Schwab’s Market Perspective: Dancing In the Dark

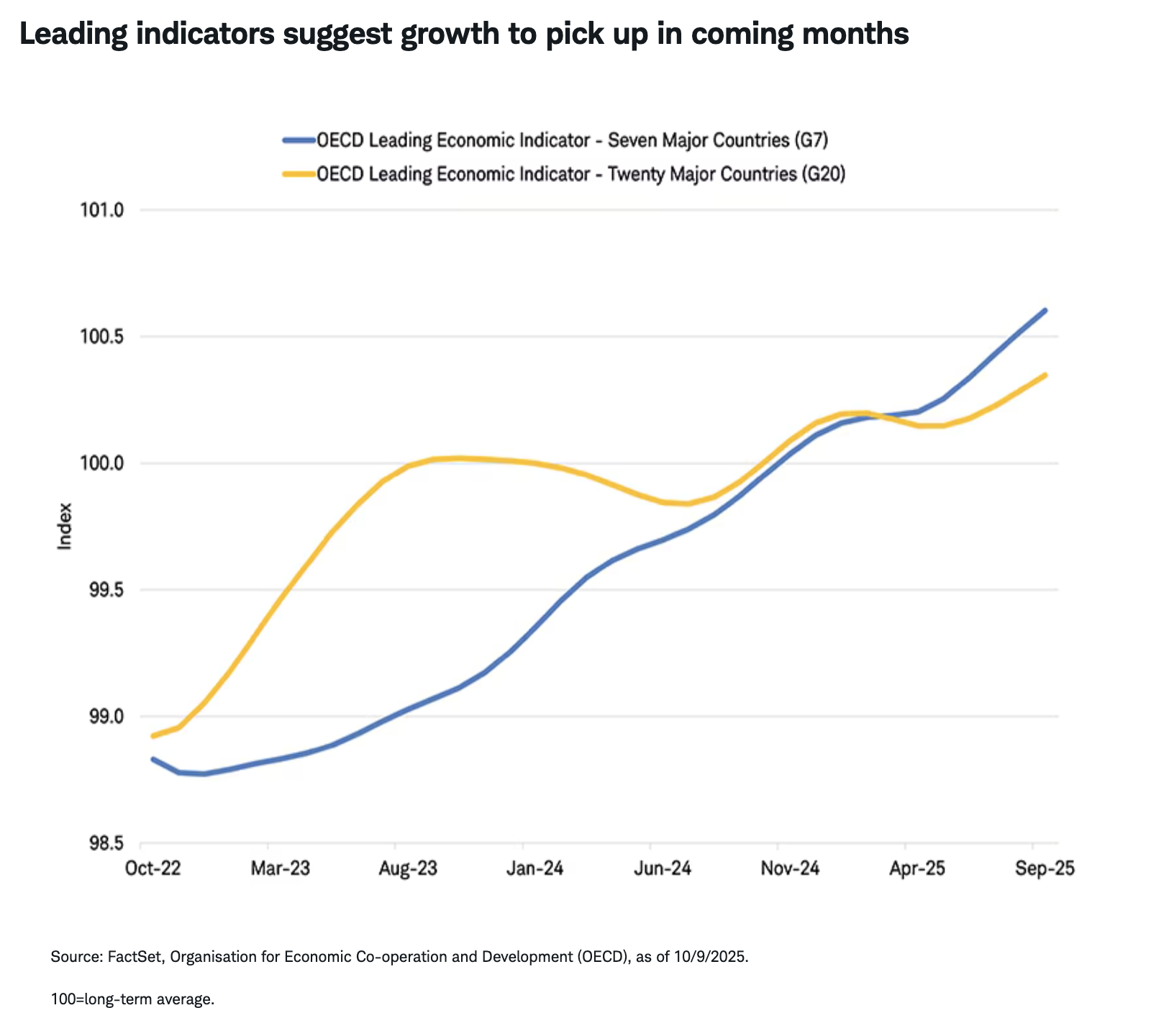

With the U.S. government still in shutdown mode, the list of missing economic reports—such as nonfarm payrolls, construction spending, and the trade balance—continues to grow. So far, domestic stock and bond markets have taken the shutdown in stride, but the recent tumble over trade tensions shows that volatility can quickly resurface for a number of reasons. Globally, growth appears to be slowing but could pick up next year.

