Janus Henderson’s Multi-Asset Quarterly Report - Q3 2025

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMacro overview

- Economic uncertainty remains as investors await to see whether U.S. economic resilience and the potential stimulative benefits of the Big Beautiful Bill can overcome the headwinds of renewed tariff threats.

- Squaring an uncertain backdrop with elevated equity valuations is a challenging proposition but with scant signs of material economic weakening, we believe one should stay invested and maintain vigilance.

- Diversification should be prioritized in this environment with healthy core fixed income yields, alternative assets, and global equities presenting opportunities for uncorrelated returns.

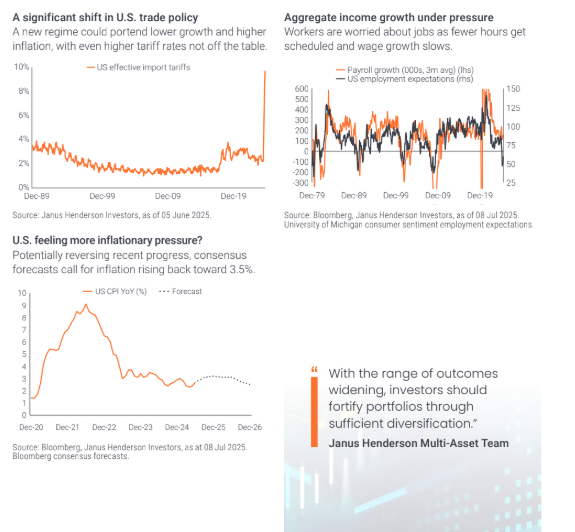

Judging by soaring asset valuations in the wake of President Trump backing away from the worst-case tariff scenario, one could believe that the threat posed by upending the global trade framework has been removed. We are more circumspect. Although softening inflation and jobs data may provide the Federal Reserve (Fed) cover to resume growth-supporting rate cuts, we believe policy could remain on hold until better economic and policy clarity emerges. With the range of outcomes widening, investors should fortify portfolios through sufficient diversification.

Equities

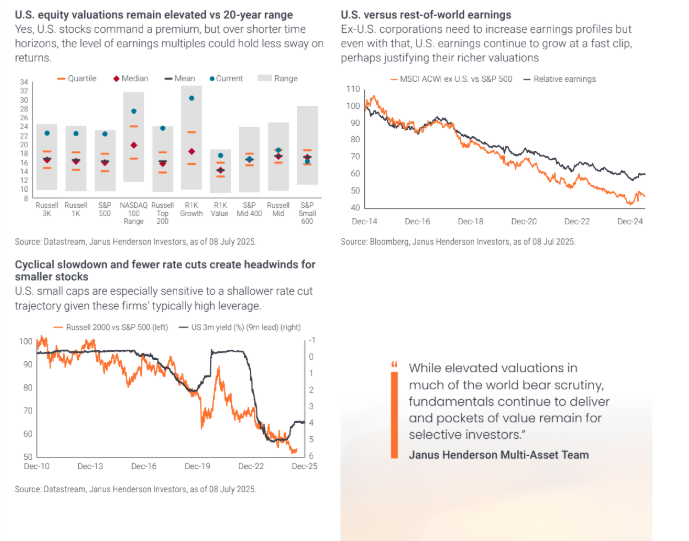

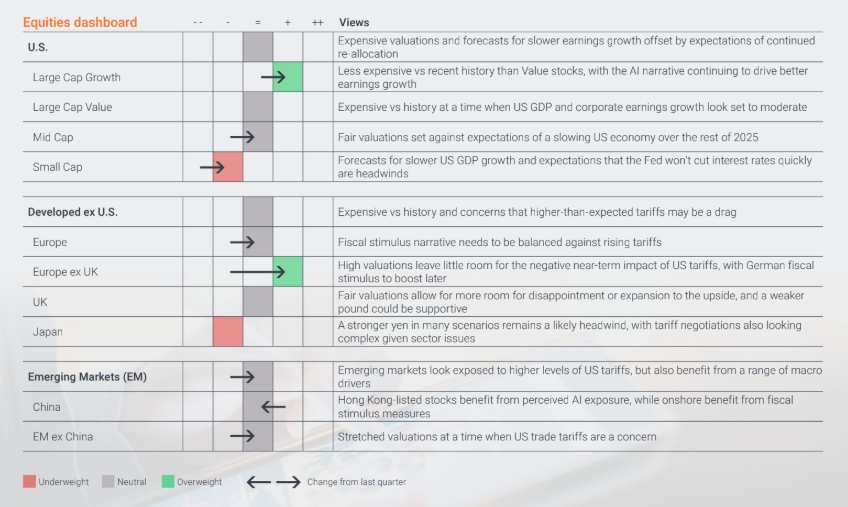

- With valuations high across equities, investors should seek to identify which market segments may justify their premiums.

