Schwab's Market Perspective: The Inflation Problem

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe Federal Reserve is likely to cut short-term interest rates at least twice before the end of the year, but stubborn inflation may keep long-term bond yields and mortgage rates from declining much. That means some of the issues that have been weighing on economic growth and homeownership won't get much relief from easier Fed monetary policy. Meanwhile, international inflation patterns have begun to diverge, but prices are still rising in countries including the U.K. and Canada.

U.S. stocks and economy: Mortgage rates pressure housing affordability

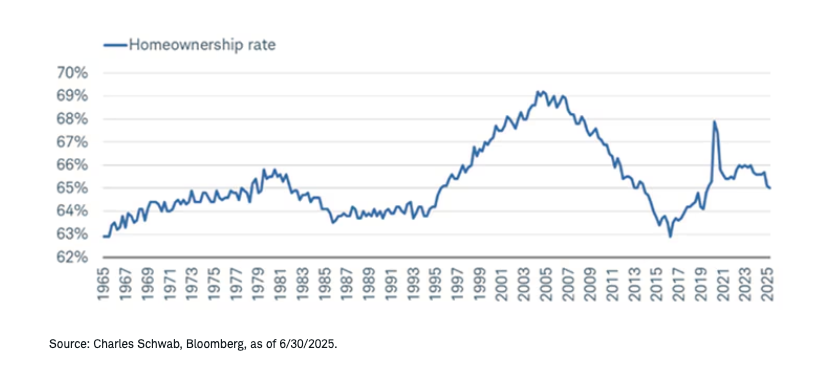

The U.S. housing market has yet to regain its equilibrium following the COVID-19 pandemic. After going through a mini boom during the pandemic—when migration patterns shifted immensely in both size and speed—mortgage rates spiked, affordability weakened, and home sales tumbled.

Arguably, still-high home prices are the main driver putting downward pressure on the U.S. homeownership rate, which has fallen to a multi-year low and essentially unwound its entire gain since the beginning of the pandemic. Our sense is that—particularly among younger and/or new homebuyers—this metric won't begin to maintain a durable uptrend until mortgage rates come down and home price growth moderates further in the existing home market. That must happen in the context of a labor market that continues to be resilient.

Homeownership rate has declined to a multi-year low

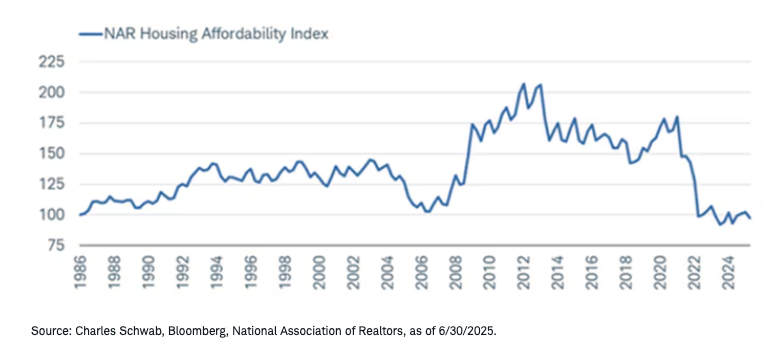

The National Association of Realtors' Housing Affordability Index measures whether a typical family has sufficient income to qualify for a mortgage on a median-priced home. It assumes a 20% down payment and mortgage payments limited to 25% of income.

Housing affordability remains low

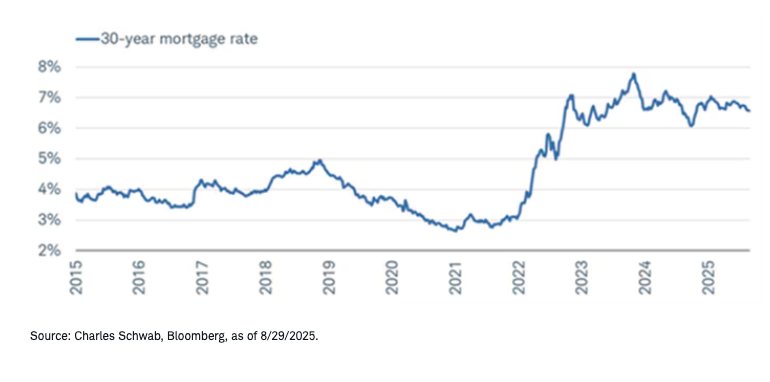

The second housing affordability component is mortgage rates. As shown below, from a peak of nearly 8% in late 2023, the average 30-year fixed mortgage rate is now about 6.6%. Given the likelihood that the Federal Reserve will start cutting the federal funds rate this month, there is an assumption that mortgage rates would come down, as well.

