AI: The Challenges for Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn part one of our new series, AI Alpha, we explored the sweeping potential of artificial intelligence (AI) as a transformative force. But alongside that opportunity lies a more complicated reality. In part two, we examine the structural challenges, strategic trade-offs, and competitive pressures that we believe will shape how AI ultimately delivers economic payoff. Understanding AI as a general-purpose technology helps clarify both its disruptive power and the obstacles that may delay or dilute returns.

General-Purpose Technologies: Unseen Engines, Uncertain Returns

AI stands as the latest chapter in the storied history of general-purpose technologies, each breakthrough having laid the foundation for a transformative techno-economic revolution.

For example, the printing press revolutionized the mass production of texts, profoundly influencing education, religion, science, and politics; the steam engine powered factories, trains, and mining operations, enabling mass production and transforming transportation; electricity powered industrial machinery, household appliances, and modern communications, reshaping production, consumption, and interaction; and computers and the internet transformed commerce, communication, and innovation by processing and transmitting information. Each of these technologies redefined society by providing versatile platforms for mass production, dissemination, and connectivity.

Today, AI’s general-purpose capability stems from its ability to translate various types of data into numerical representations and compute similarities between them, thereby enabling its application in a wide array of settings. By leveraging vast datasets and sophisticated algorithms to extract hidden patterns and drive decision-making—is emerging as a general-purpose technology poised to redefine economic structures, spur innovation across sectors, and reshape societal functions.

Zero ROI

Left to themselves, general-purpose technologies command no tangible return on investment. As Paul David1 elucidates in his analysis of technological transformations, two principles are paramount. First, the evolution of techno-economic regimes built around these technologies often spans decades—returns eventually emerge, though after a long gestation period. Second, general-purpose technologies require a suite of complementary products, infrastructure, training, and organizational changes to realize their full economic value.

This second point underscores the inherent complexity of broad technology adoption. Providers of the technology therefore invest in nurturing complementary innovations, sometimes developing them in-house. Early electric utility companies, such as Edison Electric Company (General Electric’s precursor) and Westinghouse Electric recognized that raw electricity was of little use until harnessed by consumer products that, in turn, drove demand. Today, Nvidia CEO Jensen Huang follows this time-tested playbook, understanding that graphics processing units (GPUs) have limited value without complementary software. In AI’s layered ecosystem, GPUs train AI models that must be integrated into further complementary applications.

AI, in itself, offers no immediate return; it is only through the creation of complementary products—be they digital applications, autonomous vehicles, or humanoid robots—that its full potential can be realized. ChatGPT may have served as AI’s light bulb, but as we progress into our Information Age, inventors are still racing to create the toasters, washing machines, and refrigerators of the AI era.

A self-reinforcing flywheel is at work here: each leap in AI spurs inventive responses that, in turn, accelerate further technological advances. I believe the promise of AI will unfold gradually, contingent on the maturation of complementary products and broader societal shifts, including labor reorganization and even political recalibrations in response to changing employment landscapes.

Investors must recognize that the journey toward AI’s trillions of dollars in impact is both intricate and protracted—a transformation unfolding as gradually as the evolution from a solitary light to a fully furnished home complete with all its essential appliances. Yet this steady progression often clashes with a market that rapidly reprices assets based on shifting narratives, a dynamic tension that poses constant challenges.

Darwin, Fermat, and Pascal: Why AI May Not Lead to Profitability

In 1859, Charles Darwin observed, “It is not the strongest of the species that survives, nor the most intelligent, but the one most responsive to change.”2

And in 1994, another Charles, Mr. Munger, echoed that spirit of navigating complexity with a different lens; he noted:

“The Fermat/Pascal system is dramatically consonant with the way that the world works. And it’s a fundamental truth. So you simply have to have the technique … One of the advantages of a fellow like Buffett, whom I’ve worked with all these years, is that he automatically thinks in terms of decision trees and the elementary math of permutations and combinations.”3

Both point to the same reality: survival and success depend on the ability to assess risk, adapt, and act. And I believe AI’s potential impact must be viewed through that lens.

AI’s potential impact is vast. We are in the Information Age that has been evolving for more than 50 years. The true effect of AI will depend on the businesses that integrate it, the innovators who build its return on investment (ROI) within digital ecosystems, and the managers navigating complex strategic choices with outcomes that may ultimately lie beyond their control.