- U.S. tech stocks’ record of superior earnings growth amid economic uncertainty means the segment could resume its market dominance.

- Thanks to fiscal stimulus, domestic-focused Chinese stocks represent a rare value play and diversification to the dominant tech-centric growth theme.

Top-quartile valuations across global equities should give investors pause but the deceleration in aggregate earnings growth has been less than feared and tech-heavy growth earnings continue to deliver upgrades. While high valuations mean broader equities merit a balanced view, U.S. small-caps’ prospects have improved on stimulative legislation but lingering high interest rates represent a headwind. European valuations have taken the luster off the region’s rally, leaving China as perhaps a unique source of value in the current environment.

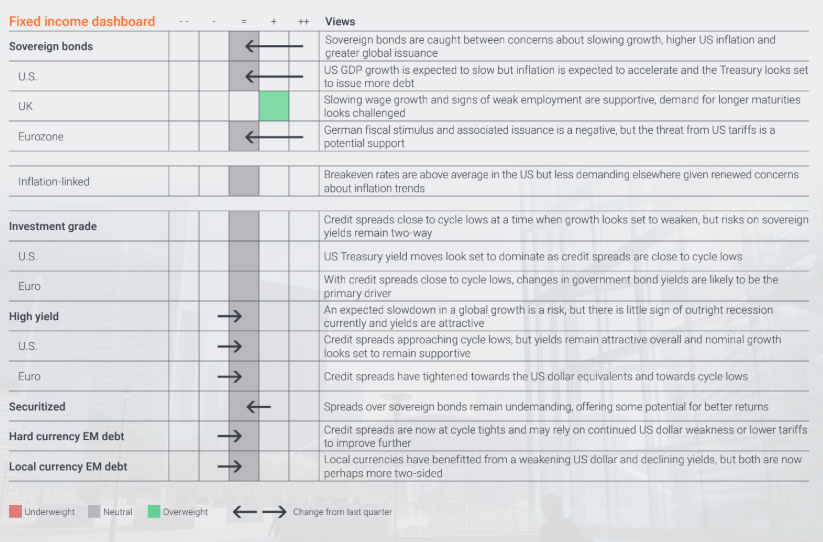

Fixed Income

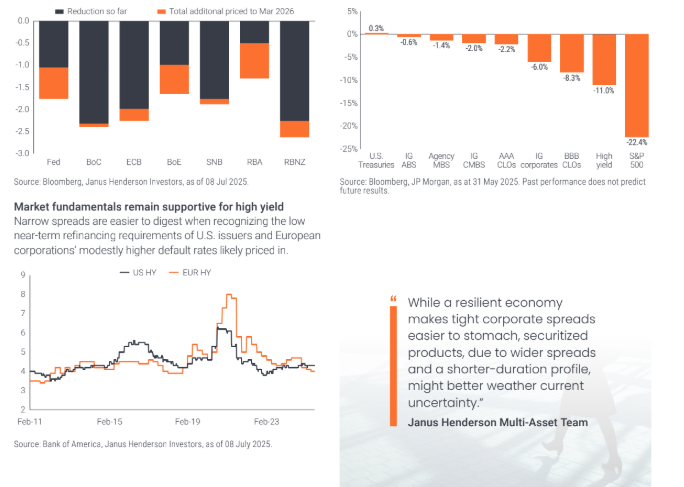

- Softening labor markets and slowing inflation create a favorable environment for bonds but beware the stagflationary risk posed by tariffs.

- Credit spreads are tight but with absolute yields high and the economic cycle extending, these conditions can persist longer than expected.

- The staggered cadence of monetary easing creates opportunities for global investors to harvest yields and participate in capital appreciation.

While tariff policy uncertainty impeded the Fed in following the European Central Bank, among others, by cutting rates into a slowing economy, an eventual resumption of cuts could buoy Treasuries. While a resilient economy makes tight corporate spreads easier to stomach, securitized products, due to their shorter-duration profile, are better placed to weather current uncertainty. Diversification within bonds is possible by adopting a global mindset.

Fed now expected to make two 25 bps rate cuts in 2025

The Bank of England has also been reticent to cut rates given the UK’s sticky inflation while the European Central Bank has been among the most aggressive easers.

U.S. securitized debt: Strength in the face of adversity

Average peak-to-trough returns of the five most recent equity market corrections/bear markets, with corresponding returns for various fixed-income sectors.