U.S. stocks and economy: Can't start a fire without a spark

U.S. government data are the gold standard in terms of depth and breadth, so with the Bureau of Economic Analysis (BEA), Bureau of Labor Statistics (BLS), and other agencies closed, markets and investors have little to guide them. It's worth noting that the BLS is calling back employees to put out September's delayed consumer price index (CPI) report, which is now slated for release on October 24.

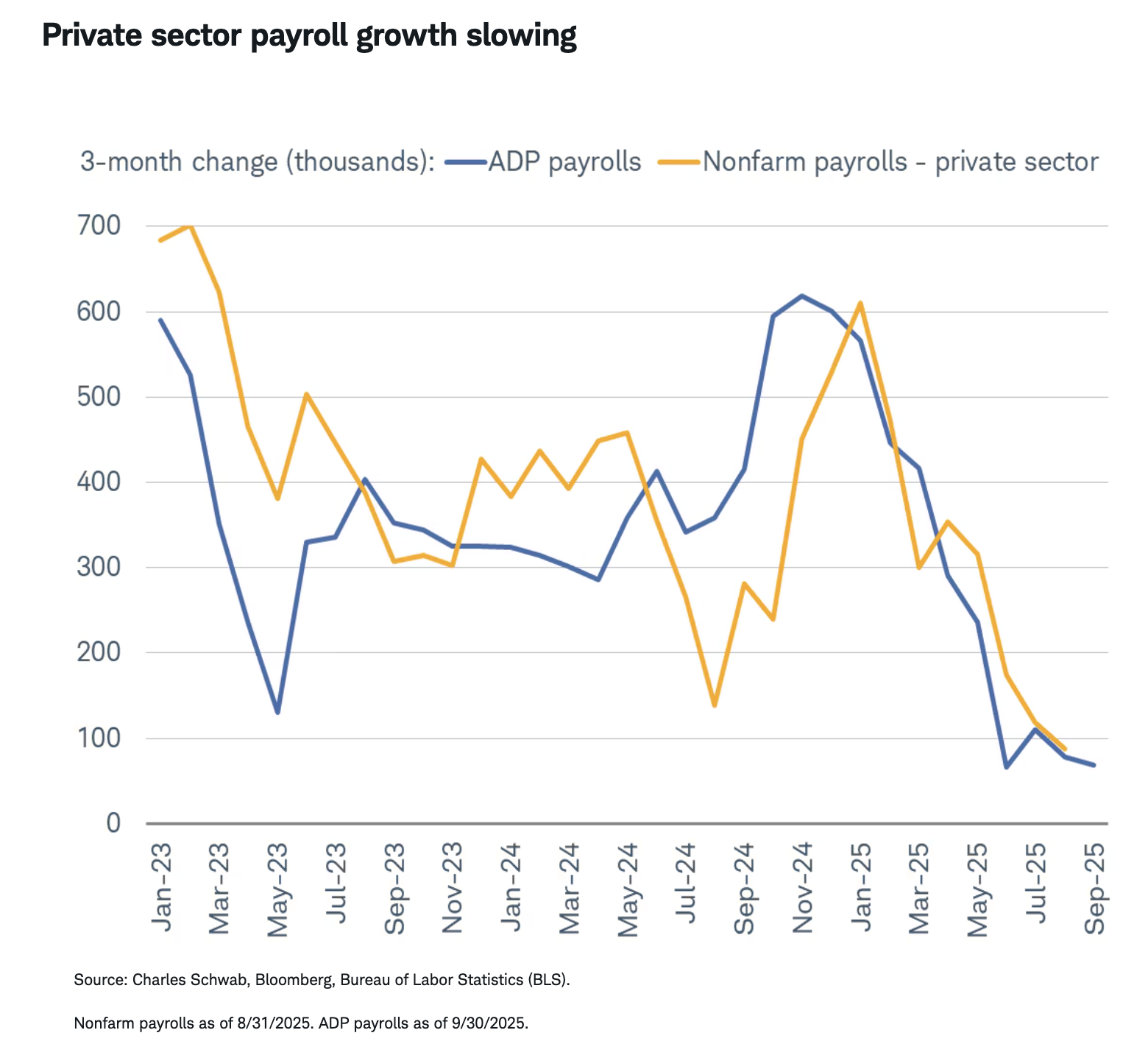

Until then, we're left sifting through data from the private sector, such as ADP's employment report. That report, which tracks private sector jobs, showed a decline of 32,000 in September—far worse than August's decline of 3,000, which itself was revised down from an initially reported gain of 54,000. In essence, the labor picture was already much worse than expected heading into September.

