On Firmer Ground?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMarkets have been encouraged so far this year by relatively steady U.S. nonfarm payroll data, but White House tariff policy remains a moving target. On the positive side of the ledger, tariff rates are down significantly from the April 2nd "Liberation Day" levels—but on the other hand, trade negotiations are ongoing, as is the uncertainty.

Bond markets have calmed, but it may be a temporary quiet period. The tariff deadline was extended to August 1st, keeping uncertainty simmering, and the speculation about when the Federal Reserve will lower the federal funds rate will heat up as fall approaches.

Meanwhile, governments around the globe are finding it difficult to cut deficits, leading to political friction and rising bond yields in some countries.

U.S. stocks and economy: A change is gonna come?

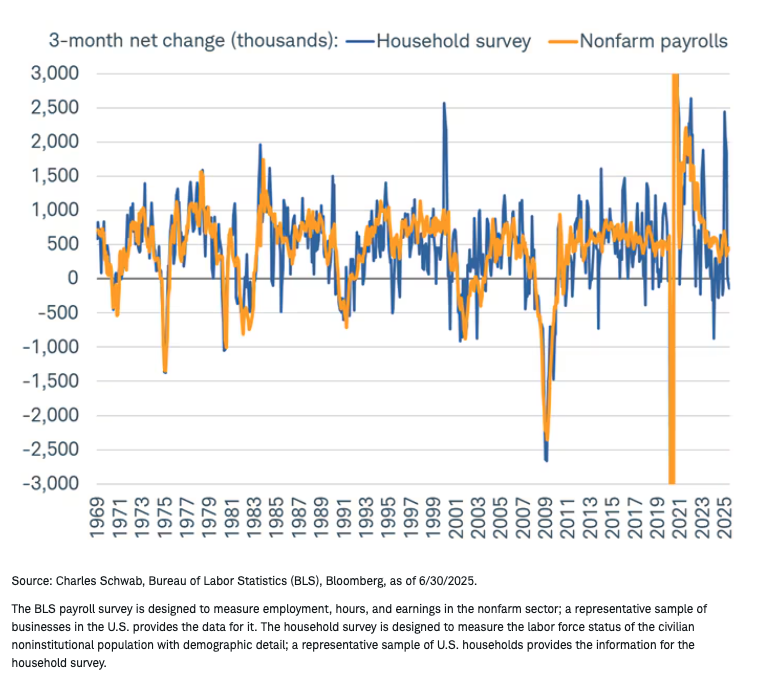

As we begin the second half of the year, the economy remains on somewhat firm ground, but not without some potential tremors under the surface. We think the strongest tell for how growth will hold up will be the state of the labor market. At the midway point of 2025, labor looked to be in a solid position based on nonfarm payroll growth. As shown in the chart below, the three-month change in payrolls has eased considerably over the past few years but has also stabilized at a level consistent with prior economic expansions. More volatile has been the household survey, from which the unemployment rate is calculated.

Payrolls tell a solid story

Speaking of the unemployment rate, its drop in June—to 4.1% from 4.2%—was perhaps the most notable development in the June jobs report. To be sure, the decline was for the "wrong" reason in that the contraction in the labor force was quite large. That may not necessarily continue, but a continued deterioration would be a worrisome sign for the economy. For now, though, the upside is that the upward momentum in the unemployment rate has halted.

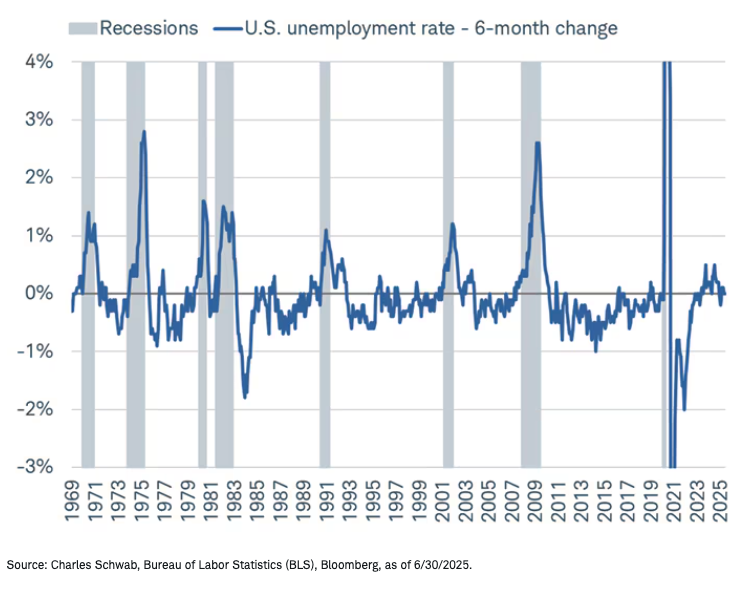

As shown in the chart below, the six-month change in the unemployment rate gathered steam last year—at times, to levels consistent with what we've seen at the start of prior recessions. Fortunately, that momentum has stalled out, with the unemployment rate essentially unchanged over the past six months. That is rare to see in history, as unemployment is typically falling or rising as opposed to holding steady.

