Trump’s Trade Deal with China Is a Tailwind for Global Shipping

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsPresident Donald Trump’s announcement on Wednesday of a new trade agreement with China is the kind of headline that gives markets a sense of relief. As I overheard this week at Wealth Management’s EDGE conference, which I attended in Boca Raton, Florida, we may have dodged a recession.

Beyond that, I think Trump’s announcement provides investors with a fresh incentive to turn their attention to global trade, particularly the shipping industry.

According to the president’s statement on Truth Social, the deal is “done,” pending final approval from both him and President Xi Jinping. The terms include a commitment from China to supply rare earth metals, while the U.S. maintains significantly higher tariffs on Chinese imports—reportedly 55% compared to China’s 10%.

I think most people would agree that, after months of tariff turmoil, this is a constructive step toward stability and, indeed, fairness. For shipping, that matters more than you might think.

Shipping Activity Rebounds as Tariff Pause Boosts Imports

As everyone recalls, the White House imposed an eye-popping 145% tariff on Chinese imports in April, sending shockwaves through global supply chains and capital markets. Retailers hit the brakes. Orders were delayed or canceled, and ocean freight volumes plunged.

But just a few weeks later, the administration announced a 90-day pause and slashed tariffs to 30%. “Reciprocal” tariffs with other trading partners were also temporarily frozen.

During that window, we’ve seen a surge of renewed shipping activity.

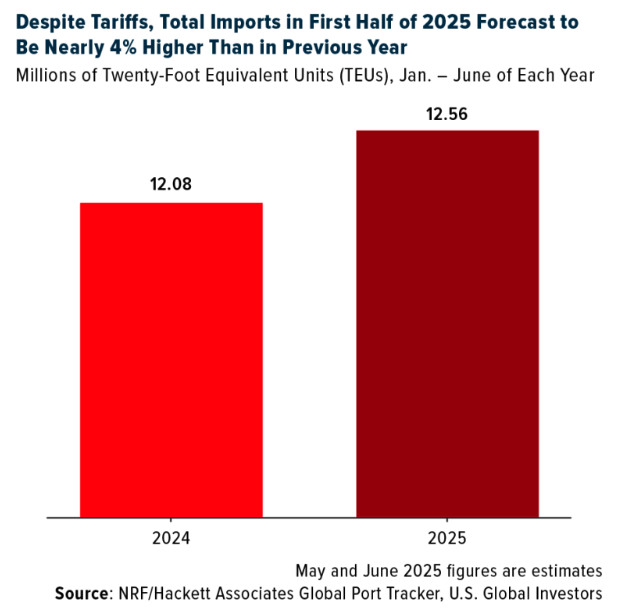

The National Retail Federation (NRF) reported this week that container imports at U.S. ports are now expected to climb 3.7% year-over-year for the first half of 2025. That’s better than forecasts before the pause. Shipping volume from China jumped 9% in the first week of June alone, according to Goldman Sachs data.

Rates Are Up

The container shipping industry has always been cyclical and sensitive to geopolitical events. This year has been no exception. After bottoming in 2023, rates have rebounded sharply, driven not only by tariff uncertainty but also by persistent global disruptions, such as the Red Sea crisis.

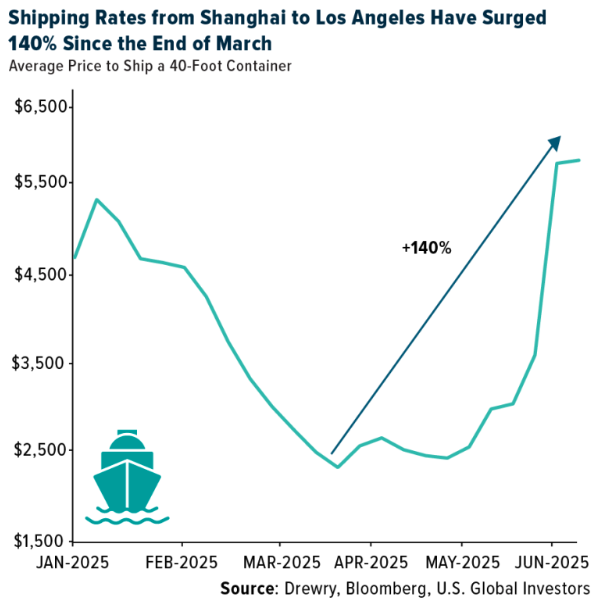

Drewry’s World Container Index showed a 70% spike in just four weeks, with freight costs from Shanghai to Los Angeles up nearly 140% since the end of March. That said, prices remain well below the COVID-era highs, when rates surpassed $10,000 per 40-foot container.