The ADP report often gets a lot of flak for not mimicking the BLS's monthly nonfarm payrolls report, given the (at times) large difference in the two data sets. However, the relationship over the past three months looks like it's growing tighter, at least when it comes to the trend, as you can see in the chart below.

On the inflation front, we'll know more after the BLS sends out September's CPI report. However, assuming the government remains shut down, we won't see the producer price index (PPI) or personal consumption expenditure (PCE) price index—so the inflation and broader economic backdrop remains darker given the lack of available government data.

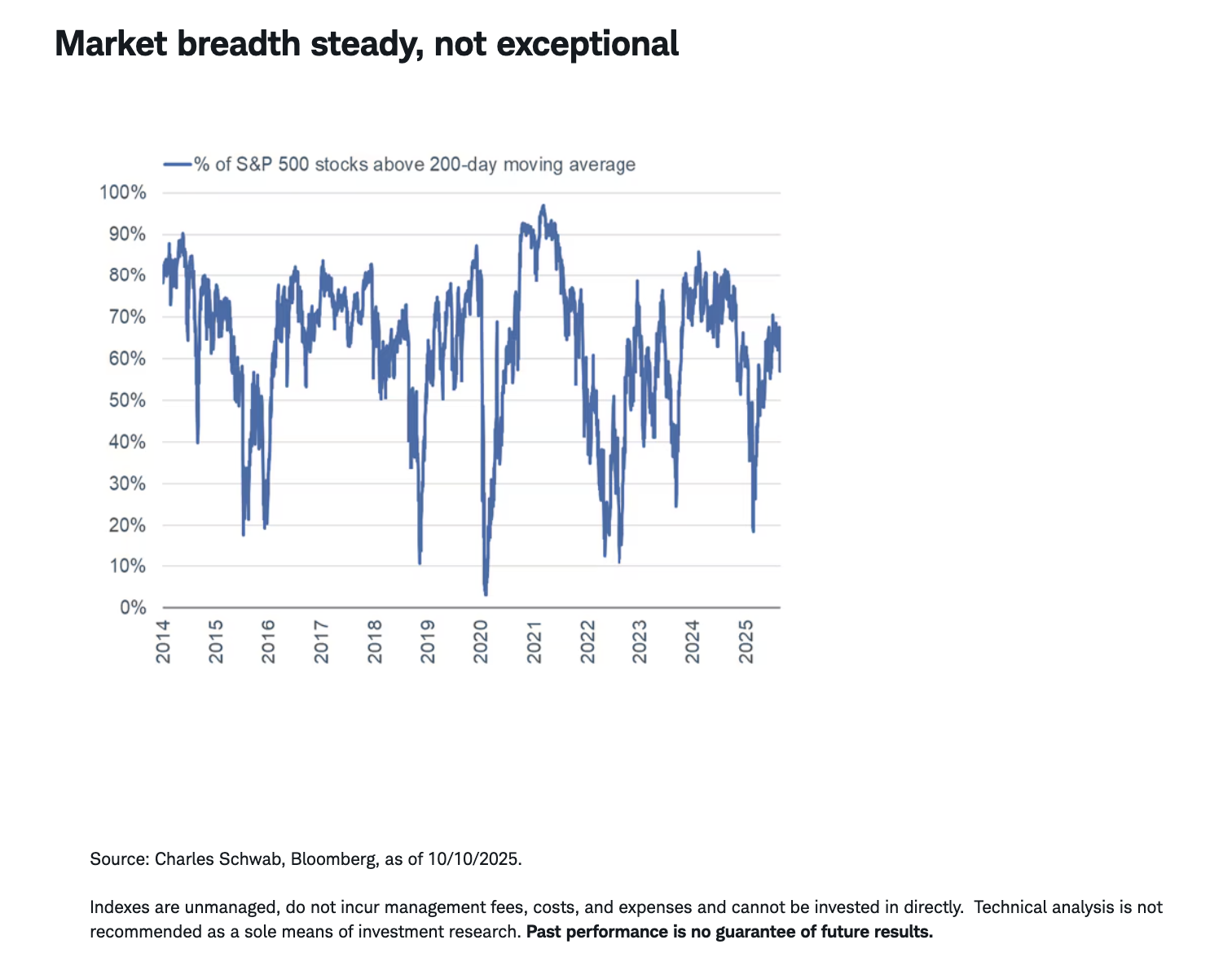

Markets have mostly taken the shutdown in stride, evidenced by the still solid (but not exceptional) percentage of S&P 500 members trading above their 200-day moving average, but we anticipate further volatility and disruption if the shutdown lasts for several more weeks—especially given the potential for CPI and payroll data to not be collected.

