A Focus on Fundamentals

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Observations

Government Debt Is High—Corporate Debt Is Not

While the immediate path for tariffs may drift lower, the U.S. legislative branch is hammering out a tax and spending bill that seems to favor tax cuts over lower spending, reviving worries over the U.S. budget deficit and a growing debt burden that cannot be ignored.

Total federal debt, as a percentage of GDP, has doubled in the last 20 years.[1] In 2025, the Moody’s U.S. downgrade, rising longer-term Treasury yields, a falling U.S. dollar, and a rally in Bitcoin can all point to this rising debt burden as a key driver. But equities, meanwhile, don’t seem to notice, in part because corporate debt is near all-time lows. Over the last 20 years, net debt/EBITDA for the S&P 500 has fallen by roughly two-thirds.[2] Lower debt and leverage may blunt the impact of rising interest rates on companies—at least for a while.

Still, investors need to consider fundamentals like debt and leverage when assessing the risk and opportunity of stocks. Valuations currently appear full, especially given the combined and possible long-term impact of rising federal debt and tariffs that are still likely to end up higher than pre-election levels. And while the U.S. may avoid stagflation, inflation could prove sticky and growth muted. In such a scenario, even solid fundamentals can prove fleeting. Consider what’s happened in the energy sector over the past few years.

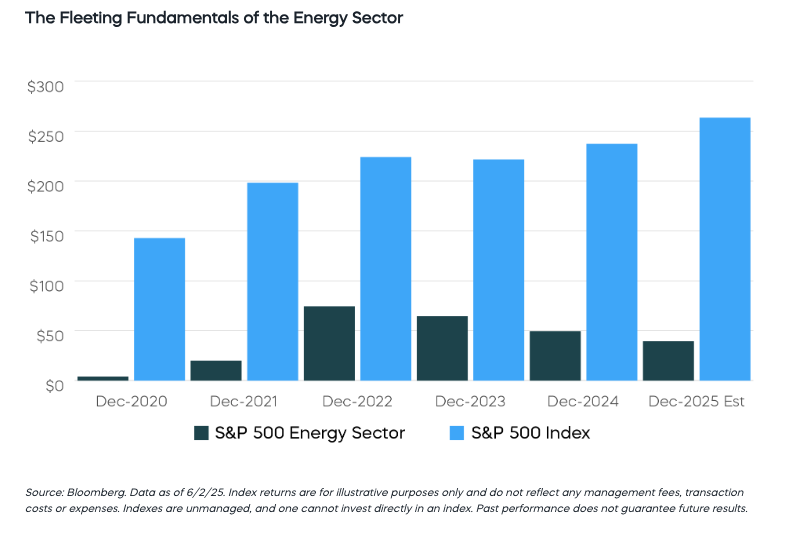

Chart of the Month

It wasn’t long ago that the energy sector was a darling of fundamental investors. Strong earnings (and cash flow, EBIT, and EBITDA) in 2022 led many to invest heavily in the sector—to their detriment. In the end, they invested at the peak of oil prices. Since then, from late 2022 through May of this year, the sector has remained largely flat, while the S&P 500 has returned nearly 60%. Investors narrowly focused on fundamentals need to consider the stability and growth of those fundamentals as well.

