Many companies say they pay dividends because it’s what their shareholders want. Yet CFOs of the same companies also typically tell us they only allocate capital to maximize shareholder returns. In today’s markets, these two points are often at odds and may create a conundrum for income-seeking equity investors.

Dividends are widely seen as a dependable source of income and are typically associated with strong equity performance. But conventional wisdom about dividends can be simplistic. High payouts today mean less cash to support future business growth, which could erode earnings and share-price return potential. Investors seeking equity income can resolve this quandary by understanding the dynamics of dividends, which can be traced back to their rising appeal 60 years ago.

A Brief History of Modern Dividends

At the beginning of the 1960s, powerful regional monopolies began to emerge across multiple sectors, including banking, energy, media and telecoms. These regional giants dominated their markets and enjoyed the benefits of local scale that eclipsed all competitors.

With healthy revenue and profit growth—and little incremental investment—these monopolies could distribute large sums of cash to shareholders (often including themselves) via the only route possible: dividends. At the time, share buybacks didn’t exist—they were only legalized in 1982 in the US and much later in Europe (Denmark only allowed buybacks in 2006). This golden age of dividend investing reigned supreme for years.

More than three decades later, the birth of the internet shook the foundation of dividend culture. In August 1995, Netscape went public. Despite generating just $1.4 million in revenue, Netscape ended its first trading day with a market cap of nearly $3 billion. The dot-com bubble had begun.

While the market madness lasted only six years, Netscape’s launch marked the start of the commercialization of the internet, which signaled the beginning of the end for most regional monopolies. Monopolists could no longer compete purely on a regional basis because what was once scarce had now become abundant and what was once local had become global. The game had changed.

The Reinvestment Requirement for Growth

In a world of abundance and global competition, the importance of reinvesting in a business became paramount for companies and their shareholders. Companies that do not or cannot reinvest back into their business face stagnation at best, oblivion at worst.

This explains why equities are one of very few assets that can grow without requiring significant reinvestment by investors. Cash is whittled away by inflation, bonds must be reinvested, and property needs constant maintenance. A stock’s value, however, may continue to grow completely untouched. The reason? Someone else is doing the investment for you—the underlying company.

Fast forward to 2025, and a new market force is redefining dividend dynamics. Passive assets that track indices are now the dominant force in markets, with AUM surpassing that of active managers. This shift in power has spurred a subtle change in markets that has upended the classic investing adage of buy low, sell high.

Indeed, the opposite is now true, because most indices are market-cap weighted. All else being equal, if a company’s share price falls, its market cap and index weight decline; vice versa when a share price rises. As a result, the weight of money in the market will buy stocks that go up and sell stocks that go down. In other words, buy high, sell low has become commonplace today.

The Interplay Between Dividends, Earnings and Share Prices

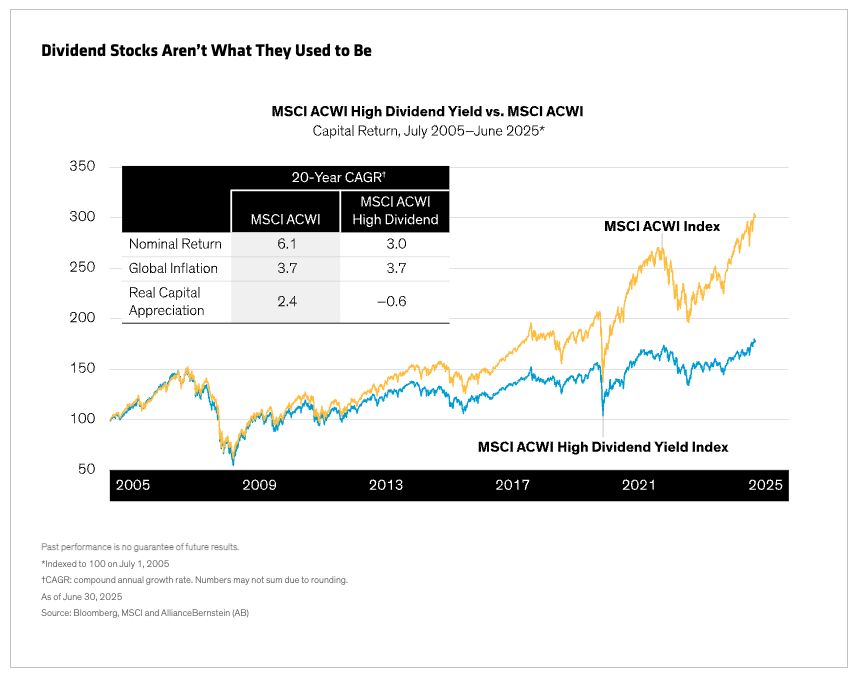

New market dynamics have changed the calculus for dividends, which aren’t necessarily aligned with strong stock performance anymore (Display). Yet many investors still like a dividend because it’s widely believed that by spending our dividends, we are protecting our capital. Sadly, in today’s world that’s not always true.

While not all dividends are bad, income-seeking investors should be mindful of three points that govern the relationship between dividends, earnings and share prices.

- Companies that fail to adequately reinvest in their business are likely to see a decline in their earnings over the long term. When earnings fall, share prices will follow.

- Paying a dividend mechanically causes a share price to fall. That’s because a company’s value is based on its profits and net assets, which naturally decline when cash exits the business to pay a dividend.

- In today’s passive-dominated markets, falling share prices can be self-perpetuating.

Growth and Income: Trade-offs for Equity Income Success

So why do companies really pay dividends? In our eyes, the only acceptable answer to that question is because a company’s stock price is too high to justify a buyback. However, no CEO or CFO would ever admit that. All too often, dividend-paying companies are loath to cut payouts for fear of alienating shareholders, even if it would be best for the health of the business.

That said, people and organizations need their assets to generate an income. And despite their shortcomings, equities are uniquely positioned to do that over the long term.

Here’s the good news: despite the challenges, there is a way to generate equity income and protect the real value of one’s capital or even grow it over time. But to achieve this, certain trade-offs must be made.

First, investors should be willing to accept a low-percentage dividend yield today. This enables one to invest in businesses that are reinvesting to drive long-term earnings growth. Second, invest in companies that don’t pay a dividend today. While that may sound surprising, removing this impediment provides access to some of the world’s best businesses that offer capital protection and growth for years to come as well as future dividend potential. Third, forego diversification. Since very few businesses can sustain high dividends and earnings growth over time, we think investors may be risking their capital by broadening an allocation in the name of risk management.

These points may sound counterintuitive to traditional equity income strategies that focus primarily on high dividend yields. But as we see it, a disciplined search for select businesses that compound free cash flow can deliver higher dividends and capital growth over time. It’s a recipe for a better balance of growth and income that disentangles the dividend dilemma facing companies—and investors—in today’s tricky market conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams, and are subject to change over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

© AllianceBernstein

Read more commentaries by AllianceBernstein