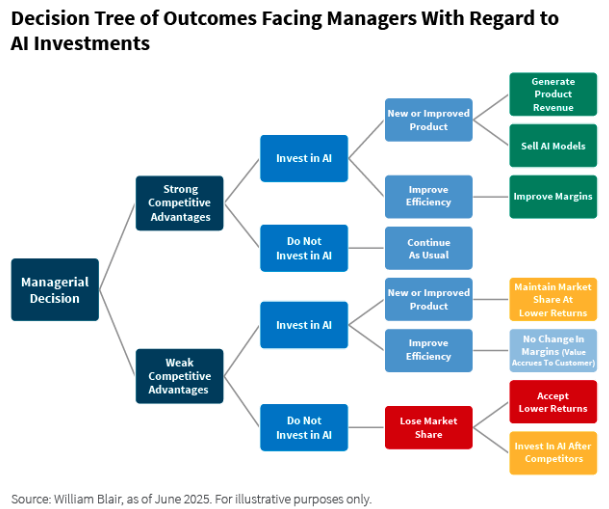

If a business saves or generates an extra $1 million through AI, the question remains: does that benefit translate directly to its bottom line, or is it passed on to consumers through competitive pressures? Investors who assume every dollar will boost profitability may be disappointed if market dynamics force these gains to accrue elsewhere. AI will likely be a strategic investment rather than an economic investment for many businesses as they invest in AI not for immediate revenue or cost savings but simply to remain competitive. The decision tree below reflects some of the decision paths facing businesses.

As the chart above illustrates, managers face a branching decision tree when considering AI investments. Where a company has a strong competitive advantage, the arithmetic is straightforward—AI can drive additional revenue and/or improved margins, potentially reinforcing existing advantages and delivering what shareholders anticipate. In these scenarios, firms may benefit from enhanced products and lower costs, allowing them to capture a greater share of value.

In contrast, in more fiercely contested markets, companies with weak competitive advantages lack the luxury of dominance. Here, competitors rapidly anticipate and match improvements, forcing managers to invest in AI merely to stay in the game—even if such investments do not translate directly into increased revenue or profitability. Although AI may reduce total expenses when its cost savings exceed the investment, whether this translates into higher margins depends on the elasticity of demand and the relentless force of competitive pressures. Like rising blinds in poker, every player must commit more resources just to remain competitive, often passing the benefits onto customers rather than the bottom line. I believe most businesses will find themselves trapped in this competitive arena, where substantial AI expenditures, despite their promise, ultimately vanish from the financial statements, a stark reminder that in many competitive environments, survival demands economic sacrifices at the altar of innovation.

These competitive market dynamics reflect the broad magic of capitalism at work—where better products emerge at lower prices and the relentless force of competition curtails profit margins beyond any simple ROI calculus. Just as peacocks incur costs for their elaborate displays or as Costco invests in wages and quality rather than skimming profit, businesses may adopt AI to signal strength, secure market position, or simply ensure survival—regardless of immediate returns.

A new general-purpose technology such as transformer-based AI reconfigures the digital ecosystem, echoing the upheavals Karl Marx highlighted in political and economic ecosystems triggered by inventions such as gunpowder or the printing press. Managers must weigh competition, customer power, and internal dynamics, all while accepting that shareholders might not be at the front of the queue for AI’s spoils.

Game theory problems, as illustrated by the decision-tree managers face—such as prisoner’s dilemma (without cooperation investment takes place out of self-interest), Pascal’s wager (uncertain downside makes investment the safer bet), or dollar auction (a zero-sum race forces escalating costs)—underscore the short-term rational yet sometimes long-term suboptimal paths companies may follow.

No single forecast or model can capture every nuance of these strategic choices, but prudent investors must build in a margin of safety and weigh broader strategic considerations when making their forecasts. Indeed, the landscape has shifted, and those who fail to adapt, whether business manager or investors, invite their own undoing.

Asymmetries for Public Investors: AI Winners and Losers

The history of investing in technological change reveals an intriguing asymmetry: it is often easier to pick the losers than the winners. As Alasdair Nairn’s Engines that Move the Markets illustrates, when railroads disrupted canals, it was easier to see that canal valuations would collapse than to pinpoint which railroad would ultimately prevail; similarly, the shift from horses to automobiles clearly signaled the obsolescence of equine transport, even if singling out Ford’s Model T as the definitive winner proved challenging. In the dot-com era, while it was difficult to predict Amazon’s rise, it was unmistakable that traditional brick-and-mortar retail would falter, and in the same vein, the transitions from video rental stores to Netflix and from traditional taxi services to Uber reveal that, though identifying the specific victor is challenging, an entire legacy industry could erode away.

This pattern arises because incumbents, built on outdated technological foundations, are not merely competing against a single firm but against a shifting technological frontier that continuously elevates the standard. AI is a general-purpose technology whose impact will ultimately depend on the complementary applications and products that evolve alongside it. Yet which specific company will prevail as the technology matures and new business models emerge remains a much greater unknown particularly in the digital realm, where the dynamism and complexity of business models is more pronounced than in the physical world.

Success ultimately depends on a multidimensional framework: product-market fit, competitive strength, and the ability to capture value rather than simply pass it to consumers. It is difficult to pinpoint the exact winners in every sector, yet in traditional areas—be it software, transportation, or online advertising—the competitive advantages of incumbent players must be reassessed. In such a competitive and evolving environment, investor success hinges not only on identifying the few winners but, more critically, on evading the far greater number of likely losers.