Asset Class Perspectives

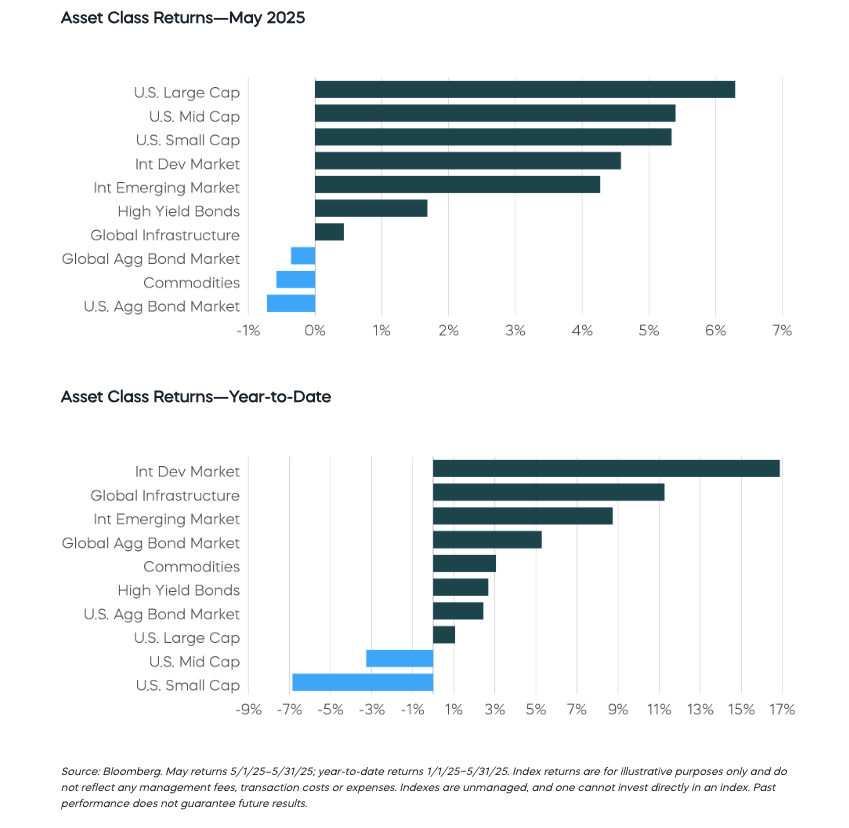

Global equities rallied in May as trade tensions eased, with U.S. large-cap stocks posting their strongest monthly performance in 35 years. Credit spreads in both investment-grade and high-yield corporate bond markets tightened, reversing most of their April widening. Meanwhile, commodities and global bonds saw modest declines, and gold prices remained largely unchanged.

Asset Class Perspectives

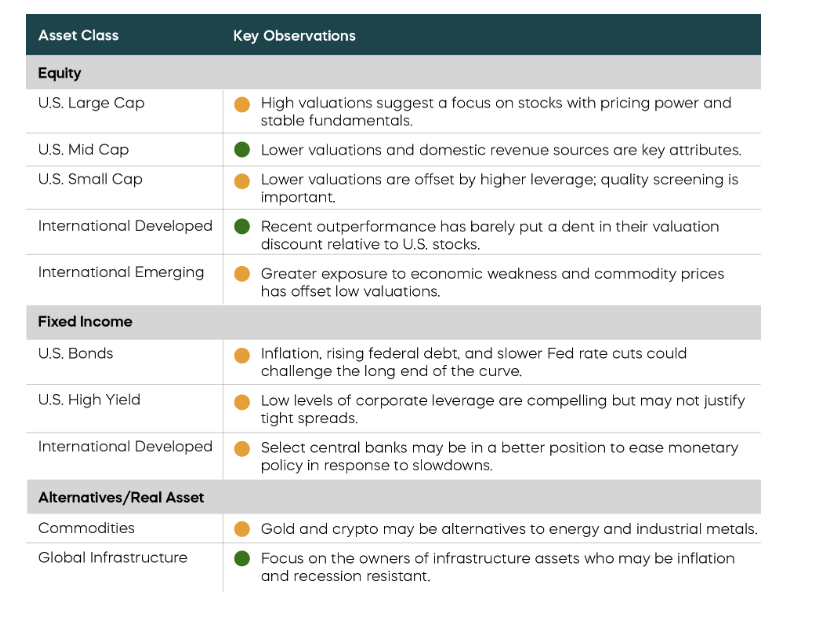

The following are observations on a range of asset classes. For each, green indicates a constructive backdrop, yellow indicates a neutral environment, and red indicates a challenging backdrop.

