Fixed Income Outlook: A Not-so-Random Walk

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIt can be a challenge to identify the direction of asset prices when market moves are often predicated on the announcement of a single person. Wild market swings – once worthy of headlines – are at risk of becoming tedious. Aggressive price anchoring (start with a shockingly high tariff so that anything lower seems reasonable) by the White House means the world has had to adjust rapidly to a potentially new trade regime.

At the time of writing, only a handful of countries had reached a preliminary agreement with the US and legal opposition means some of the tariff increases might yet be revoked. The final tariffs could therefore be worse than expected, provoking recessionary fears and higher inflation, or more moderate, likely triggering a relief rally. Either way, outcomes among countries will differ. The US would be among the most impacted – its consumers will likely face higher prices and this may weigh on economic growth as households retrench and companies revisit investment plans. Ironically, Europe and China may see lower inflation as goods destined for the US seek an outlet in these regions.

President Trump sees unpredictability as a useful bargaining tool, but it also widens the range of economic outcomes. Fixed income markets dislike uncertainty and term premiums have risen on longer-dated US bonds as investors demand more compensation (higher bond yields) to lend for longer periods.

A well-worn path

But we should not fixate on tariffs. Most of the moves we have seen in fixed income markets reflect longer-term trends – not least the repricing of the cost of capital. The zero and negative interest rate policies that characterised the decade after the Global Financial Crisis are now viewed as an aberration.