For context, today’s rates are closer to $5,800—a historically elevated level, but not unsustainable. Importers are moving fast to restock while the policy window is open. That activity is supporting not only shipping volumes but also company earnings.

More Shipping Companies Joining the $10 Billion+ Market Cap Club

In the first quarter of 2025, the global container shipping industry posted nearly $10 billion in profit. That’s a drop from the $15.6 billion earned in Q4 of last year, but it’s also 83% higher than the same period in 2024.

The market has taken notice. As of this month, I count nine publicly traded container carriers with a $10 billion market cap or higher. That includes names like Maersk and Hapag-Lloyd, as well as fast-growing Asian players like Wan Hai Lines. These firms now rival or exceed well-known, investable U.S. airline stocks in valuation.

This tells me that institutional investors see the potential in global shipping.

Granted, it’s not all smooth sailing. A recent survey by Freightos of more than 100 small-to-midsize importers paints a picture of anxiety beneath the surface. Even with the pause in place, 80% of respondents said they’re as or more worried than they were in April. Nearly half gave the situation a “perfect 10” on the disruption scale. Full disclosure, this survey was taken before the U.S.-China trade deal was announced.

Reshoring—or the practice of shifting production back to the U.S.—remains a possibility for companies that have moved overseas, but only 6% of companies have done so, according to Freightos.

World Bank Backs Trump’s Push for Fairer Global Trade Practices

You may have seen headlines this week that the World Bank revised its global growth forecast downward to 2.3% for 2025, marking the slowest non-recessionary year since 2008. Trade frictions, including those stemming from tariff uncertainty, are among the top culprits.

But there’s more to the story. The same World Bank report echoed Trump’s longstanding complaint that the U.S. faces unfairly high trade barriers abroad. The Washington, D.C.-based organization calls for a broad reduction in global tariffs, suggesting growing recognition of the problem and, perhaps, momentum for reform.

If that happens, and the world moves toward more equitable trade terms, shipping could be a key beneficiary. More open markets mean more trade, and more trade means more cargo.

Shipping companies are coming off a strong earnings season. Rates are elevated but not extreme. Inventories are being replenished. And long-term, the world will still need ships to move the goods that power our economies.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.32%. The S&P 500 Stock Index fell 0.39%, while the Nasdaq Composite fell 0.63%. The Russell 2000 small capitalization index lost 1.49% this week.

- The Hang Seng Composite gained 0.89% this week; while Taiwan was up 1.90% and the KOSPI rose 1.36%.

- The 10-year Treasury bond yield fell 10 basis points to 4.40%.

Airlines and Shipping

Strengths

- The best performing airline stock for the week was Embraer, up 3.8%. According to UBS, parked GTF aircraft remain near a plateau, at 775 aircraft at the end of May, up a touch from 756 at the end of April.

- Air freighters’ outbound flights have largely recovered to the level before May 2 when the 30% tariff rate on Chinese de minimis went effective, reports Goldman, from a trough of 20% decline during the first week of May.

- Qantas has closed Jetstar Asia. The airline is expected to post an A$35 million underlying EBIT loss in FY25e prior to closure decision. The closure cost is estimated to be A$175 million with one-third in FY25e and two-thirds across FY26e, taken outside of underlying earnings. The pre-tax cash impact will be $160 million, largely incurred in FY26, according to Goldman.

Weaknesses

- The worst performing airline stock for the week was Frontier, down 14.5%. TSA throughput through June 8 was down 4.2% year-over-year on a trailing seven-day basis versus down 1.7% in the prior week. Off-peak (Tuesday, Wednesday, Saturday) continued to be significantly weaker than peak travel, with off-peak down 7.3% and peak down 2.2%, according to Bank of America.

- Stifel reports that air capacity is still elevated—mostly due to lower freighter demand from de minimis rule changes. Pricing is likely to stay weak.

- According to Statistics Canada, the number of Canadians flying back from the U.S. was down 24% year-over-year in May compared to a 20% year-over-year decrease in April. Meanwhile, return trips from overseas countries increased 10% year-over-year.

