (net) of overlaying cash by last 5 individual calendar year is as follows: 2023:20 bps, 2022:-17bps, 2021:16bps, 2020:14bps, 2019:23bps.

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Diversification and strategic asset allocation do not assure a profit or guarantee against loss in declining markets.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The Russell Investments logo is a trademark and service mark of Russell Investments

The information, analyses and opinions set forth herein are intended to serve as general information only and should not be relied upon by any individual or entity as advice or recommendations specific to that individual entity. Anyone using this material should consult with their own attorney, accountant, financial or tax adviser or consultants on whom they rely for investment advice specific to their own circumstances.

Products and services described on this website are intended for United States residents only. Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained on this website should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional. Persons outside the United States may find more information about products and services available within their jurisdictions by going to Russell Investments' Worldwide site.

Russell Investments is committed to ensuring digital accessibility for people with disabilities. We are continually improving the user experience for everyone, and applying the relevant accessibility standards.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates Management, L.P., with a significant minority stake held by funds managed by Reverence Capital Partners, L.P. Certain of Russell Investments' employees and Hamilton Lane Advisors, LLC also hold minority, non-controlling, ownership stakes.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

© Russell Investments Group, LLC. 1995-2025. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

© Russell Investments

More Innovative ETFs Topics >