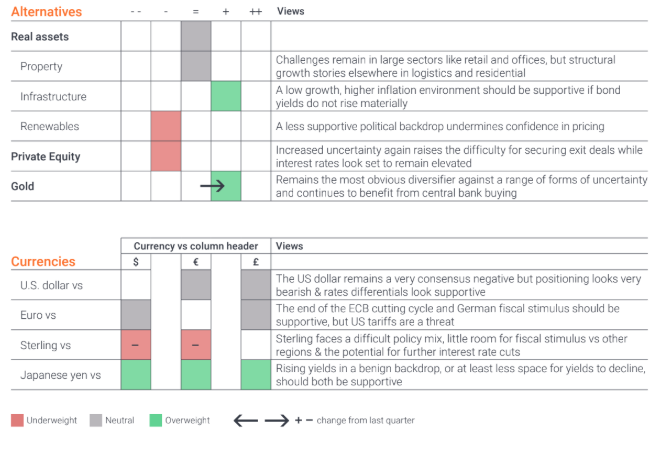

Alternatives and currencies

- Alternative assets including gold – despite its rally – present an opportunity to diversify away from equities and bonds while geopolitical and tariff uncertainty persists.

- However, modestly lower geopolitical risk should dampen the rally in other commodities, temporarily diminishing their efficacy as a diversifier.

- Given its precipitous 2025 decline – and reserve currency role – it’s difficult to envision the U.S. dollar losing much additional ground.

With most economies potentially late cycle in nature, the possible emergence of stagflation complicates investors’ ability to diversify portfolios. Rather than hedging risk assets with sovereign exposure, the left-tail risk posed by trade barriers means traditional risk management with duration should be diversified with alternative assets that offer low correlations to both equities and bonds. Within currencies, while monetary policy will influence U.S. dollar returns, current low levels renew the greenback’s appeal as a safe haven.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Definitions, Indices, & Risks

Definitions

10-Year Treasury Yield is the interest rate on U.S. Treasury bonds that will mature 10 years from the date of purchase.

Agency mortgage-backed securities (MBS): A security which is secured (or ‘backed’) by a collection of mortgages. Investors receive periodic payments derived from the underlying mortgages, similar to the coupon on bonds.

Asset-backed securities (ABS): A financial security that is ‘backed’ (or collateralised) with existing assets (such as loans, credit card debts or leases), usually ones that generate some form of income (cash flow) over time.

Collateralized loan obligations (CLOs): A bundle of generally. lower quality leveraged loans to companies that are grouped together into a single security, which generates income (debt payments) from the underlying loans.

Commercial mortgage-backed securities (CMBS): Fixed-income securities backed by a pool of commercial mortgage loans.

Consumer price index (CPI): A measure that examines the price change of a basket of consumer goods and services over time. It is used to estimate inflation.

Correlation: How far the price movements of two variables (eg. equity or fund returns) move in relation to each other. A correlation of +1.0 means that both variables have a strong association in the direction they move. If they have a correlation of -1.0, they move in opposite directions. A figure near zero suggests a weak or non-existent relationship between the two variables.

Credit spread: The difference in yield between securities with similar maturity but different credit quality, often used to describe the difference in yield between corporate bonds and government bonds. Widening spreads generally indicate a deteriorating creditworthiness of corporate borrowers, while narrowing indicate improving.

Cyclical: Sensitive to changes in the economy. In the case of stocks, that would include companies that sell discretionary consumer items (such as cars), or highly correlated to demand (eg. mining).

Default rate measures the failure of debtors (such as a bond issuer) to pay interest or to return an original amount loaned when due.

Diversification: A way of spreading risk by mixing different types of assets/asset classes in a portfolio, on the assumption that these assets will behave differently in any given scenario.

Duration measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates and vice versa.

Earnings per share (EPS): EPS is the bottom-line measure of a company’s profitability, defined as net income (profit after tax) divided by the number of outstanding shares.

Fiscal/Fiscal policy: Describes government policy relating to setting tax rates and spending levels. Fiscal policy is separate from monetary policy, which is typically set by a central bank.

Forward earnings: An estimate of the future earnings of a business, usually covering the present financial year or the next one.

High yield bond: Also known as a sub-investment grade bond, or ‘junk’ bond. These bonds usually carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher interest rate (coupon) to compensate for the additional risk.

Investment-grade bond: A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

Late cycle refers to the final phase of an economic cycle before a recession. Economic activity often reaches its peak and growth slows but remains positive.

Monetary Policy refers to the policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money.