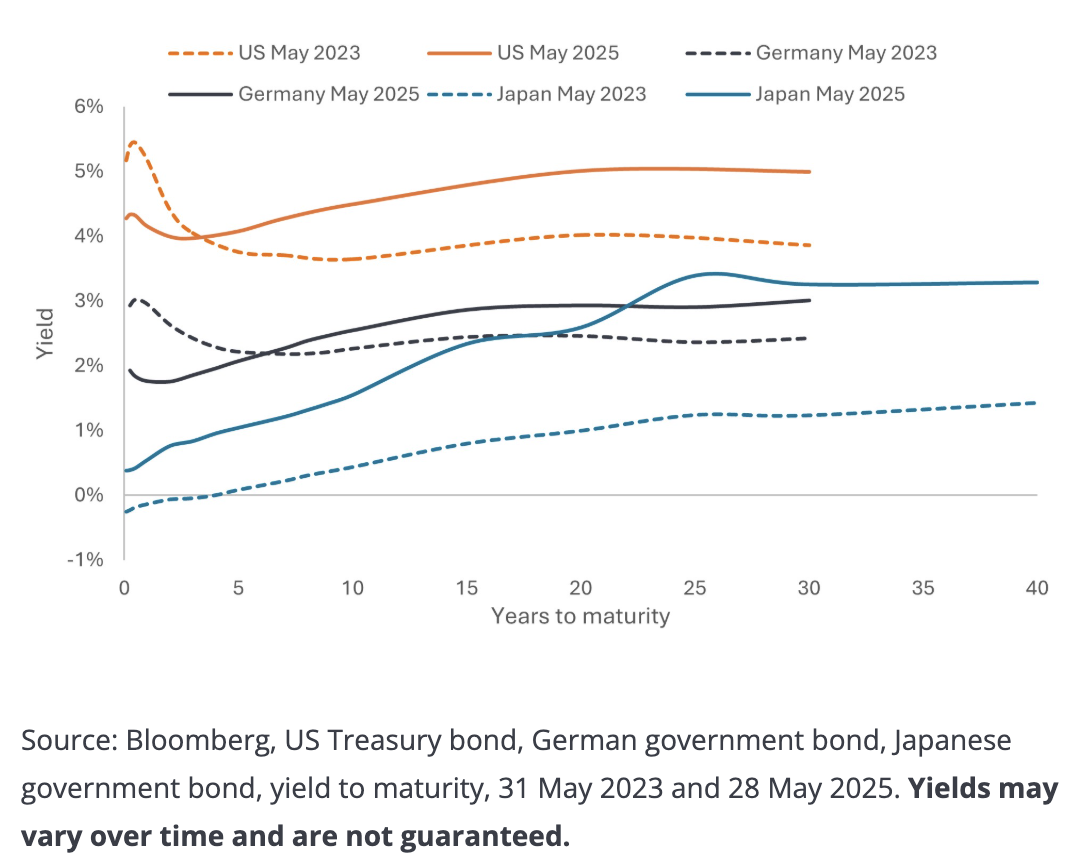

We have returned to a path where markets pay attention to debt. Many governments are lacking fiscal discipline (borrowing is high despite economies being at or near full employment) and defence spending is ramping up. Throw into the mix central banks actively shrinking their balance sheets and the onus is on the private sector to buy all the newly created government debt. Structural reform, such as the Dutch pension fund transition, meanwhile, is likely to encourage allocations towards equities. Longer-dated bond yields have therefore risen. This is a global phenomenon: yield curves, which plot government bond yields against their term to maturity, have steepened in Germany and Japan, not just the US (Figure 1).

Figure 1: Yield curves have steepened globally

The flip side of higher bond yields is that investors can harvest higher income. Coupon or interest income has historically been the biggest contributor to fixed income total returns over time. Do we think longer dated bonds are near their peak yields? Probably, but concerns about fiscal discipline, US Federal Reserve (Fed) independence (Jerome Powell’s term as Fed chair expires in May 2026), and the willingness – or otherwise – of overseas investors to hold US assets could create volatility in the coming months. That said, while there may be more willingness for non-US investors to diversify away from US Treasuries, we still see US Treasuries playing a critical role in investors’ portfolios for decades to come.

Consulting the map

Inflation has subsided globally from the highs of 2022, but its downward path had already started to flatten somewhat and that was before the potential impact from increased trade friction. Moderating inflation allowed major central banks (outside of Japan) to lower interest rates over the past 12 months and we see a path to further cuts from the European Central Bank (contained inflation) and the Bank of England (soft economic growth). If tariffs weigh on the US economy, we could see cuts before year-end, but the Fed has been vocal about needing to see more data. The collapse in the oil price could be a harbinger of impending economic weakness (and not just a reflection of rising OPEC output) but the Fed could face a credibility issue if it cuts interest rates with inflation above its target. The Fed will be keeping a watchful eye on inflation expectations (Figure 2). Much will depend on how labour markets play out over the coming months.

Figure 2: US inflation expectations

Some of the yield curve steepening described earlier reflects rate cuts, and any further cuts are likely to flow through to the front of the yield curve, with the impact on longer-dated bonds more equivocal. In such an environment, we believe high quality, shorter-maturity bonds offer more insulation from uncertainty. Investors may also look more globally, where the path to interest rate cuts is more clearly signposted.

