Key Takeaways

- The structural characteristics of emerging markets provide active investors with the opportunity to generate alpha—returns beyond the index and beyond passive investment strategies.

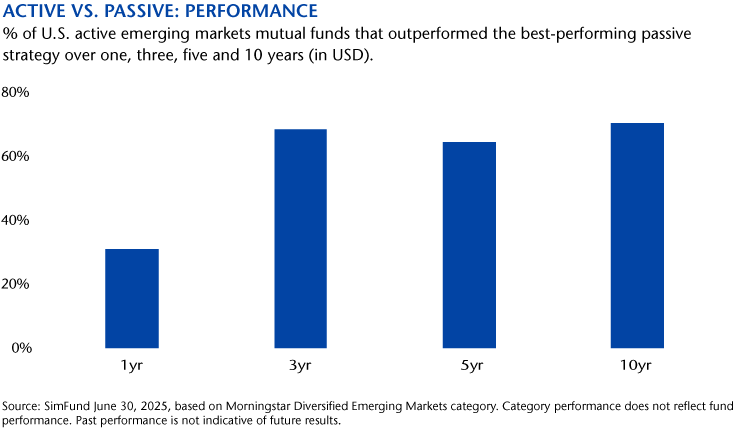

- The long-term outperformance of active investment strategies demonstrates the impact of alpha generation.

- Core active strategies can offer balance and greater flexibility than strategies with style biases, which is often key in markets where multiple variables impact returns.

- Country allocation plays a crucial role in active investment management by identifying areas that may either support or may hinder potential stock-picking opportunities.

Emerging markets, we believe, offer compelling opportunities. One of the choices investors need to consider when seeking exposure to the asset class is how active they want their exposure to be. Passive equity strategies have successfully harnessed robust U.S. equity returns over the past decade. Does the same playbook apply to emerging markets? The merits of passive investing can be argued for emerging markets, as they can for most equity markets. However, we believe that to generate sustainable returns over the medium to long term, the role of an active strategy is also crucial.

In contrast to the U.S. and other developed markets, emerging markets comprise multiple economies at different stages of development—some facing headwinds, others benefiting from tailwinds. Emerging markets tend to be less efficient and are often under-researched. Despite their vast scope, indexes can also become concentrated in a small number of companies as market capitalizations or free floats increase and these companies may not necessarily be best positioned to provide attractive future returns. We believe these factors create an opportunity for active managers—through research, local expertise and fundamental investing—to generate alpha that exists beyond the scope of index products and many smart beta strategies.

We believe actively managed funds can be a vehicle for exposure to emerging markets and a complement to passive investments in the asset class; they are a platform that can identify and unlock opportunities within these complex markets, often outside benchmark indexes, and we would argue the long-term performance of these strategies proves this.

Why Active Investing Works for Emerging Markets

When considering adding or increasing exposure to emerging markets, investors should also be cognizant of the different types of active strategies that are designed to generate alpha. In our view, a core active approach—unconstrained by index composition or by investment style—offers both flexibility and balance.

Core active strategies have the flexibility to make portfolio decisions across markets and take different tactical postures, be it more aggressive or more cautious. They can also seek opportunities in small-cap companies or probe deeper into thematic trends. In contrast, some actively managed strategies can tilt toward value, growth or momentum investing, which can be restrictive if the market environment is not aligned with the style bias. The latent strength of the core active approach, however, is in the ability to have greater—or lesser—exposure to markets. We believe this flexibility is the foundation for generating long-term returns that outperform the index.

We can distill the strengths of core active investing in emerging markets into five key areas:

-

Countries Matter

Domestic political developments or economic policy changes can directly influence company earnings and market sentiment. While domestic variables have always been important in emerging markets, their influence has amplified in recent years and they can contribute to wide dispersions in the returns at the country level. It points to the importance of country allocation in managing exposure and also the potential for alpha generation in the asset class.

-

Importance of Stock Picking

Assessing company fundamentals, management teams and the growth trajectory of a business is at the core of generating market outperformance. This process requires deep analysis of financials, competitive advantages, supply chains, capital efficiencies, management quality and business outlook. Evaluating governance standards is also crucial. Poor standards can undermine earnings growth and profitability, and active investing can play a crucial role in screening out companies with substandard governance and weak regulations. More importantly, good governance research is a key tool that enables active managers to add exposure to companies with weak standards at the right price and to engage with those companies to improve their governance, thereby improving investment return potential.

-

Portfolio Construction

A key strength of core active management is the scope to invest across companies, markets and cycles. Part of this strength is the ability to vary or avoid exposure to holdings and markets included in benchmark indexes. In addition, being intentional about active risk in portfolio construction is critical to achieving investor return goals and consistent performance. In our view, aggregate active risk in a portfolio should align with a strategy’s outperformance target to ensure the manager has the potential to deliver the expected risk-reward profile for investors.

-

Market Mispricing

Emerging markets are generally less efficient than those of advanced economies. This may be in terms of volume of liquidity, scope of capital markets or the availability of information. For example, in markets with minimal equity analyst coverage, the level of information to passive investors is limited. In contrast, portfolio managers can gain a more comprehensive understanding through proprietary research of markets and companies.

-

Focus on Alpha

For most investors, we believe an index-aware, fundamental active core strategy can be an appropriate way to generate sustainable investment returns over the medium to long term. Passive strategies can efficiently replicate an index and have lower tracking errors. They offer simplified exposure to emerging markets which can be less effective if the market itself is volatile or in decline. Alternatively, smart beta and quantitative strategies offer style biases, such as a growth or value orientation, as a way of filtering a desired opportunity set for investors. These biases can lead to wider tracking errors and may result in investment returns that differ from the index.

The core approach prioritizes generating alpha. It allows active managers to navigate across countries, markets, sectors and companies, embracing different styles and taking thematic positions. Core active managers can add value at both the country and stock level, control exposure to market risk and maintain flexibility over what markets to invest in.