Opportunities

- A320 & A350 backlogs are almost sold out through 2029, reports Bank of America, and these orders will add backlog visibility well beyond 2030. Airbus & Boeing book to bill ratios in 2024 are 1.15x and 1.63x respectively.

- New ship orders have reached levels not seen since 2008, up 31% year-over-year in FY3/25 with now a four-year backlog. Some 65% of bulkers are still over 15 years in service, the usual replacement age, according to CLSA.

- Over the past 10 years, the airplane manufacturers have outperformed entering the airshow, while suppliers have outperformed exiting the event, explains RBC. The airframe OEMs have outperformed the market by 140 basis points (bps) for the week leading up to the airshow. During the airshow, the commercial OE industry has historically outperformed the market by an average of 150 bps.

Threats

- Confidence in the 2025-2026 outlook at Airbus has deteriorated. For example, suppliers now see the A320neo as the most at-risk program, and their view of production rates exiting 2025 has declined from 60 per month in RBC’s 2H24 survey, to now just under 55 per month. Similarly, suppliers have lowered their outlook for the A350.

- Spot rates on transpacific (TP) routes have been hiking aggressively in the past few weeks, resulting from a short-term mismatch in supply and demand. However, given the surging rates, operators have high incentives to add capacity to U.S. West routes, reports Morgan Stanley.

- According to Flight Master, China’s domestic flight seat capacity increased 3% year-over-year, faster than 2% the prior week. However, domestic passenger volume growth decelerated to 4% from 5% year-over-year. Domestic airfare decline widened to -4% from -2% year-over-year in week 22.

Luxury Goods and International Markets

Strengths

- L’Oréal Groupe announced this week the acquisition of a majority stake in Medik8, a British skincare brand. The company’s founder will remain on the board and management team to ensure continuity. The acquisition aligns with L’Oréal’s strategy to strengthen its luxe portfolio by adding a premium, science-backed skincare brand with strong growth potential.

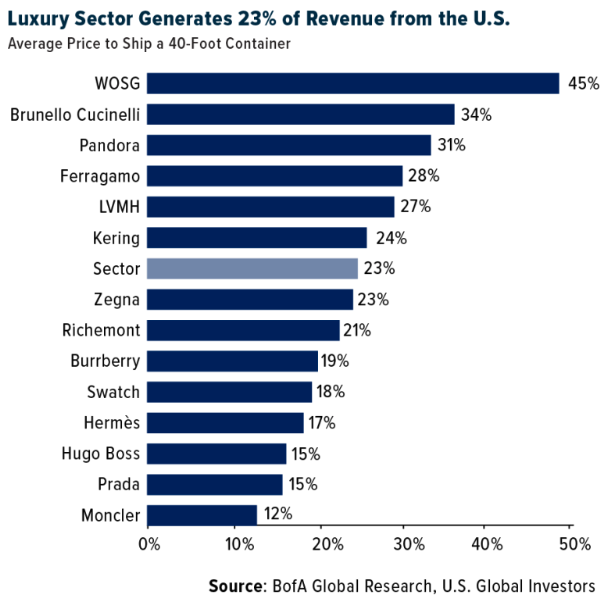

- According to the last Bank of America luxury report, luxury companies generate 23% of their revenue from the U.S., one of the leading luxury markets worldwide. Brunello Cicinelli and Pandora are luxury companies with the most exposure to the U.S., with 34% and 31% exposure, respectively, compared with Prada with 15% exposure.

- Ananti, a South Korean company that operates leisure clubs, was the top performer in the S&P Global Luxury sector, gaining 35.72% over the past five days. The stock price rose 14% this week, higher than any close since April 2022, and it was the best performer among its peers.

Weaknesses

- According to Business Insider, in response to U.S. trade tariffs, major brands like Victoria’s Secret are cutting promotions and gifts to offset a projected $50 million hit to operating income. This is just one example of how these policies directly impact consumers and slow sales.

- China’s deepening deflation and economic slowdown are weakening demand for luxury goods, especially among middle-class shoppers who favor steep discounts or second-hand items. Brands like Coach have slashed prices by up to 90% to sustain sales, harming brand value and pricing power. This highlights the sector’s vulnerability to economic pressures, raising concerns about inventory, margins, and exclusivity.

- Cettire, a retail apparel company from Australia, was the worst-performing stock in the S&P Global Luxury Index, falling 40%. The company issued its second profit downgrade in less than two months, affecting its share price.