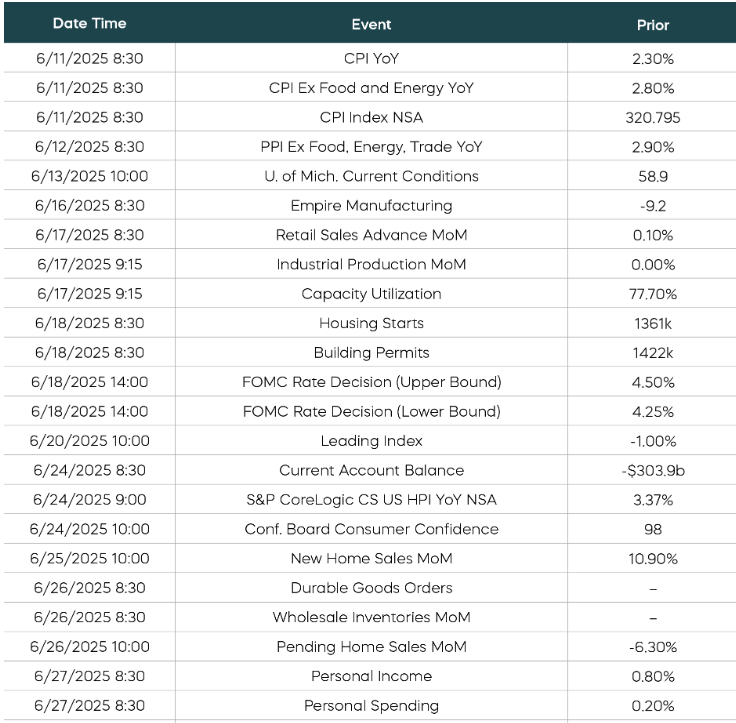

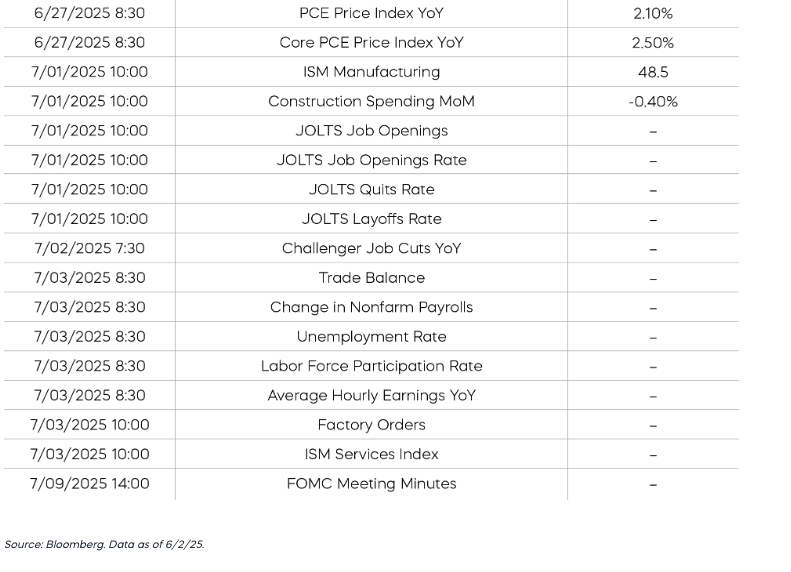

Economic Calendar

Here is a list of key and upcoming economic releases, which may serve as a guide to potential market indicators.

Equity Perspectives

April Tariffs Bring a May Stock Rally

The S&P 500 delivered returns of 6.3% last month, marking its best May performance since 1990, according to Standard & Poor’s. Performance was so consistently good that the index never fell below its starting level during the month. In addition to being consistent, the rally was broad-based. Ten of the 11 S&P sectors posted gains (only health care was negative) as did most styles, measured through the lens of factors. Mid- and small-cap stocks also participated. Despite fluctuating court rulings on trade policy late in the month, the tariff de-escalation trend has been positive for stocks. While it seems that we may live with some tariffs, they are becoming less relevant to investors as summer arrives.

Stock performance since early April has been a roller-coaster and brings fundamentals clearly back in focus. Large-cap valuations may not be cheap, but their profit picture has been favorable. NVIDIA’s solid earnings capped off a generally strong Q1 earnings season in which S&P 500 companies delivered earnings growth north of 13%.

Focus on the Fundamentals with Staying Power

As this year began, it was our view that mid-cap stocks could become a compelling opportunity. With favorable valuations and healthy earnings expectations, they generally offered a better fundamental outlook than large caps. Tariff developments have strengthened that view, as mid-caps generate most of their revenues domestically, potentially insulating them from the brunt of any trade-related fallout.