However, that's not necessarily the case. Bond market investors, not the Fed, "control" mortgage rates, which are typically most closely correlated with the 10-year Treasury bond yield. While the Fed can cut the federal funds rate—a very short-term rate that represents the interest banks charge each other for overnight loans—longer-term interest rates are more affected by investors' expectations about future inflation and economic growth. During the period last fall when the Fed lowered the federal funds rate by 100 basis points, mortgage rates rose by about 80 basis points (a basis point is one-hundredth of a percentage point, so 80 basis points is equal to 0.8%). If a Fed short-term rate cut caused investors to expect higher inflation in the future, mortgage rates would not decline.

Mortgage rates remain relatively high

Fixed income: The winding road to lower long-term rates

With inflation elevated and fiscal deficits rising, there may not be room for Treasury yields to fall much further, especially those with longer-term maturities. We anticipate a modest move down in short-to-intermediate term Treasury yields over the next few months as the Federal Reserve lowers the federal funds rate, but long-term yields are likely to remain elevated in the absence of falling inflation and/or a decline in fiscal deficits.

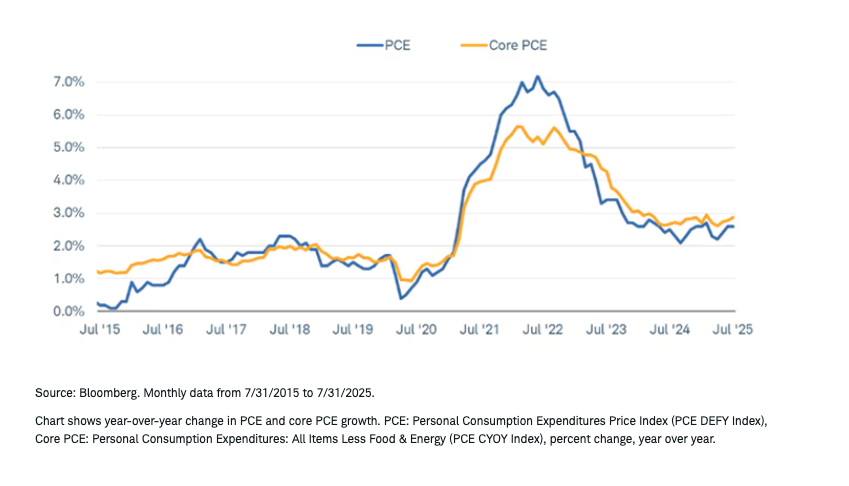

Recent inflation readings underscore the difficulty facing the bond market. Inflation has been above the Fed's 2% target for four years. It has fallen steeply from its pandemic peak but has been stuck in the 2.5% to 3.0% range for over a year. Recently, it has been edging higher and the flowthrough of tariffs will likely push it higher into 2026.

Inflation remains above the Fed's 2% target

The Fed's dual mandate requires it to set policy to achieve low inflation and full employment. With inflation elevated and the unemployment rate at 4.3%, it seems that a rate cut is not warranted. However, recent labor market data suggest there has been a slowdown in hiring with layoffs starting to pick up. The unemployment rate has held at a low level because there have been fewer new entrants into the labor force.

We expect the Fed to cut rates at least twice by the end of the year. Beyond that, it would take a much weaker economy, a significant deterioration in the labor market, and/or much lower inflation to warrant further easing by the Fed.

Government fiscal policy is also a factor that could keep long-term bond yields from falling