Opportunities

- L’Oreal announced a collaboration with Nvidia to use next-gen AI for transforming beauty experiences, including 3D product rendering and generative AI content creation, aiming to enhance personalized marketing and digital shopping, reports Bloomberg.

- Moncler’s spending share rose from 3% to 7.46% in May month-over-month. As a leading Italian luxury brand, this shows that despite global economic uncertainty, customers continue to spend on luxury as an experience, not just a product.

- Prada, Alfa Romeo, and the Luna Rossa Prada Pirelli sailing team announced a high-profile partnership to launch limited-edition Quadrifoglio models in 2026, inspired by racing yacht aerodynamics and materials.

Threats

- Wells Fargo maintains an underweight rating on Tesla with a $120 price target, citing a weak Q2 outlook as May deliveries dropped 23% year-over-year. Key markets—North America, Europe, and China—face double-digit declines, with France, Portugal, and Sweden down 50%, per Investing.com.

- A 2024 PYMNTS report finds 79% of Gen Z and millennials seek financial advice on social media like TikTok, where influencers promote luxury handbags, especially Hermès Birkins, as alternative investments. This hype-driven trend risks inflating short-term demand and attracting inexperienced buyers, potentially harming the sector if returns don’t meet expectations.

- Asian luxury markets, especially China, Japan, and Southeast Asia, show a shift toward quality, craftsmanship, and timeless designs over logos, says Vogue Business. With China’s consumer confidence dipping and emerging markets uncertain, buyers favor local, authentic brands, challenging Western luxury houses to justify premiums through real value.

Energy and Natural Resources

Strengths

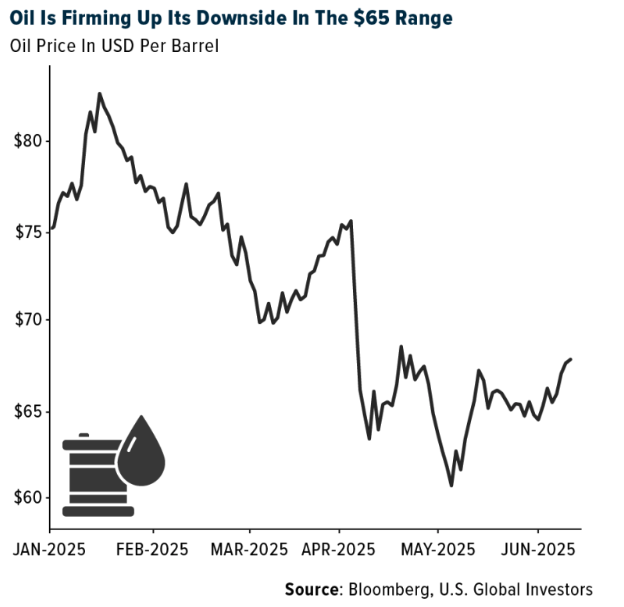

- The best-performing commodity for the week was crude oil, rising 13.25%. Oil prices spiked as much as 14% after Israel launched airstrikes on Iran, triggering fears of a broader conflict in the Middle East and potential disruptions to global oil flows through the critical Strait of Hormuz. While the sharp move reflects rising geopolitical risk, the market is not yet fully pricing in worst-case disruptions to Iranian oil infrastructure or exports.

- Oil was also buoyed by renewed U.S.-China trade talks, which offered the potential for reduced global tensions. Brent crude traded above $66 per barrel after gaining 4% last week. Negotiators from the U.S. and China were set to meet in London, raising hopes that the world’s two largest economies could make progress on disputes that have rattled markets this year, according to Bloomberg.

- The U.S. Energy Information Administration (EIA) has forecast a decline in domestic crude production in 2026—the first drop since 2021. This may come as a surprise to policymakers seeking to boost U.S. energy output. However, domestic producers appear to favor constrained production to minimize downward pressure on prices, especially amid an anticipated hike in OPEC+ output. Political instability remains the wildcard for oil prices, though.

Weaknesses

- The worst-performing commodity for the week was natural gas, dropping 4.84%. European natural gas prices are under pressure due to weak global demand and a surge in LNG imports, allowing traders to accelerate storage injections, now over 51% full. Meanwhile, China cut natural gas imports by 11% year-over-year in May, as record domestic output and increased reliance on clean energy reduced demand for thermal fuels.

