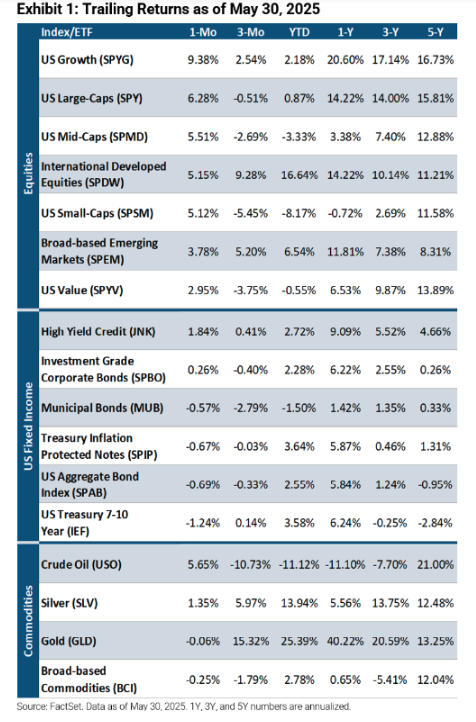

Despite inflation worries, fiscal deficit concerns, and continued geopolitical conflict, equity markets posted strong returns in May on the back of easing tariff tensions, lower probability of recession, and better than expected US Q1 earnings. Technology led the rebound as the Nasdaq Composite Index gained 9.7%, while the S&P 500 Index was up 6.3%, both posting their best monthly gains since November 2023. Following US growth and US large-caps, US mid-caps rose 5.5% while international developed equities also increased 5.2%. Aside from high yield credits (+1.8%) and investment grade corporates (+0.3%), bonds were mostly down as 7-10 year US Treasuries and the US Aggregate Bond Index both fell (-1.2% and -0.7%, respectively). Commodities produced mixed returns, with both crude oil and silver posting gains (+5.7% and +1.4%, respectively) while broad-based commodities and gold were down (-0.3% and -0.1%, respectively).

Fed Holds Rates Steady Amid Uncertain Outlook

The Federal Reserve held interest rates steady at the May FOMC meeting, keeping the fed funds rate in the 4.25–4.50% range. Policy members have stressed uncertainty around tariffs and the upcoming fiscal package, which cast a shadow over the economic outlook. Although inflation has eased, it remains above the Fed’s 2% target as April Core PCE (Personal Consumption Expenditures Index) printed at 2.5%. Fed Chairman Jerome Powell expressed “increased concern over the balance of risks,” emphasizing that persistent inflation combined with weakening labor and growth indicators could force difficult tradeoffs. The May FOMC minutes also revealed that officials see slower growth for 2025 and 2026 than their previous March estimate. Markets broadly expect the federal funds rate to remain at 4.25–4.50% range throughout the summer.

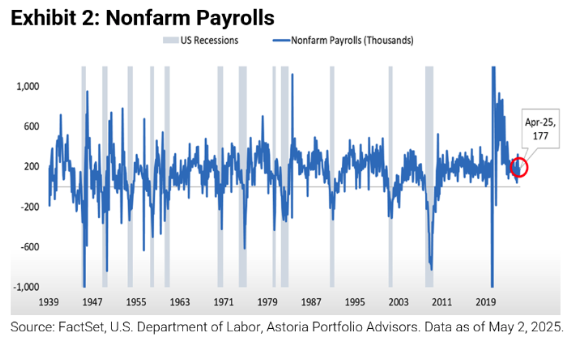

Nonfarm Payrolls Show Resilience

Despite weakness evidenced from Initial and Continuing Jobless Claims, JOLTS Job Openings and ADP Payrolls, the labor market displayed signs of resilience as Nonfarm Payrolls grew by 177k in April, exceeding the 133k estimate. The report also showed the unemployment rate was unchanged at 4.2%. Will job growth remain at such levels, or slow ahead?

US Earnings Revision Breadth Overtakes International

Although international markets have outperformed the US in 2025, earnings revision breadth (analyst upward and downward revisions to earnings) for the US has rebounded relative to that of international markets. Will US equities outperform for the remainder of the year?

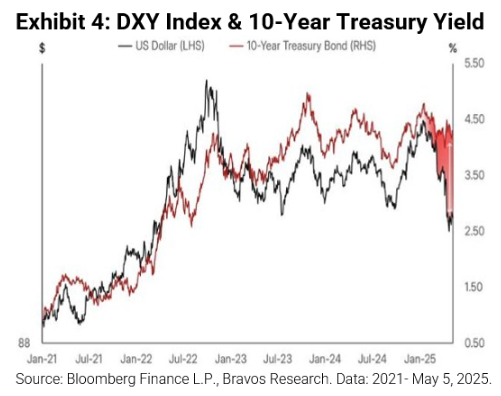

Yields Up, Dollar Down?

Typically, the dollar strengthens as US bond yields increase relative to other countries. However, this relationship has broken down recently with US rates rising and the dollar declining amid tariff policy uncertainty, foreign selling of US assets, and a significant deficit coupled with an anticipated fiscal package.

Cautious Optimism: Shift Exposure, Stay Balanced

As we look ahead, we remain grounded in a framework of cautious optimism. Persistent fiscal slippage, rising term premiums, and ballooning interest costs suggest that investors should not ignore growing structural risks. Yet, equities have been gradually broadening out, and we believe the macro backdrop for 2H 2025 appears more favorable amid a shift in policy focus and improving earnings revision breadth. Here are our latest portfolio views:

- Rotate portfolios away from the Magnificent 7. This doesn’t mean completely selling out of SPX or NDX—but it does mean tilting exposure away from hyper-concentration.

- Favor pro-growth sectors like technology and inflation-linked ones (industrials/materials/energy), but hedge with some defensive positioning in case the economic recovery proves nonlinear.

- Increase mid-cap exposure, where we see compelling valuation and growth dynamics.

- Use international equities for diversification. International developed markets have outperformed SPX by over 16% YTD.

- Maintain a slight overweight to US equities but remain neutral between equities and bonds overall.

- Tariff-related uncertainties are expected to ease.

- Trump is continuing to shift toward pro-growth policies (tax cuts, deregulation).

- Revision breadth is well off the lows. We view this as a leading indicator for forward EPS growth and a key barometer of corporate confidence.

Click here to view this report as a PDF.

Originally published June 2, 2025.

For more news, information, and strategy, visit the ETF Strategist Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by Astoria Portfolio Advisors