Unemployment rate's rise stalls out

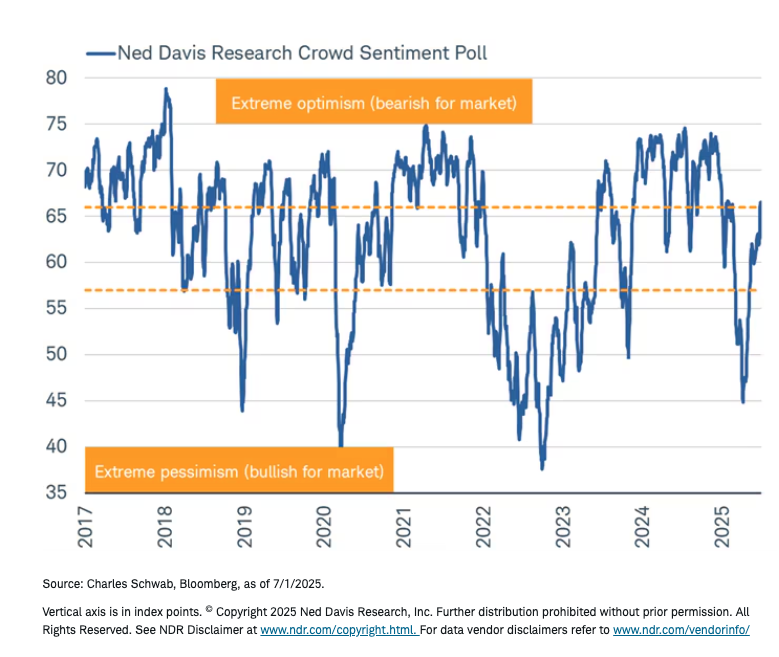

The stock market has reacted positively to the resilience of the labor market but has unquestionably been driven more by Washington policy this year. As of this writing, the Trump administration is still working through several negotiations with countries, which means the average U.S. tariff rate continues to be a moving target. Amid drawn-out negotiations, the market has reacted favorably to the fact that tariff rates have come down from "Liberation Day" levels, evidenced by the significant snapback in investor sentiment.

As shown in the chart below, Ned Davis Research's Crowd Sentiment Poll (CSP) has crept back into "extreme optimism" territory. Historically, that is the weakest zone for the market, but history also suggests that sentiment can get increasingly "frothy" from here—not least because the CSP has only recently crossed into "extreme optimism" territory.

The crowd grows louder

With sentiment, it's always worth reminding investors that extreme bouts of optimism can make stocks more vulnerable to a negative catalyst. Policies from Washington have mostly been consistent catalysts this year, but we would add the labor market as one to watch in the back half of the year—especially if the labor force continues to deteriorate.

Fixed income: Calm between the storms?

Bond markets have settled down after volatility sparked by the budget bill, the Federal Reserve meeting, and tariff uncertainty. Treasury yields currently are about unchanged from a month ago; however, the U.S. dollar continues to trend steadily lower.

We view the bond market's recent steadiness as the calm between the storms. The July 9th tariff deadline has been extended, which will keep uncertainty elevated. The Fed is on hold for now—but the guessing game about when it will lower the federal funds rate is bound to continue. Currently the market is expecting one rate cut in 2025 and a three to four more in 2026. However, inflation will need to get closer to the Fed's 2% target to justify a rate cut—something that may prove difficult with the prospect of tariffs still on the horizon and a sinking dollar.

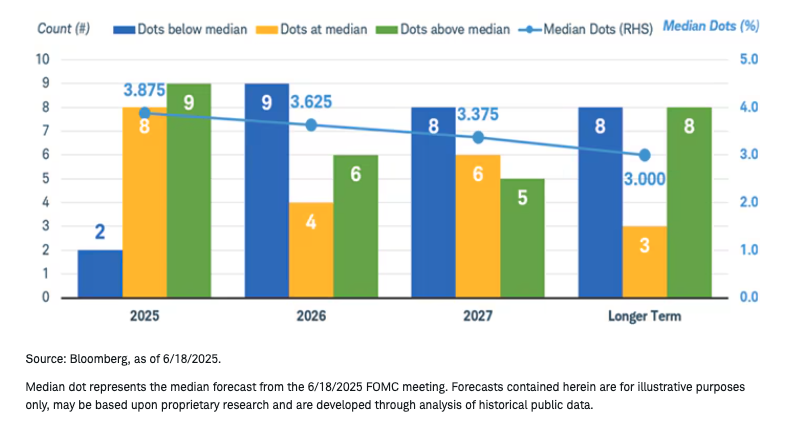

At the July Federal Open Market Committee (FOMC) meeting the median projection was for two rate cuts by year-end. However, the committee's views were clearly divided. Seven members projected that there would be no rate cuts this year and two projected just one cut. The bar for rate cuts at the Fed appears to be high.