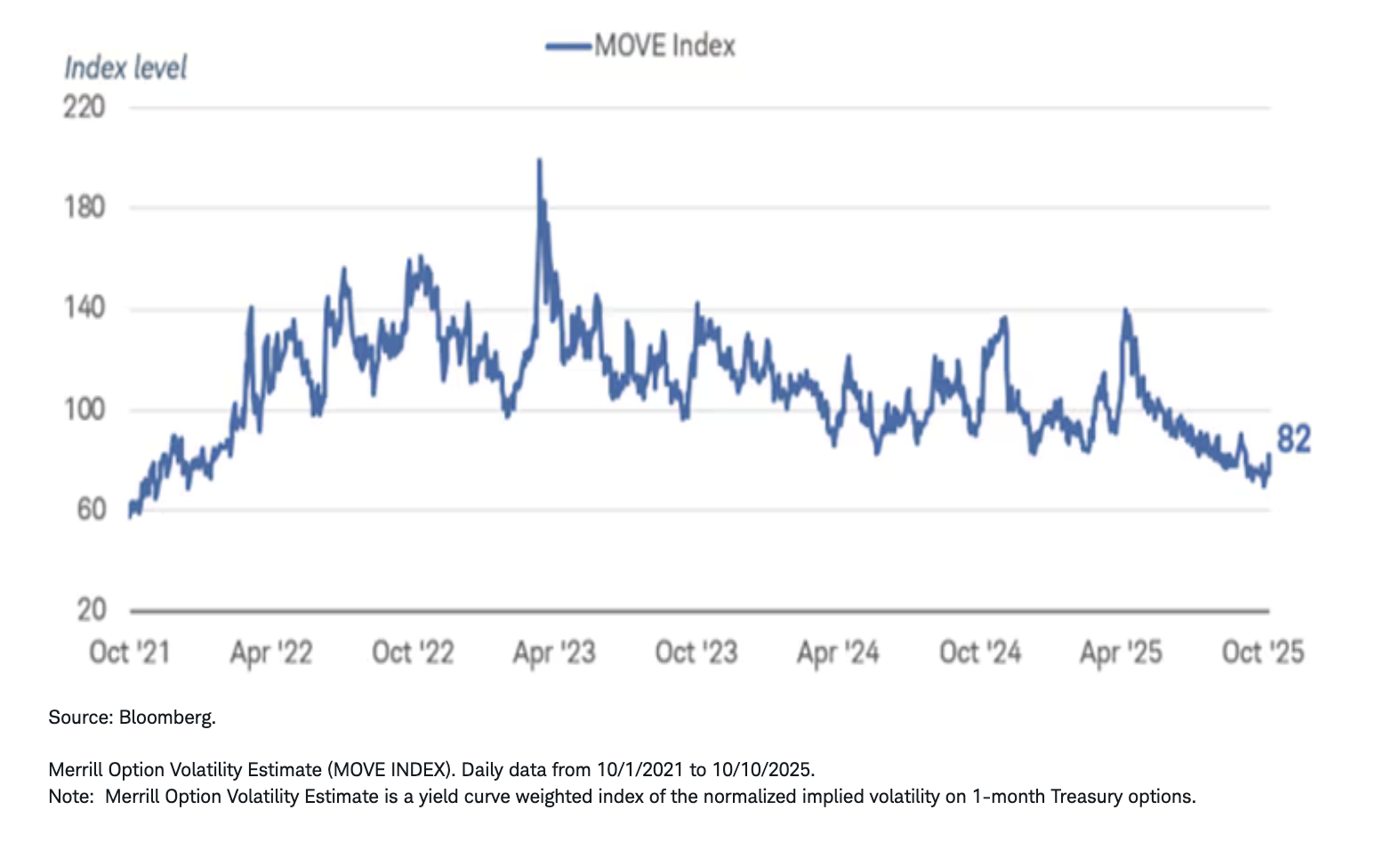

Fixed income: No data? No problem!

