Additional content provided by Brian Booe, Associate Analyst, Research.

With just a week remaining until the highly anticipated September Federal Open Market Committee (FOMC) meeting, Wednesday’s wholesale inflation print and Thursday’s consumer inflation results for August are the last major hurdles lying between the expected resumption of the FOMC easing cycle. Fed fund futures have fully priced a 0.25% rate reduction next Wednesday — and are currently priced for a full percentage point of easing before Federal Reserve (Fed) Chair Jerome Powell’s term ends in May (with roughly two-thirds of this priced in for 2025). Baring the unlikely chance Fed Chair Powell warns of a recession or outsized urgency around the labor market, U.S. equities are likely poised to build on year-to-date gains should central bankers deliver on Powell’s hint of a policy change at Jackson Hole last month.

Dry Powder for Wall Street Bulls?

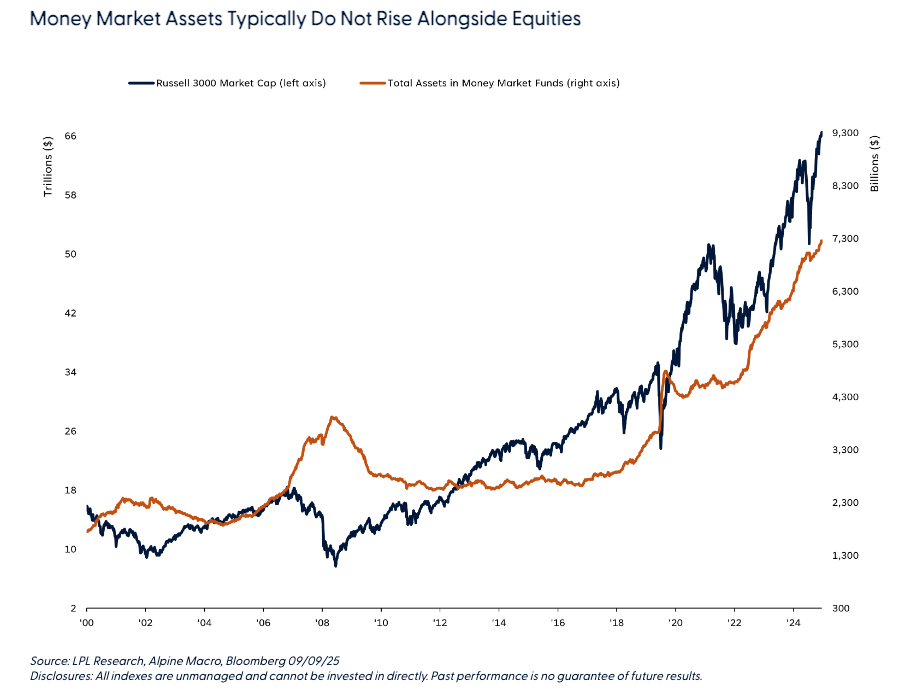

In addition to strong corporate profits, fiscal policy, and a resilient economy, potential rate cuts could be a necessary catalyst for stocks to extend their rally off April 8 lows as rate cuts historically are stimulative for stocks absent a recession (as we noted in our September 8 Weekly Market Commentary). As an honorable mention to these direct themes underpinning the future of the bull market, the resumption of the monetary policy easing cycle could also provide additional longer-term tailwinds for equity markets under the surface. Assets in money market funds have been on the rise since 2022, and if rate reductions are delivered roughly on pace with market expectations, this capital currently on the sidelines is likely to be called into the big game. The meaningful move lower in rates currently priced in would shift the arithmetic around money market funds, diminishing earnings and potentially leading investors to re-deploy capital — ending the unusual trend of money market assets rising alongside equity prices. As shown in the “Money Market Assets Typically Do Not Rise Alongside Equities” chart, rises in the market cap of the Russell 3000 Index (which represents roughly 98% of the investable U.S. equity market) tends to correlate with declining or stable levels of money market fund assets. This has not been the case since 2022 due to the Fed’s rate hiking cycle and “higher-for-longer” stance, which increased the attractiveness of money market funds.

Money Market Assets Typically Do Not Rise Alongside Equities

Paired with U.S. equity positioning still only moderately above neutral relative to developed and emerging markets following this spring’s so-called “tariff tantrum” selling, elevated and rising money market funds indicate that investors may not be fully invested — suggesting next Wednesday’s Fed rate decision could be an early domino to fall in igniting additional support for the bull market. However, the effects of investors potentially re-deploying to the market would not be felt overnight, potentially taking multiple rate cuts for a meaningful impact. Plus, it’s worth noting that the amount of capital in money market funds as a percent of U.S. market cap has remained rangebound over the same time, also serving as a reminder that the unprecedented acceleration in market cap powered by a handful of index heavyweights presents concentration risks that should not be ignored. For example, NVIDIA’s (NVDA) market cap is now larger than the entire listed stock exchanges of all nations outside of the U.S., China, Japan, and India.

Conclusion

The bull market likely has more left in the tank, and there is a notable amount of capital available to be put to work when the Fed resumes its rate cutting cycle, potentially acting as dry power for U.S. investors. Volatility will come at some point, as macro headwinds such as sticky inflation (with more tariffs on the way) should not be ignored and potential geopolitical shocks remain on the table. Nonetheless, we expect the path of least resistance for U.S. equities to be higher over the longer-term (with intermittent volatility), supported by Fed rate cuts, moderate but steady economic growth poised to pick up next year, stable long-term interest rates as inflation normalizes, and the powerful ongoing AI capital investment cycle.

The LPL Research Strategic and Tactical Asset Allocation Committee (STAAC) maintains its tactical neutral stance on equities. Investors may be well served by bracing for occasional bouts of volatility given how much optimism is reflected in stock valuations, lingering tariff and inflation risks, and historical seasonal weakness. LPL Research advises against increasing portfolio risk beyond benchmark targets currently and continues to monitor trade negotiations, economic data, earnings, the bond market, and various technical indicators to identify a potentially more attractive entry point to potentially add equities on weakness.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

Read more commentaries by LPL Financial