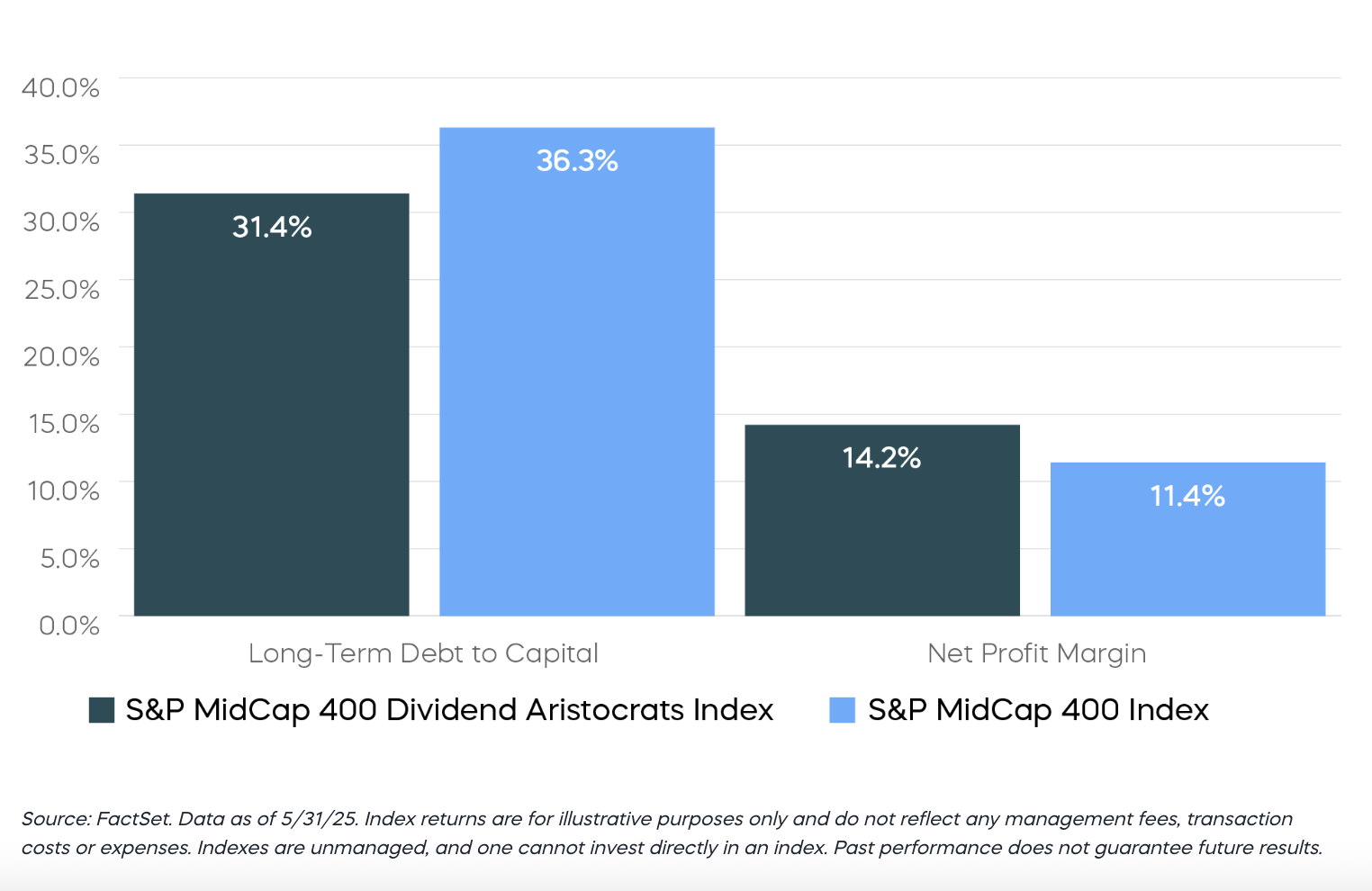

Looking ahead, our focus is not only on stocks with strong fundamentals, but also those with potential staying power. The S&P MidCap 400 Dividend Aristocrats are a good example. Companies that have raised their dividends for a minimum of 15 consecutive years across a variety of economic conditions are signaling their belief in the underlying strength of their businesses and management’s confidence in their ability to sustain revenue growth, profits and cash flows.

The signal this should send to investors is one of potential long-term quality. Companies with long track records of dividend growth generally have durable competitive advantages and solid fundamentals. And the S&P MidCap 400 Dividend Aristocrats typically generate higher net profit margins and carry lower levels of debt than companies in the broader S&P MidCap 400.

Dividend Aristocrats Typically Have Higher Margins and Lower Debt

Fixed Income Perspectives

Let the Dust Settle

In last month’s commentary, we asked whether the shifting macro environment calls for a reevaluation of long-term U.S. Treasury bonds. Specifically, would investors begin demanding a higher risk premium leading to higher yields on longer-duration Treasuries?

While U.S. Treasuries have historically served as a premier safe-haven asset, offering diversification during equity market drawdowns, we noted that they sold off alongside equities following the April 2 tariff announcements. Since then, equity markets have rebounded sharply from their April lows, driven in part by temporary tariff pauses and the announcement of a “total reset” in trade with China. But despite this rally in risk assets, demand for Treasuries from asset allocators who use them to build diversified portfolios appears yet to have recovered meaningfully.