- Iron ore prices fell as data from China pointed to persistent deflationary pressures in Asia’s largest economy. Additionally, year-to-date imports of the commodity lagged last year’s pace, according to Bloomberg.

- While the OPEC+ alliance is increasing oil production quotas to restart idled capacity, that shift has yet to result in significant gains in actual output, according to Morgan Stanley. “Despite the approximately 1 million-barrel-per-day increase in production quotas between March and June, an actual rise in production is hard to detect,” analysts, including Martijn Rats, noted.

Opportunities

- According to Morgan Stanley, May steel license data suggests imports will rise 14% month-over-month but fall 17% year-over-year. Import spreads and lead times both narrowed as spot hot-rolled coal (HRC) prices fell to $840/ton throughout May. At the end of the month, President Trump doubled steel tariffs to 50%, lending support to domestic prices.

- RBC maintains a positive long-term outlook on uranium and nuclear energy fundamentals, citing strong, steady demand and increasing supply risks—especially into the 2030s. Long-term energy demand growth from AI and data centers is a key factor driving nuclear demand, as underscored by the White House’s nuclear-related executive orders announced prior to the World Nuclear Fuel Market (WNFM) conference and the Meta/Constellation 20-year nuclear power purchase agreement announced during the mid-conference.

- Some refiners process a petroleum product called ethane, a gas that is inexpensive and easily converted into chemical building blocks used in products such as packaging and solvents. Thanks to the shale gas boom, the U.S. is the world’s largest ethane producer. China is its top customer, importing nearly half of total U.S. output, according to Bloomberg.

Threats

- The U.S. clean energy sector is struggling under the strain of persistently high borrowing costs, President Trump’s anti-renewables policies and elevated tariffs. The latest casualty is residential solar company Sunnova Energy International Inc., which filed for bankruptcy early Monday.

- China is reducing imports of coal and natural gas as domestic output hits record highs and a surge in clean energy reduces the need for thermal generation. Coal imports in May fell 18% from the same month last year, while natural gas shipments dropped 11%, according to customs data published on Monday.

- Even as trade tensions cloud demand expectations, refined copper production continues to rise in China. The resulting competition has shifted bargaining power to some of the world’s largest miners. Copper treatment charges—a key revenue stream for processors—have plunged well below zero in the spot market. The situation is drawing attention to the surprising resilience of China’s output and raising questions about how long it can be sustained, according to Bloomberg.

Bitcoin and Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Kaia, rising 47.86%.

- Kathleen Wrynn, formerly of JPMorgan Chase, is joining Invesco as global head of digital assets. Wrynn, who spent about three years at JPMorgan as an executive director, will be overseeing Invesco’s digital-asset portfolio which includes tokenized assets and cryptocurrencies, writes Bloomberg.

- Crypto ETFs have shown exceptional growth, with total assets under management rising approximately 97% year-over-year to $120 billion, according to new research by JPMorgan. This surge has been driven largely by the successful launch of spot Bitcoin ETFs in January 2024, which sparked sustained investor interest. In addition to strong inflows, the market has seen the debut of 37 new crypto funds, signaling robust product expansion.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Sonic, down 14.48%.

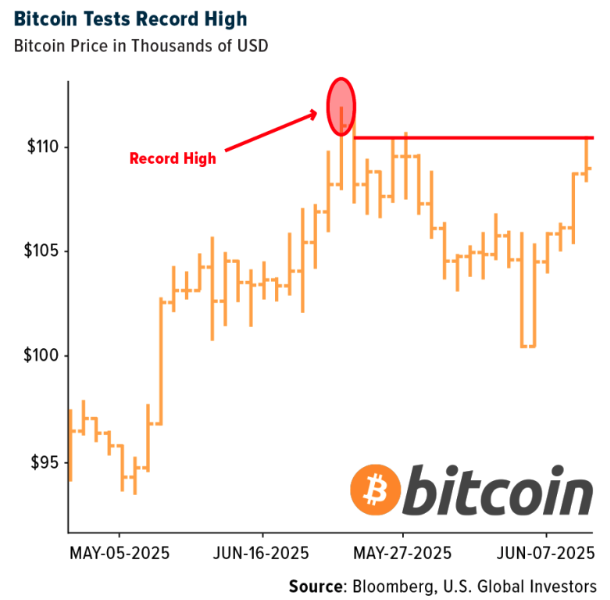

- Bitcoin retreated from its daily high after failing to reach its record price set two weeks ago, despite jumping 16% this year due to increased demand from institutional buyers, according to Bloomberg.

