Assessment and selection of covered call funds is based on criteria like total return, distribution rate (sometimes referred to as yield), and fees. Total return may be the most important as it drives the long-term sustainability of a fund’s distributions.

Total return in covered call strategies consists of three components: dividends collected, option income profits or losses, and capital appreciation or depreciation. A covered call fund or strategy selection should include consideration of a manager’s reliance on and relative strength in all three components, as each contributes to total return differently in various market conditions.

This post explores the expected performance of the components in different markets and their relative contribution to total return.

Covered Call Writing: Adding a Contributor to Total Return

Traditionally stocks and stock-based funds generate returns via two methods: the price appreciation of the stock itself and the dividends issued by the management of a company. These two components are the drivers of total return.

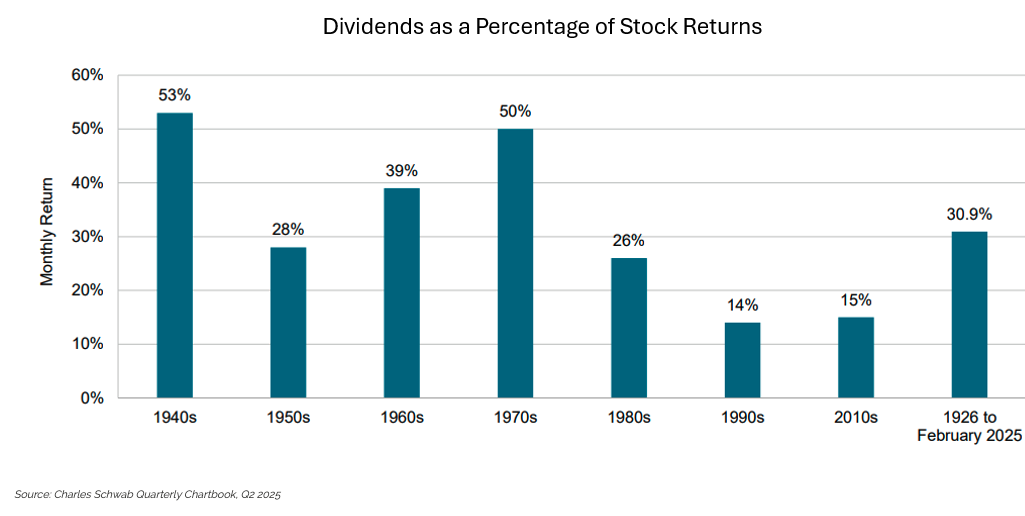

However, over the last couple of decades the dividend component of total return has become less important and investors more dependent upon price appreciation or capital gains to drive total returns. While the long-term average dividend rate for the S&P 500 from 1926 to 2024 was 4.0%, in each of the decades starting in 1990’s the dividend returns have been below its long-term average.

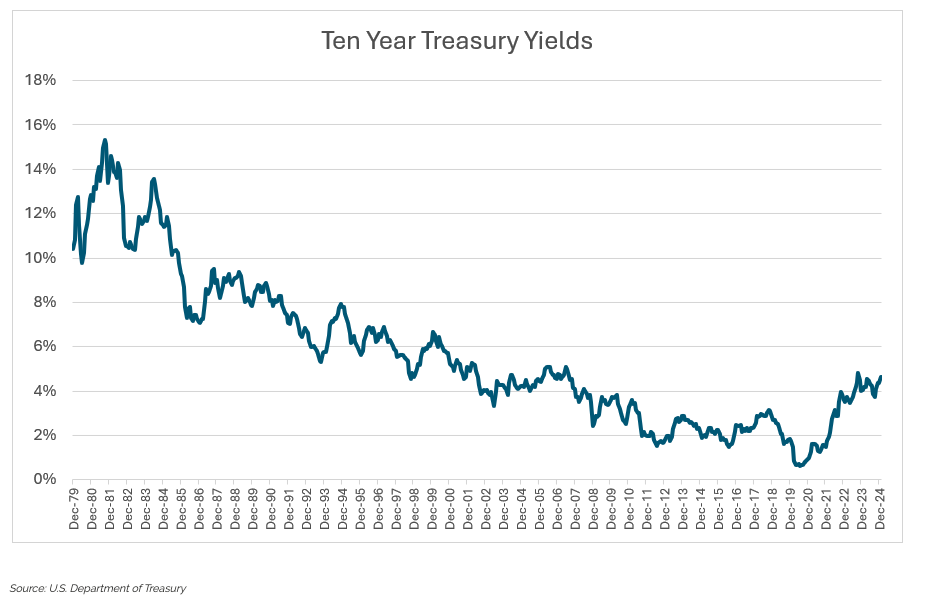

Unfortunately for income-seeking investors, this period of low equity dividends has coincided with the era of exceptionally low bond yields. In response to the Dot-Com Bust, the Global Financial Crisis, and the Covid-19 Pandemic, the Fed kept interest rates at very low absolute levels. Those seeking yield were starved over most of the 21st century.

This lack of yield from traditional means led investors to seek income from alternative sources. Derivative income or covered call strategies attempt to add a third component to total return: the collection of option premium via the writing of call options.

Derivative income funds are typically used as a vehicle to distribute capital to investors. By diversifying across capital appreciation, dividends, and call option premiums a fund could generate a total return over most market conditions that would allow the fund to make regularly scheduled distributions to investors, which may meet some portion of their “income” needs. This helps address the shortage of yield from equity dividends or traditional bonds alone.

However, there is a fundamental trade-off between writing calls for income today versus capital appreciation for the long-term. It is difficult, but not impossible, to accomplish both when it comes to a covered call strategy. Swan believes that active management of both the equity component as well as the option component of a covered call strategy can optimize the balance between the two.