Fed members are projecting two rate cuts this year

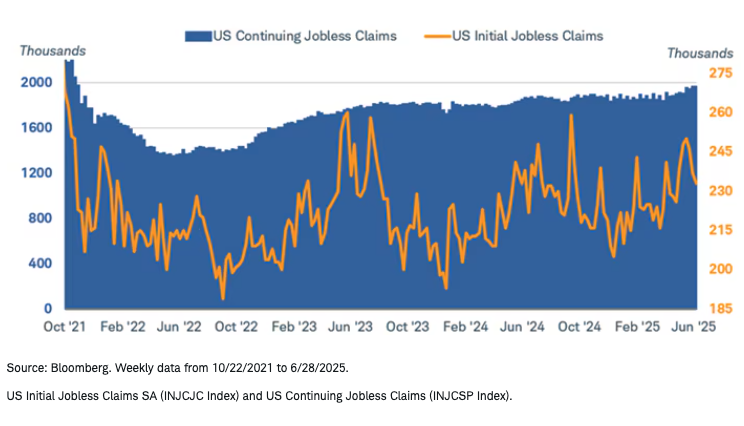

We expect the labor market will provide the catalyst for a rate cut later this year. While job growth has been resilient, it has slowed. The ripple effect of federal spending cuts for various agencies and private institutions is likely to mean a weaker job market in the fall. Layoff announcements have increased and the steady rise in continuing unemployment claims suggests that workers that have been laid off are having difficulty finding new jobs. We would expect the Fed to respond to weakness in the labor market with a rate cut by the September meeting.

Continuing jobless claims have been elevated

In the meantime, we are keeping a close eye on the dollar. It has fallen by about 10% on a trade-weighted basis, which can add to inflation pressure. A weaker dollar makes the cost of imported goods rise. Since the U.S. is a large net importer, the downtrend in the dollar can have a significant effect on inflation.

The dollar has declined in recent months

For investors, the good news is that real interest rates—those adjusted for inflation—are attractive. Real 10-year Treasury yields are near 2%, holding well above levels seen in the past 15 years. Investors are getting compensated for inflation risk.

The push-pull between slower growth and inflation likely will continue into the fall. We continue to suggest keeping an average portfolio duration in the five- to seven-year vicinity but may consider adding duration down the road, if the inflation outlook improves. We are keeping a close eye on the labor market for a signal of an approaching Fed rate cut and the dollar for potential inflation risk.

International stocks and economy: Fixing deficits is unpopular

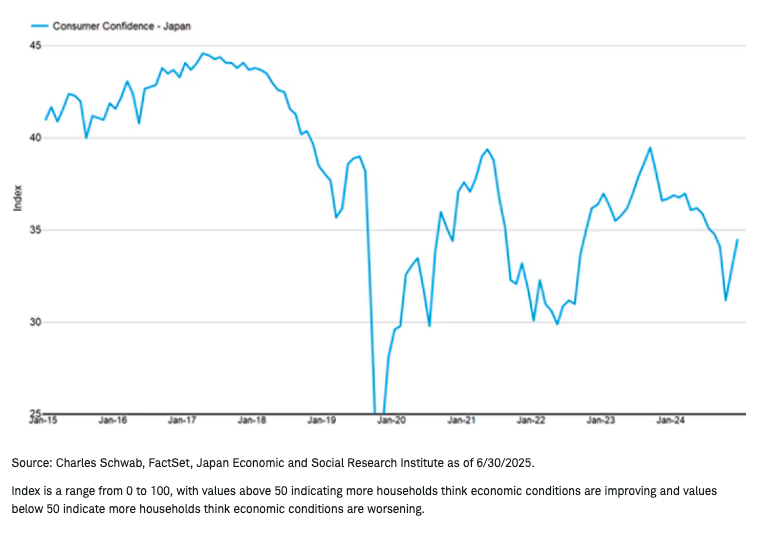

Politicians typically have an easier time adding government spending than taking it away, yet years of high deficits is requiring tough decisions. Take the case of Japan. Japan's economy is being transformed by the existence of inflation after 30 years of deflation. Although deflation is harmful to economic growth through consumption delays triggered by anticipation of lower prices, inflation without high enough wage increases can also suppress consumption.

The COVID-19 pandemic resulted in global inflation and in Japan, wages started rising for the first time in decades. The hope is that with higher wages, consumers might spend more, stimulating economic activity. The problem? Wages have not risen enough to overcome inflation in Japan, and consumers seem to be losing patience—and blaming politicians.