- Defiance has withdrawn a regulatory filing for the Defiance MSTR Double Short Hedged ETF, which would have taken short positions on two other ETFs tracking Michael Saylor’s Strategy, explains Bloomberg. The withdrawn application doesn’t necessarily mean the product is dead, as some asset managers have pulled back and refiled plans for similar products in the past.

Opportunities

- Webull has expanded its retail trading platform to allow customers to bet on the future price of Bitcoin and Ethereum through a partnership with Kalshi. The new product will give traders the opportunity to bet on specific financial events, says Bloomberg, such as whether the price of Bitcoin will land above or below a certain price at a given hour.

- Stripe has agreed to acquire Privy, a crypto wallet provider that helps companies build crypto wallets into their user experiences. Privy’s technology allows for seamless crypto transactions, eliminating the need for users to create external wallets and link them to their accounts, writes Bloomberg.

- South Korea’s new President Lee Jae-myung is moving to allow local companies to issue stablecoins, explains Bloomberg, building on his campaign pledge. The proposed Digital Asset Basic act would enable companies with at least 500 million won in equity capital to issue stablecoins, with refunds guaranteed through reserves.

Threats

- Two men, John Woeltz and William Duplessie, pleaded not guilty to an indictment charging them with first-degree kidnapping in connection with the alleged kidnapping and torture of an Italian tourist to gain access to his cryptocurrency accounts, writes Bloomberg.

- Jim Chanos criticized Michael Saylor’s valuation model for his crypto-treasury firm, calling it “financial gibberish” and recommending that investors short the company shares and buy Bitcoin instead. Chanos argued that Saylor’s firm’s market value should be based on its Bitcoin holdings, according to Bloomberg.

- Paraguayan President Santiago Pena deleted a post in his X account after a likely hack by crypto scammers who claimed the South American nation had approved Bitcoin as legal tender, Bloomberg reports. The president said on X that his account saw “irregular” activity, indicating “a possible unauthorized access.”

Defense and Cybersecurity

Strengths

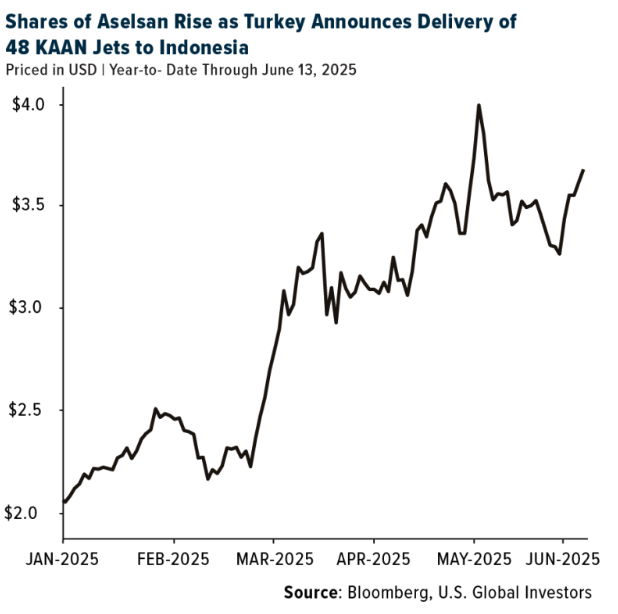

- President Erdoğan announced that Turkey will export 48 domestically produced KAAN fighter jets to Indonesia under a new bilateral agreement—an important deal that also benefits defense contractor Aselsan, which supplies key avionics and electronic warfare systems for the aircraft.

- NVIDIA’s plan to build Germany’s largest AI factory, powered by 100,000 high-performance chips; Qualcomm’s new R&D center in Vietnam; and AMD’s rollout of next-gen AI datacenter systems illustrate the aggressive global expansion of AI capabilities across geographies and firms.

- The best-performing stock this week was National Presto Industries, rising 8.31% after a surge in institutional buying and renewed investor interest driven by strength in its defense segment and improving technical indicators.

Weaknesses

- Canada’s F-35 acquisition costs ballooned by nearly 50%, and the Pentagon halved its F-35 order for the U.S. Air Force. These signals raise concerns over affordability, readiness and possible delays in core defense programs.