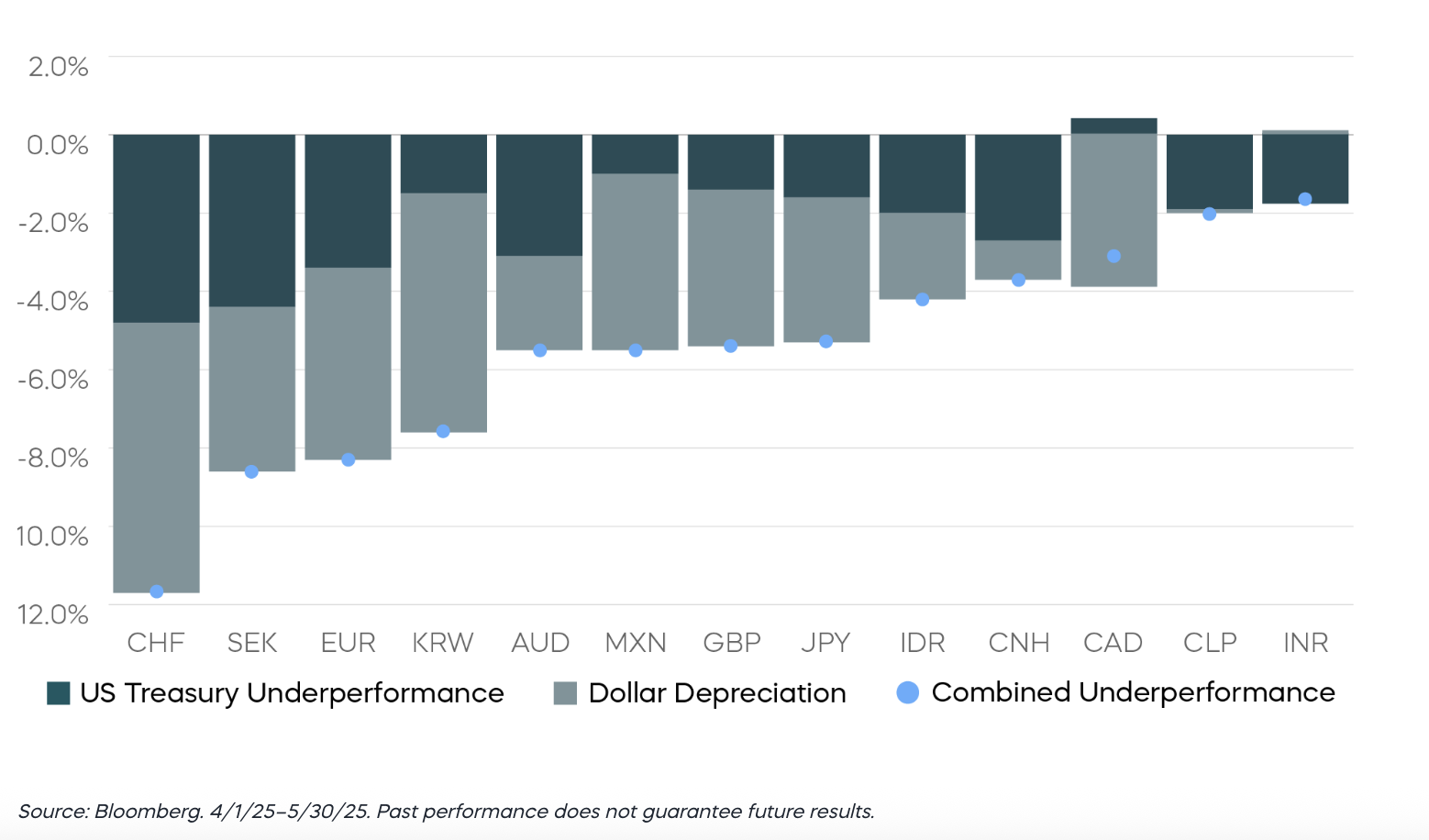

Historically, the U.S. Treasury’s status as a global safe asset has led to lower yields compared to foreign sovereign bonds. But since “Liberation Day,” Treasury yields have risen relative to both developed- and emerging-market sovereign debt. Even more notable is the fact that the U.S. dollar has depreciated against many of these same foreign currencies, despite U.S. interest rates rising faster than their global counterparts. Nearly two months after the initial tariff announcement, and more than halfway through the 90-day truce, U.S. Treasuries remain underperformers, in terms of both higher relative change in yields and due to a weaker dollar.