Monetary stimulus refers to a central bank increasing the supply of money and lowering borrowing costs. Monetary tightening refers to central bank activity aimed at curbing inflation and slowing down growth in the economy by raising interest rates and reducing the supply of money.

Private assets are investments that are not publicly traded or listed on a public stock exchange.

Purchasing Managers’ Index (PMI) is a survey that acts as a leading insight into the prevailing direction of economic trends, based on the view of managers across 19 industries. The index is based on five indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

Ratings/Credit quality ratings are measured on a scale that generally ranges from AAA (highest) to C (lowest).

Real assets are tangible investments, such as gold, real estate, or oil, that have an intrinsic value due to their substance and physical properties.

Recession: A sustained decline in economic activity, usually perceived as two consecutive quarters of economic contraction.

Safe-haven: An asset that is expected to retain its value or potentially even gain value, during periods of economic uncertainty or market turbulence, eg. gold, US government debt, the US dollar, cash, etc.

Spreads/Credit Spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthinessof corporate borrowers, and narrowing indicate improving.

Tariffs: A tax or duty imposed by a government on goods imported from other countries.

Volatility: The rate and extent at which the price of a portfolio, security, or index, moves up and down. If the price swings up and down with large movements, it has high volatility. If the price moves more slowly and to a lesser extent, it has lower volatility. The higher the volatility the higher the risk of the investment.

Yield: The level of income on a security over a set period, typically expressed as a percentage rate. For equities, a common measure is the dividend yield, which divides recent dividend payments for each share by the share price. For a bond, this is calculated as the coupon payment divided by the current bond price.

Indices

Citigroup Economic Surprises Index measures how economic data compares to market expectations.

MSCI China IndexTM reflects the equity market performance of China.

MSCI Emerging Markets Index reflects the equity market performance of emerging markets.

MSCI Europe Index reflects the equity market performance of developed markets in Europe.

MSCI Japan Index reflects the performance of large and mid-cap companies in the Japanese market.

NASDAQ 100 Index is made up of equity securities issued by 100 of the largest non-financial companies listed on the NASDAQ stock exchange in the U.S.

The Russell 1000 / 2000 / 3000 indices measure the performance of the largest 1000, 2000 and 3000 companies in the US, by market capitalization.

Russell 1000® Growth Index reflects the performance of U.S. large-cap equities with higher price-to-book ratios and higher forecasted growth values.

Russell 1000® Value Index reflects the performance of U.S. large-cap equities with lower price-to-book ratios and lower expected growth values.

Russell Midcap® Index reflects the performance of U.S. mid-cap equities.

Russell Top 200® Index measures the performance of the 200 largest companies in the Russell 1000 Index.

S&P 500® Index reflects U.S. large-cap equity performance and represents broad U.S. equity market performance.

S&P Mid Cap 400® Index measure the performance of the mid-range sector of the U.S. stock market.

S&P Small Cap 600® Index measure the performance of selected U.S. stocks with a small market capitalization.

Risks

Investing involves risk, including the possible loss of principal and fluctuation of value.

Alternative investments include, but are not limited to, commodities, real estate, currencies, hedging strategies, futures, structured products, and other securities intended to be less correlated to the market. They are typically subject to increased risk and are not suitable for all investors.

Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Equity securities are subject to risks including market risk. Returns will fluctuate in response to issuer, political and economic developments. Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets.

Fixed income securities are subject to interest rate, inflation, credit and default risk. As interest rates rise, bond prices usually fall, and vice versa. High-yield bonds, or “junk” bonds, involve a greater risk of default and price volatility. Foreign securities, including sovereign debt, are subject to currency fluctuations, political and economic uncertainty and increased volatility and lower liquidity, all of which are magnified in emerging markets.

Growth and value investing each have their own unique risks and potential for rewards, and may not be suitable for all

investors. Growth stocks are subject to increased risk of loss and price volatility and may not realize their perceived growth potential. Value stocks can continue to be undervalued by the market for long periods of time and may not appreciate to the extent expected.

Inflation-linked bonds feature adjustments to principal based on inflation rates. They typically have lower yields than conventional fixed-rate bonds and decline in price when real interest rates rise.

Real estate securities, including Real Estate Investment Trusts (REITs), are sensitive to changes in real estate values and rental income, property taxes, interest rates, tax and regulatory requirements, supply and demand, and the management skill and creditworthiness of the company. Additionally, REITs could fail to qualify for certain tax-benefits or registration exemptions which could produce adverse economic consequences.

Securitized products, such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation, and liquidity risk than other fixed-income securities.

Smaller capitalization securities may be less stable and more susceptible to adverse developments, and may be more volatile and less liquid than larger capitalization securities.