- Recent Pentagon reports highlight how inflation and supplier bottlenecks are causing delays and cost overruns in multiple weapon system contracts, including munitions and radar upgrades. Budget forecasts may need revisions, weakening program execution in FY2026.

- The worst-performing stock this week was Rocket Lab, which declined by 12.14% after issuing Q2 revenue guidance below expectations and warning of continued losses due to rising R&D and infrastructure costs related to its Neutron rocket program.

Opportunities

- Palantir’s AI-driven transformation of manufacturing workflows and Cisco’s new AI-optimized network and firewall systems demonstrate the expanding role of artificial intelligence in enhancing critical infrastructure and enterprise resilience.

- A partnership between ANSYS and Turbotech on the development of the world’s first hydrogen-fueled turboprop engine for aviation could open new opportunities in sustainable defense and civilian aerospace propulsion systems.

- NATO’s Exercise Med Strike and Formidable Shield 25 delivered advanced multinational training in counter-drone tactics, missile defense and carrier operations, further deepening tactical integration between U.S. and European allied forces.

Threats

- Israel’s Operation Rising Lion—a large-scale air offensive targeting Iran’s nuclear and military infrastructure—risks escalating into a prolonged regional war. The conflict could disrupt global oil markets and provoke widespread retaliatory attacks across the Gulf region.

- President Vladimir Putin has called for the urgent mobilization of Russia’s economy toward a wartime footing, including expanding ground forces and constructing new military bases. This signals a long-term strategic escalation beyond the immediate Ukraine conflict.

- Iran has launched a large-scale retaliatory strike on Israel following Operation Rising Lion, deploying ballistic missiles and drone swarms targeting military installations and urban centers. While Israeli defense systems intercepted most projectiles, several impacts were reported, escalating tensions and raising fears of broader regional destabilization.

Gold Market

This week gold futures closed at $3452.20, up $105.60 per ounce, or 3.16%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.10%. The S&P/TSX Venture Index came in off 0.06%. The U.S. Trade-Weighted Dollar fell 1.07%.

Strengths

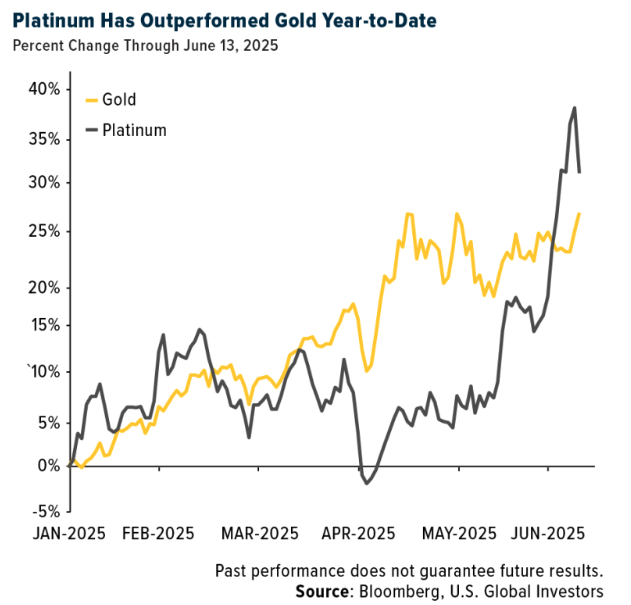

- The best performing precious metal for the week was platinum, up 3.62%. Prices of platinum, a precious white metal, have recently jumped, gaining over 35% year-to-date, with spot prices currently about $1,226 per ounce, but surged to nearly $1,300 on Thursday. Spot gold prices are around 30% higher over the same period. Platinum’s dizzying rally does not just echo the stunning rise of gold prices. It also reflects a more fundamental issue of supply deficit, Bank of America analysts wrote in a note last Friday. Solid fundamentals support platinum prices, wrote the BofA analysts, highlighting demand for the white metal in the jewelry industry.

- With central bank gold purchases over the last several years, gold bullion has now surpassed the euro, making it the second-largest reserve asset at 20% of total holdings. Interestingly, central bank holdings still stand at about 35,000 tons, the same levels last seen in the Bretton Woods era. It sounds like they need to buy more to catch up with the times, as they now own a much smaller percentage of global stocks. In addition, good news out of China with Chow Tai Fook Jewellery Group reporting better-than-expected net income for the fiscal year ended March, with improved margins. This suggests that rise in gold prices has not crimped demand for gold. In fact, some retail buyers report that the price increase is the reason they are buying gold.