Japan's consumer confidence remains relatively weak

The October 2024 election saw seat losses by the Liberal Democratic Party (LDP) and Japan's ruling coalition government is facing the potential for more losses in an upper house election on July 20. The prospect of losing power may result in pressure on the LDP to cut taxes and increase spending. If Japan's deficit looks set to increase, the Japanese government bond (JGB) market could experience volatility. That volatility could spill over into bond and stock markets globally thereafter. In June, both the Bank of Japan (BOJ) and Ministry of Finance (MOF) took steps to ease liquidity pressure in longer-term JGB maturities. Any threat to financial stability may cause the BOJ to slow the pace of balance sheet reduction again and the MOF shift even more issuance to shorter duration bonds. Additionally, the BOJ and MOF may be able to calm markets by talking about future actions they could take without needing to take decisive action.

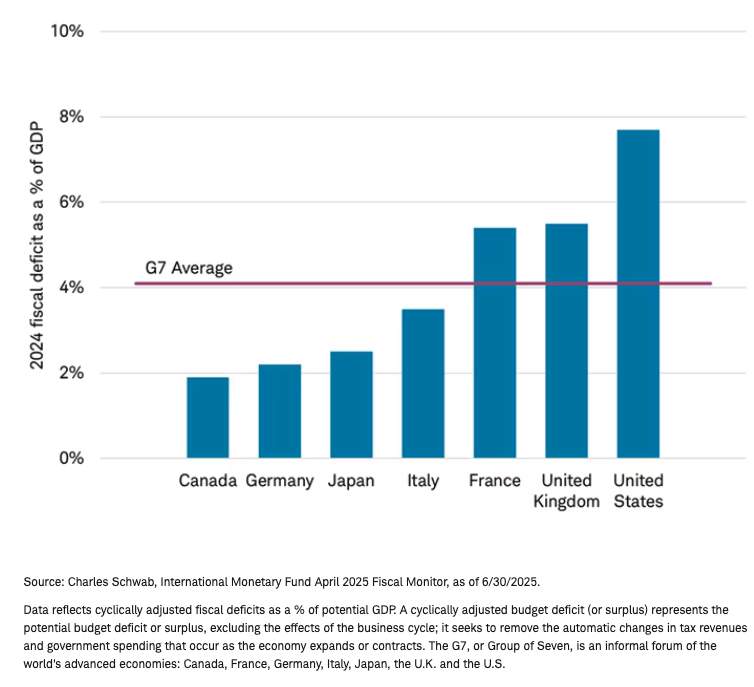

In Europe, fixing deficits is also causing friction. In the U.K., government bond yields spiked higher in early July due to questions about adherence to fiscal rules designed to keep deficits in check that arose after the government backtracked on some unpopular spending cuts; tax increases are possible in the autumn. Disagreements over actions needed to meet European Union (EU) rules that require reducing the French deficit from 5.8% in 2024 to 3% by 2029 have resulted in the eighth no-confidence vote for Prime Minister Francois Bayrou, setting up a budget fight and potential new elections in the fall. Deficit troubles in some European countries may hinder their ability to meet the increased NATO defense spending target of 5% of gross domestic product (GDP) by 2032.

Larger-than-average deficits are not uncommon

One country that may have an easier time is Germany. Germany's fiscal discipline over the years has resulted in a debt-to-GDP of just 64% in 2024, according to the International Monetary Fund—roughly half that of the U.S. Changes in U.S. policies toward NATO prompted Germany to pass defense and infrastructure spending bills this spring that translate to 1 trillion euros of spending over the next decade, so Germany's fiscal deficit is expected to increase. The issuance of more German government bonds to boost economic growth could attract new investors and increase demand for the euro. Although spending may not be linear, increased defense spending could be a durable, secular trend. European countries may prioritize European defense companies. So far this year, the MSCI EMU Aerospace and Defense Index in USD is up 68% through July 10, while the S&P Aerospace and Defense Select Industry Index has returned 27%.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, political instability, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Currency trading is speculative, volatile and not suitable for all investors.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Investment and Insurance Products Are: Not FDIC Insured • Not Insured by Any Federal Government Agency • Not a Deposit or Other Obligation of, or Guaranteed by, the Bank or any of its Affiliates • Subject to Investment Risks, Including Possible Loss of Principal Amount Invested

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co. Inc. (Member SIPC), and its affiliates offer investment services and products. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products.

This site is designed for U.S. residents. Non-U.S. residents are subject to country-specific restrictions. Learn more about our services for non-U.S. residents, Charles Schwab Hong Kong clients, Charles Schwab U.K. clients.

© 2025 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. Unauthorized access is prohibited. Usage will be monitored.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All