Sovereign debt securities are subject to the additional risk that, under some political, diplomatic, social or economic circumstances, some developing countries that issue lower

quality debt securities may be unable or unwilling to make principal or interest payments as they come due.

Important information

References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned.

The views presented are as of the date published. They are for information purposes only and should not be used or construed as investment, legal or tax advice or as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. Nothing in this material shall be deemed to be a direct or indirect provision of investment management services specific to any client requirements. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent, are subject to change and may not reflect the views of others in the organization. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. No forecasts can be guaranteed and there is no guarantee that the information supplied is complete or timely, nor are there any warranties with regard to the results obtained from its use. Janus Henderson Investors is the source of data unless otherwise indicated, and has reasonable belief to rely on information and data sourced from third parties. Past performance does not predict future returns. Investing involves risk, including the possible loss of principal and

fluctuation of value. Not all products or services are available in all jurisdictions. This material or information contained in it may be restricted by law, may not be reproduced or referred to without express written permission or used in any jurisdiction or circumstance in which its use would be unlawful. Janus Henderson is not responsible for any unlawful distribution of this material to any third parties, in whole or in part. The contents of this material have not been approved or endorsed by any regulatory agency. Janus Henderson Investors is the name under which investment products and services are provided

by the entities identified in the following jurisdictions: (a) Europe by Janus Henderson Investors International Limited (reg no. 3594615), Janus Henderson Investors UK Limited (reg. no. 906355), Janus Henderson Fund Management UK Limited (reg. no. 2678531), (each registered in England and Wales at 201 Bishopsgate, London EC2M 3AE and regulated by the Financial Conduct Authority), Tabula Investment Management Limited (reg. no. 11286661 at 10 Norwich Street, London, United Kingdom, EC4A 1BD and regulated by the Financial Conduct Authority) and Janus Henderson Investors Europe S.A. (reg no. B22848 at 78, Avenue de la Liberté, L-1930 Luxembourg, Luxembourg and regulated by the Commission de Surveillance du Secteur Financier); (b) the U.S. by SEC registered investment advisers that are subsidiaries of Janus Henderson Group plc; © Canada through Janus Henderson Investors US LLC only to institutional investors in certain jurisdictions; (d) Singapore by Janus Henderson Investors (Singapore) Limited (Co. registration no. 199700782N). This advertisement or publication has not been reviewed by Monetary Authority of Singapore; (e) Hong Kong by Janus Henderson Investors Hong Kong Limited. This material has not been reviewed by the Securities and Futures Commission of Hong Kong; (f) South Korea by Janus Henderson Investors (Singapore) Limited only to Qualified Professional Investors (as defined in the Financial Investment Services and Capital Market Act and its sub-regulations); (g) Japan by Janus Henderson Investors (Japan) Limited, regulated by Financial Services Agency and registered as a Financial Instruments Firm conducting Investment Management Business, Investment Advisory and Agency Business and Type II Financial Instruments Business; (h) Australia and New Zealand by Janus Henderson Investors (Australia) Limited (ABN 47 124 279 518) and its related bodies corporate including Janus Henderson Investors (Australia) Institutional Funds Management Limited (ABN 16 165 119 531, AFSL 444266) and Janus Henderson Investors (Australia) Funds Management Limited (ABN 43 164 177 244, AFSL 444268); (i) the Middle East by Janus Henderson Investors International Limited, regulated by the Dubai Financial Services Authority as a Representative Office. This document relates to a financial product which is not subject to any form of regulation or approval by the Dubai Financial Services Authority (“DFSA”). The DFSA has no responsibility for reviewing or verifying any prospectus or other documents in connection with this financial product. Accordingly, the DFSA has not approved this document or any other associated documents nor taken any steps to verify the information set out in this document, and has no responsibility for it. The financial product to which this document relates may be illiquid and/or subject to restrictions on its resale. Prospective purchasers should conduct their own due diligence on the financial product. If you do not understand the contents of this document you should consult an authorised financial adviser. No transactions will be concluded in the Middle East and any enquiries should be made to Janus Henderson. We may record telephone calls for our mutual protection, to improve customer service and for regulatory record keeping purposes.

Outside of the U.S., Australia, Singapore, Taiwan, Hong Kong, Europe and UK: For use only by institutional, professional, qualified and sophisticated investors, qualified distributors, wholesale investors and wholesale clients as defined by the applicable jurisdiction. Not for public viewing or distribution. Marketing Communication.

Janus Henderson is a trademark of Janus Henderson Group plc or one of its subsidiaries. © Janus Henderson Group plc.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All