- The start of a gold-futures contract in Singapore has put the spotlight on a flurry of moves in Asian financial hubs to capitalize on rising interest in the commodity as demand increases. The BlackRock-backed Abaxx Exchange began offering a U.S. dollar-denominated contract, sized at 1 kilogram (32.15 troy ounces) and locally deliverable, on Thursday. The move will be among developments highlighted at an industry conference organized by the Singapore Bullion Market Association to be held in the city-state over three days from Sunday

Weaknesses

- The worst performing precious metal for the week was palladium, down 2.44%. ETFs sold 601 ounces of palladium as of Wednesday this week, purchasing back 1,914 as of Thursday. Palladium has been the strongest net buying activity for precious metals from ETFs this year, up 7.5%, compared to 6.8% for gold, 5.7% for silver, and platinum, with a 5.6% change in buys over sells. This net buying effect, combined with being down for the week, signals that larger players may be taking a bit more speculative position on the short side of palladium, which also faces threats from decarbonization efforts.

- Petra Diamonds announced the results of the combined Tender 5 & 6 sales, which were lower than BMO’s estimates on volume sold, product mix and pricing. The continuing challenges in the diamond market and the weaker sales do not bode well given the ongoing negotiations to refinance Petra’s debt obligations, in their view.

- Hochschild Mining provided an update on production at its Mara Rosa mine in Brazil. Heavy rains and contractor issues have resulted in the mine producing only 25,000 ounces of gold year-to-date. Guidance will be revised down in due course, according to Bank of America.

Opportunities

- Gold stays in a consolidation phase, with focus shifting to U.S. economic data for cues about the dollar’s direction and the Federal Reserve’s next policy moves, according to Kotak Securities. Bullion may reach $4,000 an ounce early next year due to central bank buying and geopolitical risks, it said.

- Gold, as well as some non-U.S. equities, may offer protection for portfolios amid concern about U.S. assets, including potential fallout from tax changes being considered, according to Citigroup. “We recently added to gold along with European and Chinese equities to diversify portfolios against a potential reduction in appetite for U.S. assets,” Kate Moore, chief investment officer at Citi Wealth, said in a note.

- Paul Tudor Jones predicted this week that he expects to see the dollar drop by 10% over the next year as short-term interest rates fall. This would be extremely bullish for the price of gold, as the dollar has already declined nearly 8% in 2025 amid the tariff chaos and the dramatic shift in diplomatic relationships. Jeffrey Gundlach sees the yield curve threat coming from the long end of the yield curve rising due to demand for compensation for taking on the risks of America’s debt burden and an interest expense that has become “untenable.”

Threats

- According to Canaccord, Equinox pro forma 2025 guidance is 11% lower than previously issued guidance on a consolidated basis, while all-in sustaining costs (AISC) have increased 23%. The decline in production was largely attributable to a slower ramp-up at Greenstone, while the cost increase is also attributed to Greenstone, as well as the Brazilian mines.

- Tanzania plans to make it compulsory for large-scale miners to refine and trade at least 20% of their gold output domestically as the East African nation seeks to benefit from a rally in the bullion price and control a larger share of its resources, according to Bloomberg.

- On Friday, Mali’s government noted that it will establish a state-controlled gold refinery in partnership with Russia’s Yadran to boost bullion revenue. Specifications require the refiner to have a capacity of 200 metric tons. It is not known yet if the refinery will require artisanal miners and or international miners to refine their gold within Mali.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2025):

L’Oreal SA

Pandora

Prada

Moncler

NVIDIA

Brunello Cucinelli

Tesla

LVMH

Cie Financiere Richemont

Kering

Hermes International

Hugo Boss

Moncler

Air Canada

Allegiant Travel

Qantas

Boeing

Embraer

Frontier Group

Airbus

COSCO SHIPPING Holdings Co. Ltd.

AP Moller – Maersk A/S

Evergreen Marine Corp.

HMM Co. Ltd.

Nippon Yusen KK

Wan Hai Lines Ltd.

Delta Air Lines Inc.

United Airlines Holdings Inc.

Southwest Airlines Co.

American Airlines Group Inc.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The Drewry World Container Index (WCI) is a composite index that tracks the average cost of shipping a 40-foot container (FEU) on eight major international trade routes.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All