Today, another asymmetry confronts public-market investors with the rise of private capital. Unlike in the dot-com bubble—when companies predominantly raised funds through public markets, leading to volatile share prices—modern firms tend to remain private for longer, favoring venture capital and private equity. As a result, many AI-native companies, which are poised to drive the next technological paradigm, remain out of reach for public investors. While many AI-native startups remain out of reach, public investors who develop a nuanced understanding of how AI reshapes established businesses—by identifying which incumbents possess the culture, management, and competitive edge to potentially leverage these technologies—may still find rewarding opportunities.

Conclusion

Overall, AI’s evolution as a general-purpose technology confirms that true economic transformation unfolds only when innovative complementary products and societal shifts come into play—a process both gradual and inevitable. While the promise of trillions in value drives innovation, the journey is fraught with uncertainty, competitive pressures, and structural shifts that challenge conventional ROI measures; further complicating matters is the intangible nature of AI, which, unlike physical assets, forces investors to rely on faith as much as evidence. As the digital age inexorably marches forward, adaptation is necessary for survival.

If you’d like more information about how we’re thinking about AI in our portfolios, please reach out to our sales contacts.

Gurvir Grewal is a global research analyst on William Blair’s global equity team.

Want more insights on the economy and investment landscape? Subscribe to our blog.

1 Paul A. David (1990), The Dynamo and the Computer: An Historical Perspective on the Modern Productivity Paradox.

2 Charles Darwin (1859), On the Origin of Species.

3 Charles T. Munger (1994), “A Lesson on Elementary Worldly Wisdom As It Relates To Investment Management & Business” (talk delivered at USC Business School).

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

This content is for informational and educational purposes only and not intended as investment advice or a recommendation to buy or sell any security. Investment advice and recommendations can be provided only after careful consideration of an investor’s objectives, guidelines, and restrictions. Investing involves risks, including the possible loss of principal.

Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within William Blair Investment Management, LLC, or affiliates. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented. Past performance is not indicative of future returns.

For UK Investors: This material is distributed in the United Kingdom by William Blair International, Ltd., authorized and regulated by the Financial Conduct Authority (FCA), and is only directed at and is only made available to persons falling within articles 19, 38, 47, and 49 of the Financial Services and Markets Act of 2000 (Financial Promotion) Order 2005 (all such persons being referred to as "relevant persons").

For European Investors: This material is distributed in the European Economic Area (EEA) by William Blair B.V., authorized and supervised by the Dutch Authority for the Financial Markets (AFM) under license number 14006134 and also supervised by the Dutch Central Bank (DNB), registered at the Dutch Chamber of Commerce under number 82375682 and has its statutory seat in Amsterdam, the Netherlands. This material is only intended for eligible counterparties and professional clients.

For Swiss Investors: This material is distributed in Switzerland by William Blair Investment Services (Zurich) GmbH, Talstrasse 65, 8001 Zurich, Switzerland ("WBIS"). WBIS is engaged in the offering of collective investment schemes and renders further, non-regulated services in the financial sector. WBIS is affiliated with FINOS Finanzomubdsstelle Schweiz, a recognized ombudsman office where clients may initiate mediation proceedings pursuant to articles 74 et seq. of the Swiss Financial Services Act ("FinSA"). The client advisers of WBIS are registered with regservices.ch by BX Swiss AG, a client adviser registration body authorized by the Swiss Financial Market Supervisory Authority ("FINMA"). WBIS is not supervised by FINMA or any other supervisory authority or self-regulatory organization. This material is only intended for institutional and professional clients pursuant to article 4(3) to (5) FinSA.

For Australian Investors: This material is distributed in Australia by William Blair Investment Management, LLC (“William Blair”), which is exempt from the requirement to hold an Australian financial services license under Australia's Corporations Act 2001 (Cth). William Blair is registered as an investment advisor with the U.S. Securities and Exchange Commission (“SEC”) and regulated by the SEC under the U.S. Investment Advisers Act of 1940, which differs from Australian laws. This material is intended only for wholesale clients.

For Singaporean investors: This material is distributed in Singapore by William Blair International (Singapore) Pte. Ltd. (Registration Number 201943312R), which is regulated by the Monetary Authority of Singapore under a Capital Markets Services License to conduct fund management activities. This material is intended only for institutional investors and may not be distributed to retail investors.

For Canadian Investors: William Blair Investment Management, LLC relies on the international adviser exemption, pursuant to section 8.26 of National Instrument 31-103 in Canada.

This material is a marketing communication and is not intended for distribution, publication or use in any jurisdiction where such distribution or publication would be unlawful.

Copyright © 2025 William Blair. "William Blair" refers to William Blair Investment Management, LLC. William Blair is a registered trademark of William Blair & Company, L.L.C.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All