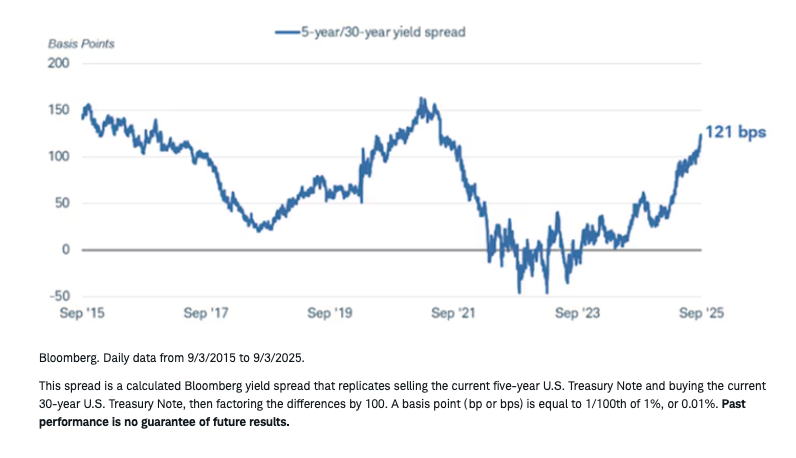

much. Rising federal budget deficits imply the need for higher debt issuance that will need to be absorbed by the market. In the U.S., the market has remained fairly calm about the prospect for ever-rising deficits, but the steepening of the yield curve is an indication of growing market concerns. The difference in yields between five- and 30-year Treasuries, at roughly 120 basis points, is the widest since 2021. Our interpretation is that investors are demanding a higher yield for long-term Treasuries to compensate for the risk of inflation and/or depreciation of the dollar as a consequence of high debt levels.

The spread between the five- and 30-year Treasury yield is the widest since 2021

International stocks and economy: Inflation diverging by country

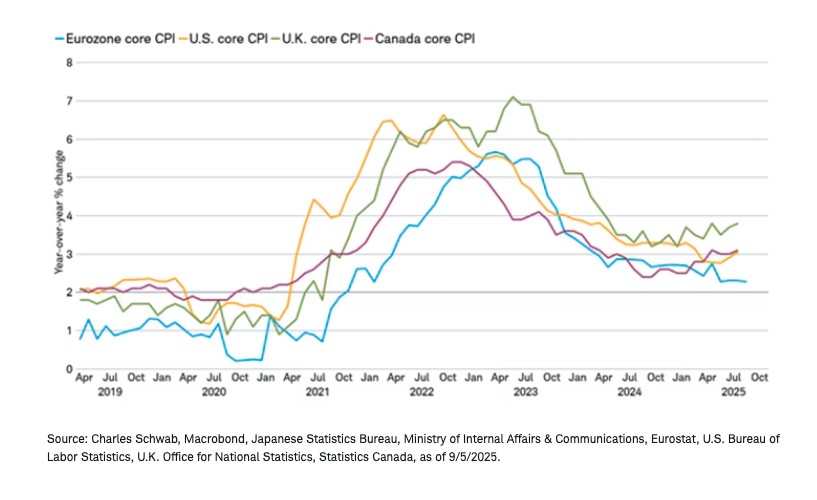

Inflation globally went up in sync across developed economies during the post-COVID period. While central banks initially viewed this inflation as "transitory," or temporary, the increase in prices had the knock-on effect of raising wages. Wages, an input to most goods and services, contribute to rising prices across the economy when they increase, creating a feedback loop often referred to as a wage-price spiral.

Developed economies' central banks started raising interest rates in 2022 to arrest inflation. Although the consumer price indexes (CPI) excluding food and energy prices (known as "core" CPI) peaked at different times, the rise and subsequent fall of inflation looked somewhat similar during this period. However, this year, we saw a divergence in the pattern. Inflation in the U.K. has increased due to an increase in minimum wages and energy bills, while the CPI in Canada is rising on the back of higher shelter costs and retaliatory tariffs in response to U.S. tariff threats. In the U.S., inflation has been sticky and the full impact of tariffs on goods prices may still be on the way. Meanwhile, the eurozone is notably seeing inflation continuing to trend lower.

Inflation diverging?

Looking at core inflation in isolation doesn't seem to tell the full story. Central banks in Canada and the eurozone have reversed nearly half of the most recent cycle's rate hikes. In the U.K., persistently high inflation has restrained the Bank of England's ability to cut rates. Uncertainty over the impact of tariffs in the U.S. has kept the Federal Reserve on hold this year.