Looking across the valley

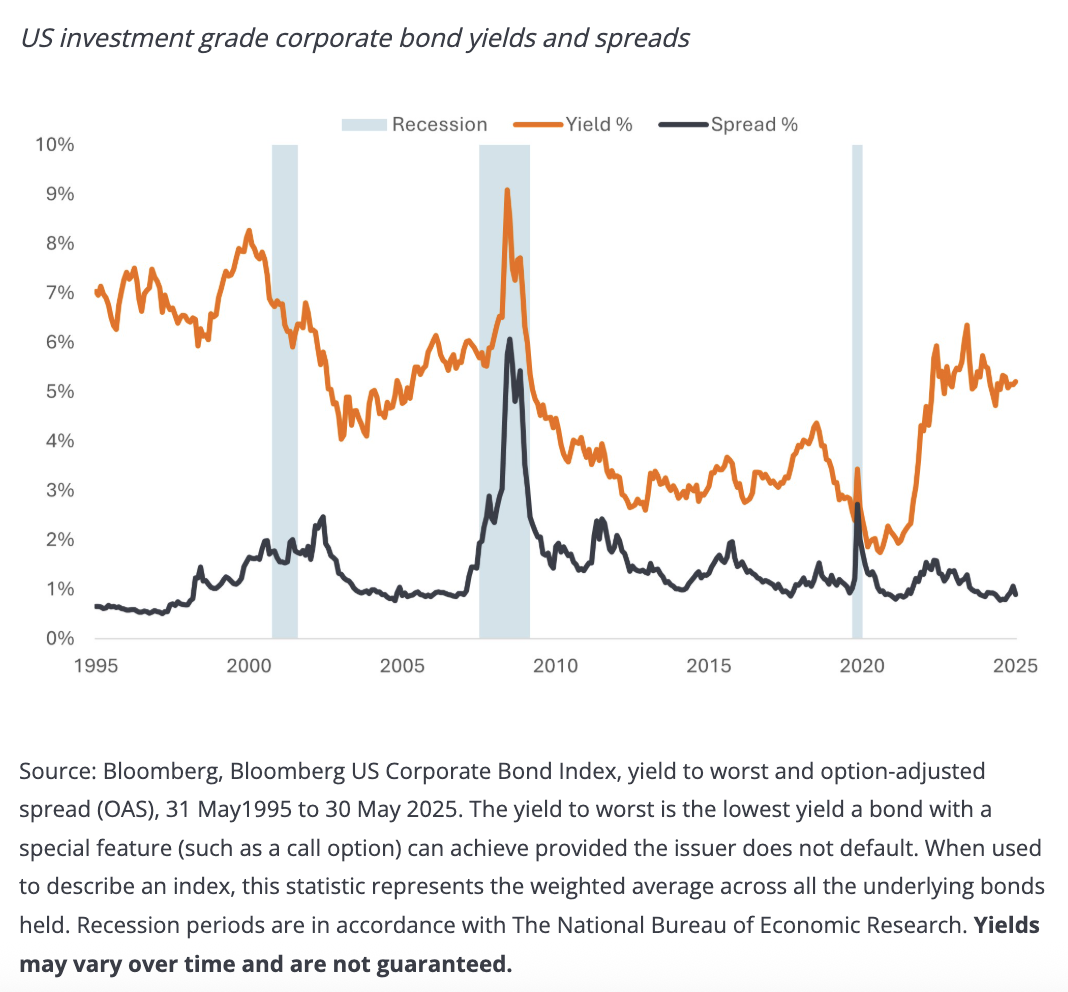

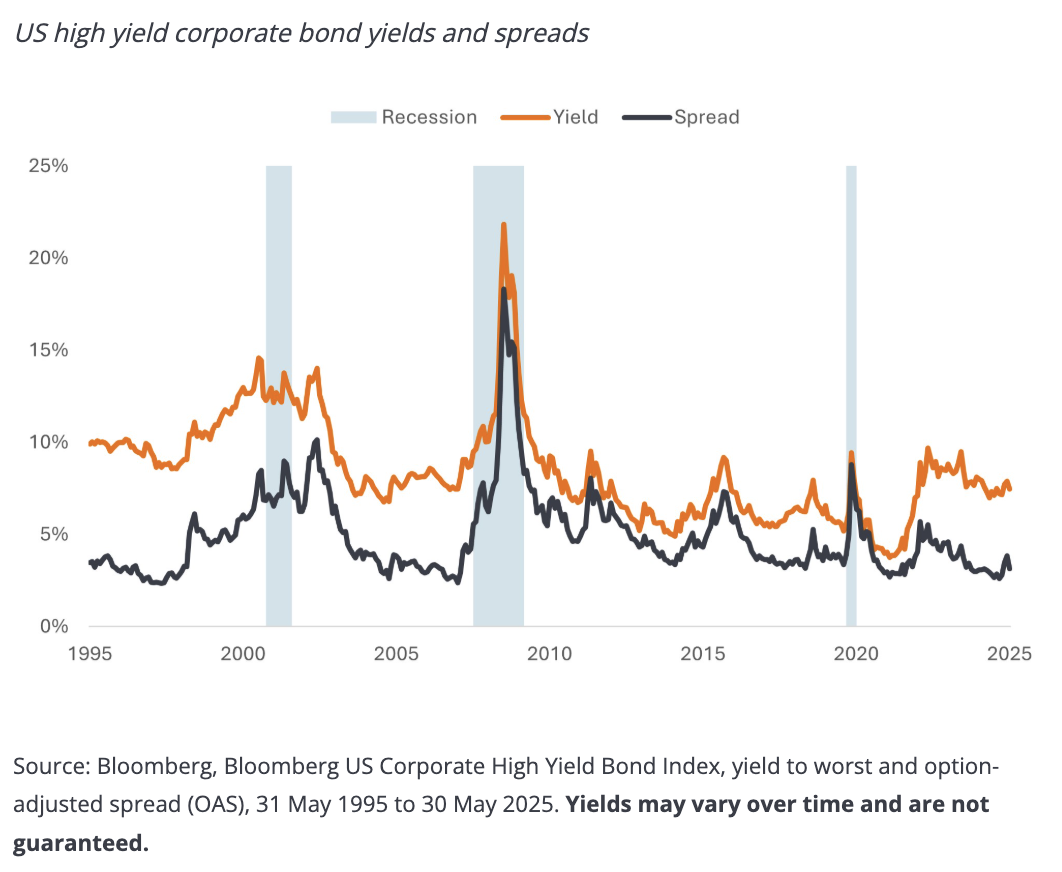

Credit spreads (the additional yield a corporate bond pays over a government bond of similar maturity) widened during the tariff panic in April but have since retraced those moves. Spreads are at relatively low levels historically and – in common with equity markets – are not pricing in a recession (Figures 3a,3b).

Figure 3a: Credit spreads are low but yields remain historically attractive

Figure 3b: Ditto in high yield

But do they need to? Trade uncertainty is likely to weigh on growth this year, but slower growth rather than recession remains the base case for most economists. Corporate bond fundamentals were strong before the tariff announcements, with many companies operating from a position of financial health with solid earnings. One could make the case that the tariff shock might be the equivalent of the energy crisis in 2015 or the eurozone debt crisis in 2011 and argue that spreads should be higher. But investors appear ready to look at today’s yields (which are comparable or higher to back then) and are willing to lend to companies, as evidenced by the strong appetite for new issuance.

Given the arguments on both sides, we see value in being nimble. Our preference is to favour corporate borrowers that are less exposed to trade disruption and have resilient business models, but with yields relatively high we stand ready to take advantage of price inefficiencies among riskier areas of the market.

Support from securitised

We have argued for some time that investors should consider the full range of the fixed income asset class. Securitised sectors may be unfamiliar terrain to many, but in our view they are attractively priced with high credit quality. Asset backed securities (ABS) and AAA-rated collateralised loan obligations (AAA CLOs) can offer alternate ways for investors to gain exposure to attractive yields with low duration, courtesy of their floating rate structure. Wide spread levels, low interest rate sensitivity and the amortising structure of AAA CLOs helped this area of fixed income prove resilient during the recent tariff volatility.