Covered Call Components: Contribution to Total Return in Various Conditions

In a covered call strategy stock price return, dividends, and option premium, are expected to perform differently in different market environments.

Bull Markets- during bull markets, price appreciation is the primary driver of total return. Equities have been one of the few major asset classes to offer real, inflation-adjusted growth over the long run. Long-term capital appreciation allows an investor to draw down capital gains over time and fund their potential income needs.

Dividends can also contribute to gains in a bull market. If a company is on a sustained period of success, they are more likely to increase their dividends.

However, during bull markets call writing becomes more challenging. If the asset’s price gains exceed the strike price of the call option, the writer of the call forgoes any future gains past the strike price. During bull markets, call writing tends to be defensive in nature, where the portfolio manager is attempting to minimize the risk of call options going “in-the-money.”

Active risk management can be particularly useful when writing call options in bull markets. A passive call writing strategy sells a call and then “lets the chips fall where they may.” If the underlying stock or equity has a breakout to the upside, a passively managed strategy can’t defend against that risk and forgoes the gains beyond the strike price.

Conversely, an actively managed covered call strategy seeks to strike the right balance and can adjust the short call trades or choose not to engage in them at all in an attempt to capture more of the capital appreciation in a bull market.

Flat or slightly rising markets – capital appreciation is less of a factor in a slightly rising or a flat market. In a slightly rising market, the equities in a covered call strategy might generate modest gains from capital appreciation; in a flat market the equities might not generate any capital gains. This is where the other two components come in.

Dividends from stocks tend to be stable over time, so even in flat markets dividends may play a role in generating positive returns.

A flat or slightly rising market tends to be a favorable environment for call writing. The ideal situation would be if the underlying stocks had gains up to, but not exceeding, the strike prices of the written call options. In this best-case scenario, the covered call strategy could potentially enjoy the modest capital gains of a slightly rising market, not surrender any gains past the strike price, and keep the premium generated by the writing of the call option. Of course, this is a delicate balancing act – the portfolio manager must balance the future upside potential of the equities against the immediate gratification of writing options on those same equities. This is another case where active management is quite useful.

Active management in covered calls can also take the form of writing calls on individual equities. If the strategy is writing calls on just the index, the index can be in one of three states: down, flat, or up. This limits the opportunities for profit. However, if the strategy is writing call options on a portfolio of many stocks, it is likely that at any given moment some of the equities will be down, some will be flat, and some will be up. The opportunity set, and thus profit potential, is expanded if one chooses to write options on individual names.

Down markets – In a down market, it is likely the equity portfolio will be a source of losses. A broad downturn in the market would likely negatively impact the prices of stocks in the fund’s portfolio. If the fund is passively managed it is reasonable to expect the equity portfolio to be down in-line with the benchmark index. If the fund is actively managed the fund could possibly sidestep some of the market losses if they favor defensive stocks and take some steps to diverge away from the index. That said, it is unlikely that during a market downturn the equity portfolio of a covered call strategy would avoid all the market losses.

That said, those stocks are still likely to maintain some level of dividends. Companies are very reluctant to cut dividends, as the market generally views it as a signal of weakness. Therefore, even in down markets a company will attempt to maintain its dividend payments as a “show of strength.”

Finally, covered call writing tends to do well in down markets. The option writer collects the premium from writing a call option. If the asset is below the strike price of the option at the time of expiration, the writer is free from further obligation. A down market could provide the opportunity to repeat this process of writing options and keeping the premium multiple times. This helps offset the downward drift in prices on the equity portfolio side. While covered call writing is not an explicit hedge on the portfolio, call writing is accurately described as a “bearish” position on the asset.

A covered call strategy that chooses to write calls on individual names might also benefit from the elevated premiums available in the options on individual equities. Premiums are a function of volatility, and the volatility of individual stocks is almost always higher than the volatility of a broad-based index. Therefore, a strategy writing calls on individual names may have more profit potential than a strategy writing calls on a passively managed index.

Bear markets – in deep bear markets it is reasonable to assume that a covered call strategy would have losses. While call writing and dividends would likely provide some positive returns in a bear market, it is unlikely that those two elements would offset the scale of losses that mark a true bear market.

From a risk management perspective, Swan has always believed hedging via put options plays a vital “capital preservation” role within a portfolio. While a call writing strategy can do well in many market environments, having a dedicated hedged equity strategy to complement an income strategy is a prudent approach if one seeks to mitigate downside risk. As an options-focused manager, Swan believes investors will benefit from utilizing options-based strategies as alternate sources of income and risk mitigation within a portfolio.

If one expects a constant, stable distribution from a derivate income or covered call fund, it is unlikely that any one of these factors can solely produce the level of “income” desired by the shareholders. Rather, it is the three drivers of capital appreciation, dividends, and call writing working together to forge the total returns needed to generate distributions reliably and without dipping into an investor’s principal investment.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Important Disclosures:

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan offers and manages the DRS for investors including individuals, institutions and other investment advisor firms.

All Swan products utilize the Defined Risk Strategy (“DRS”), but may vary by asset class, regulatory offering type, etc. Accordingly, all Swan DRS product offerings will have different performance results due to offering differences and comparing results among the Swan products and composites may be of limited use. All data used herein; including the statistical information, verification and performance reports are available upon request. The adviser’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the adviser invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. Further information is available upon request by contacting the company directly at 970-382-8901 or www.swanglobalinvestments.com. 094-SGI-052825

© Swan Global Investments

Read more commentaries by Swan Global Investments