10-Year Treasuries Remain Underperformers Against Foreign Sovereigns

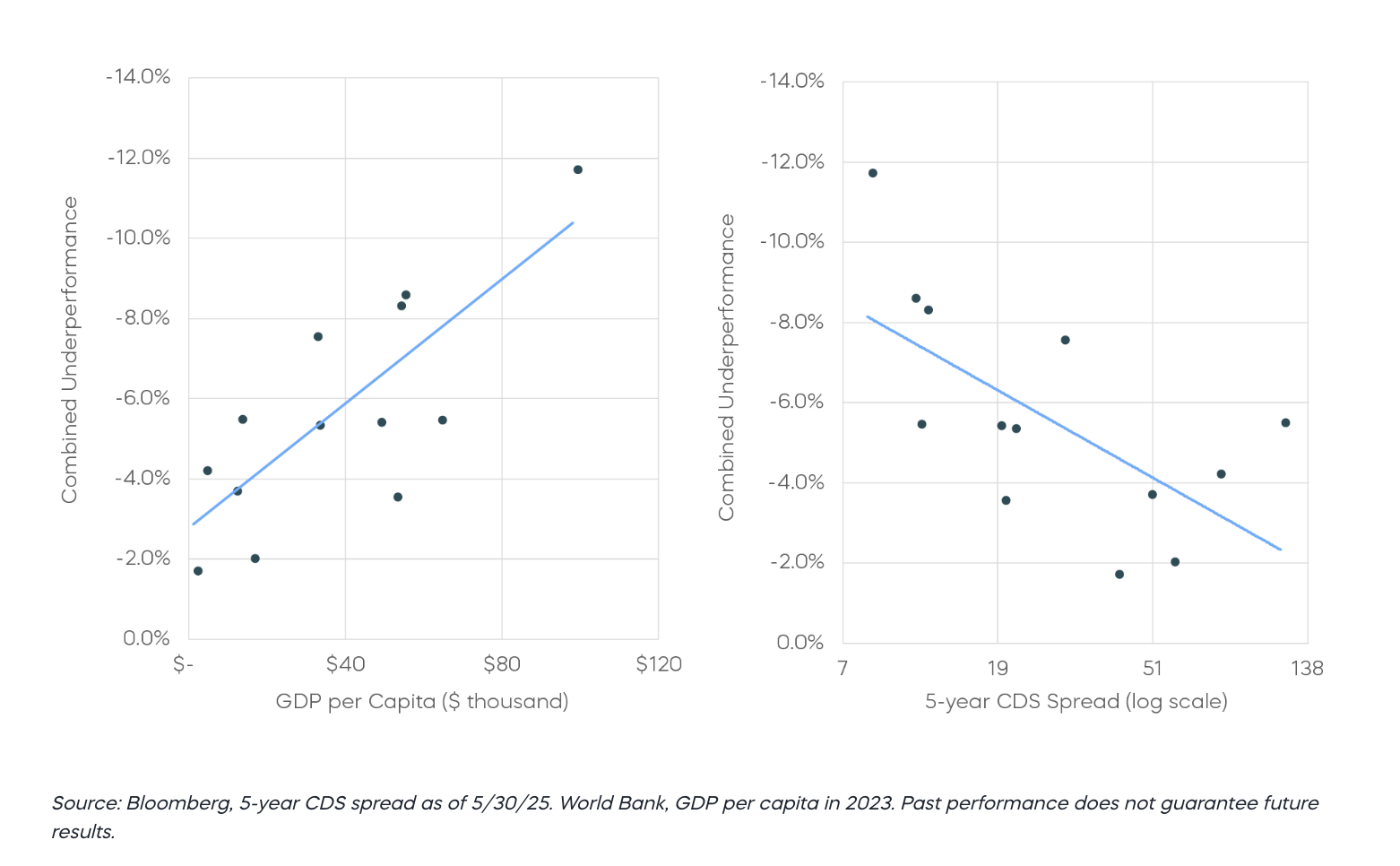

Compared to global sovereigns, the underperformance of Treasuries is most pronounced against bonds from developed economies that could potentially serve as alternative safe assets. For instance, U.S. Treasuries have declined the most against sovereign bonds issued by countries with higher per-capita GDP. And if we use five-year credit default swap (CDS) spreads as a proxy for credit quality, the strongest performance has come from countries with lower CDS spreads (i.e., those perceived to have lower default risk).

Underperformance of U.S. Treasuries Most Pronounced Against Developed Economies

The rotation away from U.S. Treasuries may continue to play out over the long term, though fundamental factors such as growth and inflation have also contributed to rising yields in the near term. Recent easing of trade tensions, along with the anticipated tax bill, may offset the effects of slowing growth. At the same time, an expanding fiscal deficit and the structural use of tariffs as a mild consumption tax could generate inflationary pressures going forward, even though backward-looking inflation has moderated recently.

This growth and inflation backdrop may limit the Fed’s ability to deliver aggressive rate cuts, potentially keeping long-term yields elevated even if short-term yields decline in response to rate cuts. Between April 1 and the end of May, market pricing for expected rate cuts during 2025 has adjusted only modestly, down from three 25-basis-point cuts to about two. Moreover, what was priced out of 2025 has largely been deferred into 2026, implying a similar magnitude of total easing over time.