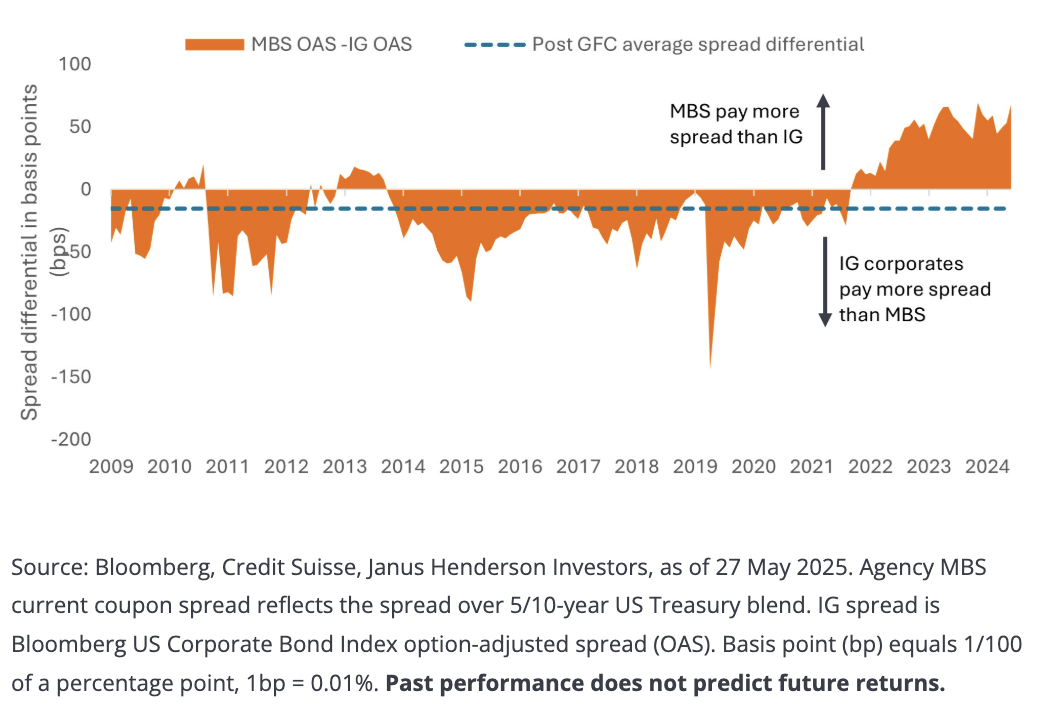

Agency mortgage-backed securities (MBS) continue to look attractive due to their relative cheapness versus investment-grade corporate bonds, their history of acting as a ballast when equity markets sell off, and their unusually low prepayment risk. Prepayment typically increases when interest rates fall and homeowners switch to lower rate mortgages. This can lead to MBS not fully capturing the gains from falling interest rates. Today, however, there is little incentive for US borrowers to repay their mortgage early when current mortgage rates are well above the levels at which the loans were taken out a few years ago.

In recent years, higher interest rates and quantitative tightening have weighed on MBS leading to the anomalous position where spreads are higher than on US investment grade (IG) corporates. With the prospect of quantitative easing (QE) ending and further rate cuts, we see this spread anomaly unwinding, making current levels a potentially attractive entry point (Figure 4).

Figure 4: MBS current coupon spread differential over US IG corporate spreads

Investors will always be confronted with a changing financial landscape. Right now, it may seem more challenging than usual, but we see the income offered by fixed income as providing a stabilising force, offering diversity to more turbulent equity markets. By having a well-stocked kit bag that blends different forms of fixed income, investors have the potential to gain exposure to varied income streams and help insulate against risk in a particular area. Through an active approach – one that harnesses enduring trends and moves tactically to capture opportunities – we believe investors can progress more surefootedly towards their investment goals.

A message from Advisor Perspectives and VettaFi: To learn more about this and othertopics, check out some of our webcasts.

IMPORTANT INFORMATION

Collateralized Loan Obligations (CLOs) are debt securities issued in different tranches, with varying degrees of risk, and backed by an underlying portfolio consisting primarily of below investment grade corporate loans. The return of principal is not guaranteed, and prices may decline if payments are not made timely or credit strength weakens. CLOs are subject to liquidity risk, interest rate risk, credit risk, call risk and the risk of default of the underlying assets.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

Mortgage-backed securities (MBS) may be more sensitive to interest rate changes. They are subject to extension risk, where borrowers extend the duration of their mortgages as interest rates rise, and prepayment risk, where borrowers pay off their mortgages earlier as interest rates fall. These risks may reduce returns.

Quantitative Tightening (QT) is a government monetary policy occasionally used to decrease the money supply by either selling government securities or letting them mature and removing them from its cash balances.

Quantitative Easing (QE) is a government monetary policy occasionally used to increase the money supply by buying government securities or other securities from the market

Securitized products such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed income securities.

Past performance does not predict future returns. There is no guarantee that past trends will continue or forecasts will be realised.

A message from Advisor Perspectives and VettaFi: To learn more about this and othertopics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All