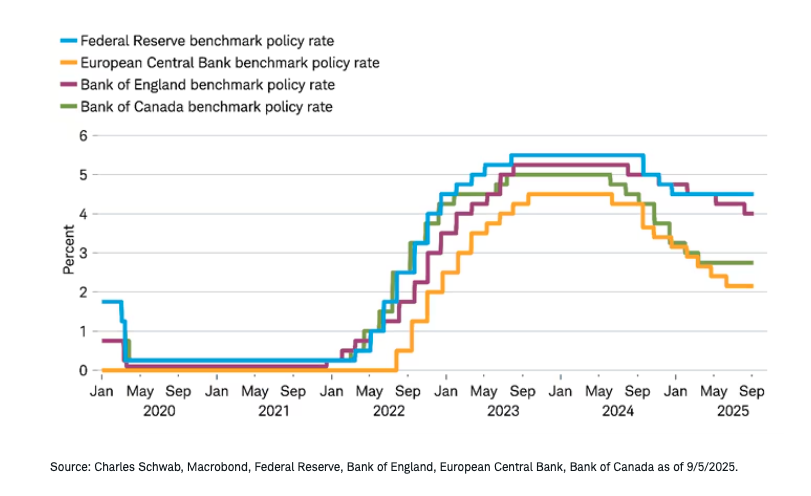

Central bank policy rates moving at different paces

Going forward, markets are expecting further rate cuts by all major central banks except the Bank of Japan.

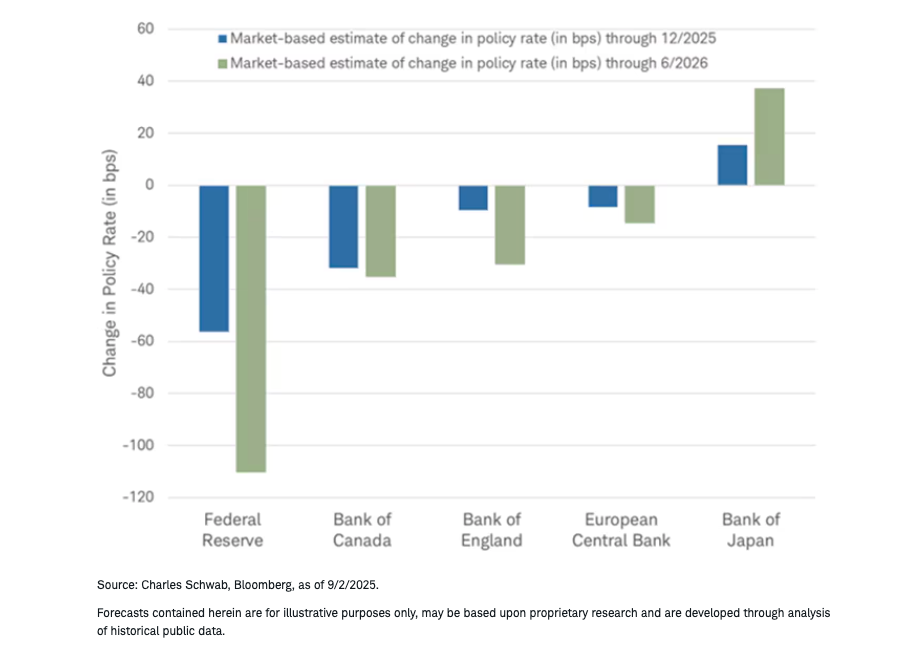

Market expectations for future central bank policy rates

- The potential for U.S. economic growth to slow has prompted markets to forecast an acceleration in rate cuts.

- Canada's economy contracted by 1.6% in the second quarter. Combined with temporary factors boosting inflation, the Bank of Canada may continue to cut rates.

- Markets may be expecting the Bank of England to continue to cut rates, but wages grew 5% in the second quarter due in part to a tight labor market, which could constrain further tightening.

- The European Central Bank (ECB) may be at or near the end of rate cuts, having made progress both on inflation and reducing the policy rate. Economic weakness or downside risks to inflation could prompt another rate cut but an acceleration in the economy or inflation could keep the ECB on hold.

- The Bank of Japan stands alone in hiking rates, emerging from 30 years of deflation with its first rate hike of 17 years in March 2024. Further hikes will likely depend on wage growth keeping up with inflation, with eyes on annual union demands in November and December.

The diverging trends and country-specific factors mean investors cannot generalize the direction in either inflation or monetary policy. In isolation, more rate cuts for the U.S. relative to the rest of the world could keep downward pressure on the U.S. dollar, which could boost returns for international stocks.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate this risk.

Currency trading is speculative, volatile and not suitable for all investors.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Investment and Insurance Products: Not a Deposit • Not FDIC Insured • Not Insured by any Federal Government Agency • No Bank Guarantee • May Lose Value

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co. Inc. (Member SIPC), and its affiliates offer investment services and products. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All