Going forward, fluctuations in growth and inflation data could become key drivers of rate expectations. At current levels, markets do not yet seem to have priced in a significant slowdown in future cuts. If economic growth remains steady, expectations may shift toward more patience from the Fed, potentially placing further upward pressure on yields.

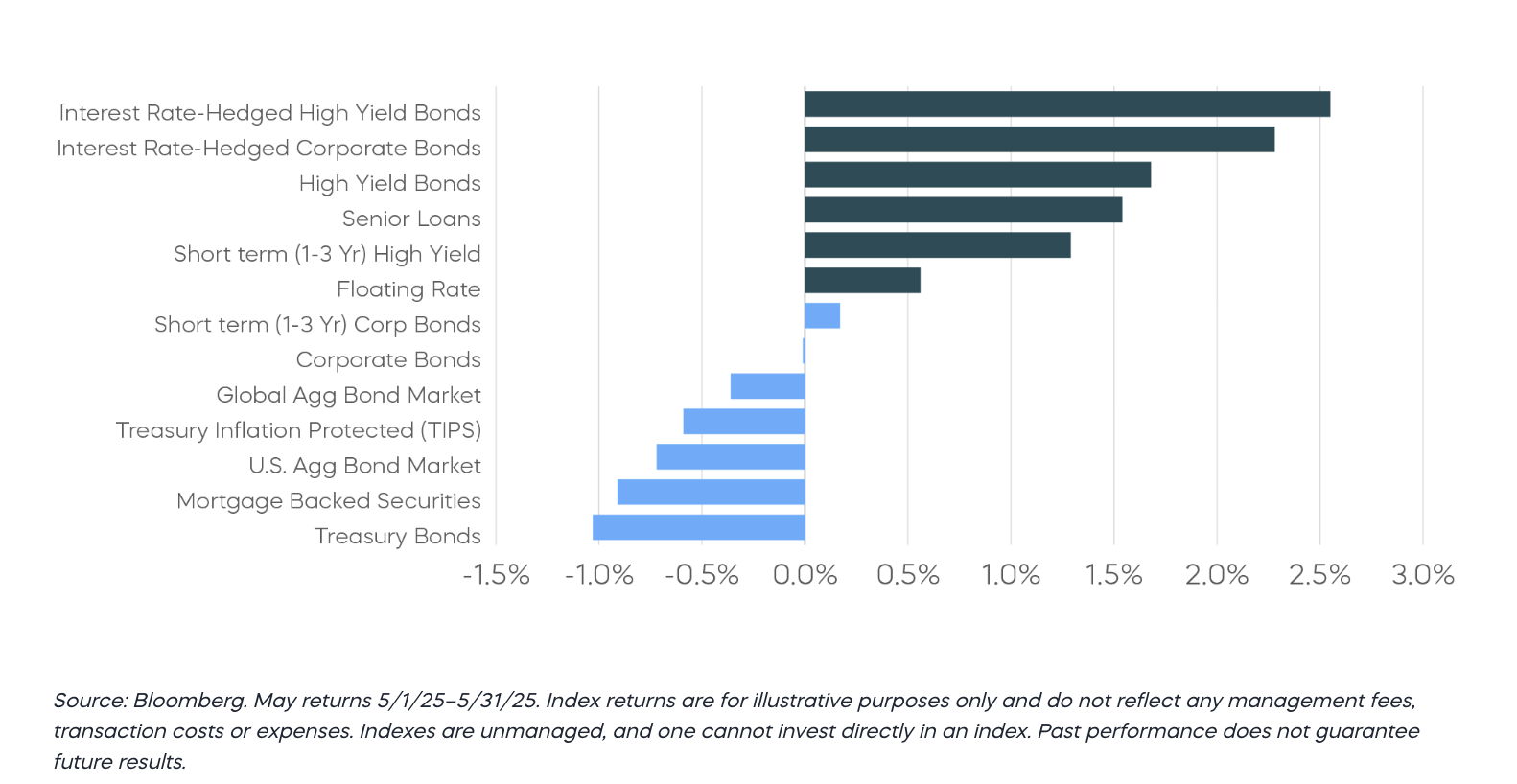

It may be prudent to consider a tactical reduction in interest rate risk over the near term for investors maintaining corporate bond allocations at benchmark durations. As an example, rate-hedged investment-grade corporate bonds delivered some of the strongest returns across fixed income categories in May, benefiting from credit spreads that largely returned to pre-April levels. In contrast, investment-grade corporate bonds with full duration exposure posted negative returns during the same period, highlighting the impact of rising rates.