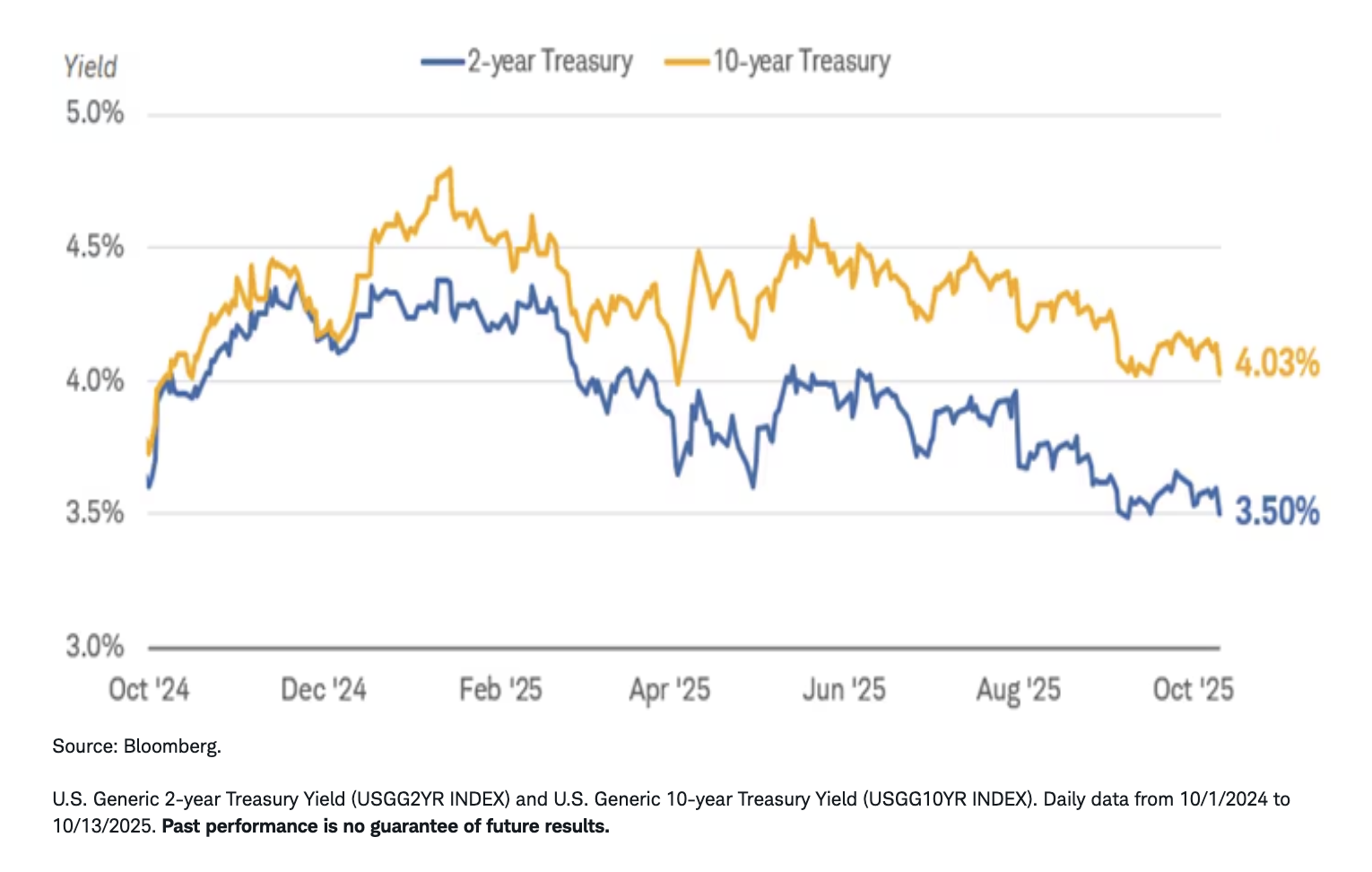

The fixed income markets have settled into a quiet range in the absence of fresh economic data. Markets are still discounting several interest rate cuts by the Federal Reserve over the next six months, and volatility is near its four-year low. However, it is far from clear that the Fed has room to cut rates as rapidly as the market is expecting.

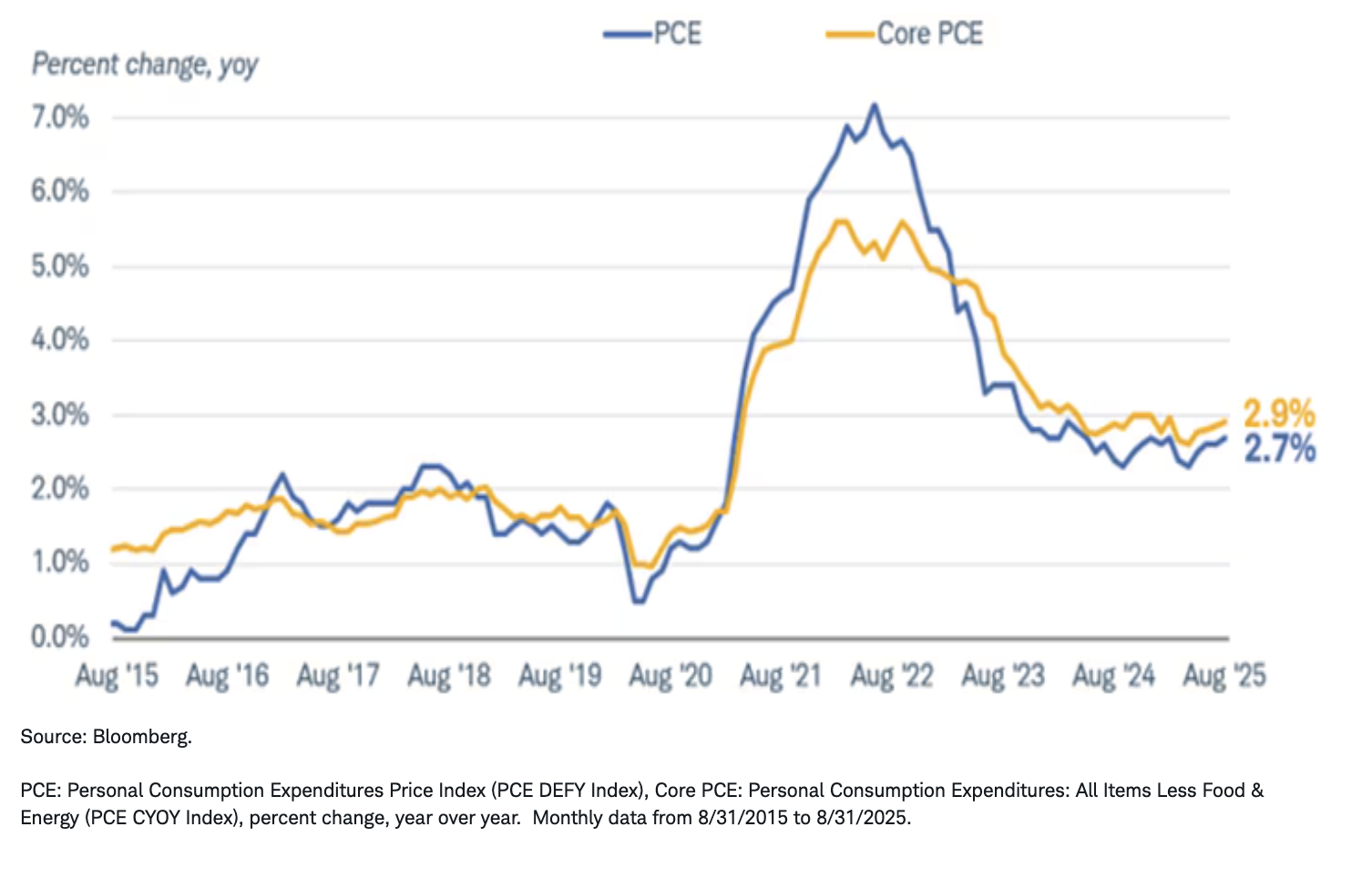

The Fed is caught in a tug-of-war between a slowing labor market and persistent inflation. The pace of job growth has dropped sharply from an average of 111,000 per month in the first quarter to just 29,000 in the past three months, and the unemployment rate has begun to edge higher. However, inflation has been stuck at just under 3% for most of the year, well above the Fed's 2% target.