Fixed Income Returns—May 2025

[1] Source: Federal Reserve Bank of St. Louis, data as of 9/26/2024.

[2] Source: Bloomberg, data as of 6/2/2025.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Sources for data and statistics: Bloomberg, FactSet, Morningstar, and ProShares.

The different market segments represented in the performance recap charts use the following indexes: U.S. Large Cap: S&P 500 TR; U.S. Large Cap Growth: S&P 500 Growth TR; U.S. Large Cap Value: S&P 500 Value TR; U.S. Mid Cap: S&P Mid Cap TR; U.S. Small Cap: Russell 2000 TR; International Developed Stocks: MSCI Daily TR NET EAFE; Emerging Markets Stocks: MSCI Daily TR Net Emerging Markets; Global Infrastructure: Dow Jones Brookfield Global Infrastructure Composite; Commodities: Bloomberg Commodity TR; U.S. Bonds: Bloomberg U.S. Aggregate; U.S. High Yield: Bloomberg Corporate High Yield; International Developed Bonds: Bloomberg Global Agg ex-USD; Emerging Market Bonds: DBIQ Emerging Markets USD Liquid Balanced.

The different market segments represented in the fixed income returns charts use the following indexes: Global Agg Bond Market: Bloomberg Global-Aggregate Total Return Index Value Unhedged USD; Mortgage Backed Securities: Bloomberg U.S. MBS Index Total Return Value Unhedged USD; Treasury Bonds: Bloomberg U.S. Treasury Total Return Unhedged USD; U.S. Agg Bond Market: Bloomberg U.S. Agg Total Return Value Unhedged USD; Corporate Bonds: Bloomberg US Corporate Total Return Value Unhedged USD; High Yield Bonds: Bloomberg U.S. Corporate High Yield Total Return Index Value Unhedged USD; Interest Rate-Hedged High Yield Bonds: FTSE High Yield (Treasury Rate-Hedged) Index; Treasury Inflation Protected (TIPS): Bloomberg U.S. Treasury Inflation Notes TR Index Value Unhedged USD; Short term (1-3 Yr) High Yield: Bloomberg U.S. Corporate 0-3 Year Total Return Index Value Unhedged USD; Senior Loans: Morningstar LSTA U.S. Leveraged Loan 100 Index; Short term (1-3 Yr) Corp Bonds: Bloomberg U.S. Corporate 1-3 Yr Total Return Index Value Unhedged USD; Floating Rate: Bloomberg U.S. FRN < 5 yrs Total Return Index Value Unhedged USD; Interest Rate-Hedged Corporate Bonds: FTSE Corporate Investment Grade (Treasury Rate-Hedged) Index.

The S&P 500 is a benchmark index published by Standard & Poor's (S&P) representing 500 companies with large-cap market capitalizations. The S&P 500 Energy comprises those companies included in the S&P 500 that are classified as members of the GICS energy sector. The S&P MidCap 400 is a benchmark index published by Standard & Poor's (S&P) representing 400 companies with mid-cap market capitalizations. The S&P MidCap 400 Dividend Aristocrats Index targets companies that are currently members of the S&P MidCap 400 that have increased dividend payments each year for at least 15 years.

This is not intended to be investment advice. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results.

Any forward-looking statements herein are based on expectations of ProShare Advisors LLC at this time. Whether or not actual results and developments will conform to ProShare Advisors LLC’s expectations and predictions, however, is subject to a number of risks and uncertainties, including general economic, market and business conditions; changes in laws or regulations or other actions made by governmental authorities or regulatory bodies; and other world economic and political developments. ProShare Advisors LLC undertakes no duty to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Investing involves risk, including the possible loss of principal. This information is not meant to be investment advice.

The “S&P 500®,” “S&P MidCap 400®,” “S&P MidCap 400® Dividend Aristocrats® Index, and “S&P 500® Energy” are products of S&P Dow Jones Indices LLC and its affiliates. "S&P®" is a registered trademark of Standard & Poor’s Financial Services LLC (“S&P”), and “Dow Jones®" is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”) and they have been licensed for use by S&P Dow Jones Indices LLC and its affiliates. All have been licensed for use by ProShare Advisors LLC. ProShares ETFs based on these indexes are not sponsored, endorsed, sold or promoted by these entities or their affiliates, and they make no representation regarding the advisability of investing in ProShares ETFs. THESE ENTITIES AND THEIR AFFILIATES MAKE NO WARRANTIES AND BEAR NO LIABILITY WITH RESPECT TO PROSHARES.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All