At Research Affiliates, we are always on the lookout for markets where valuations offer a compelling case for long-term investors. While the strength and resilience of U.S. large caps continue to dominate the global equity conversation, our current research suggests that developed markets outside the United States are quietly reasserting themselves as a fertile ground for return-seeking allocators.

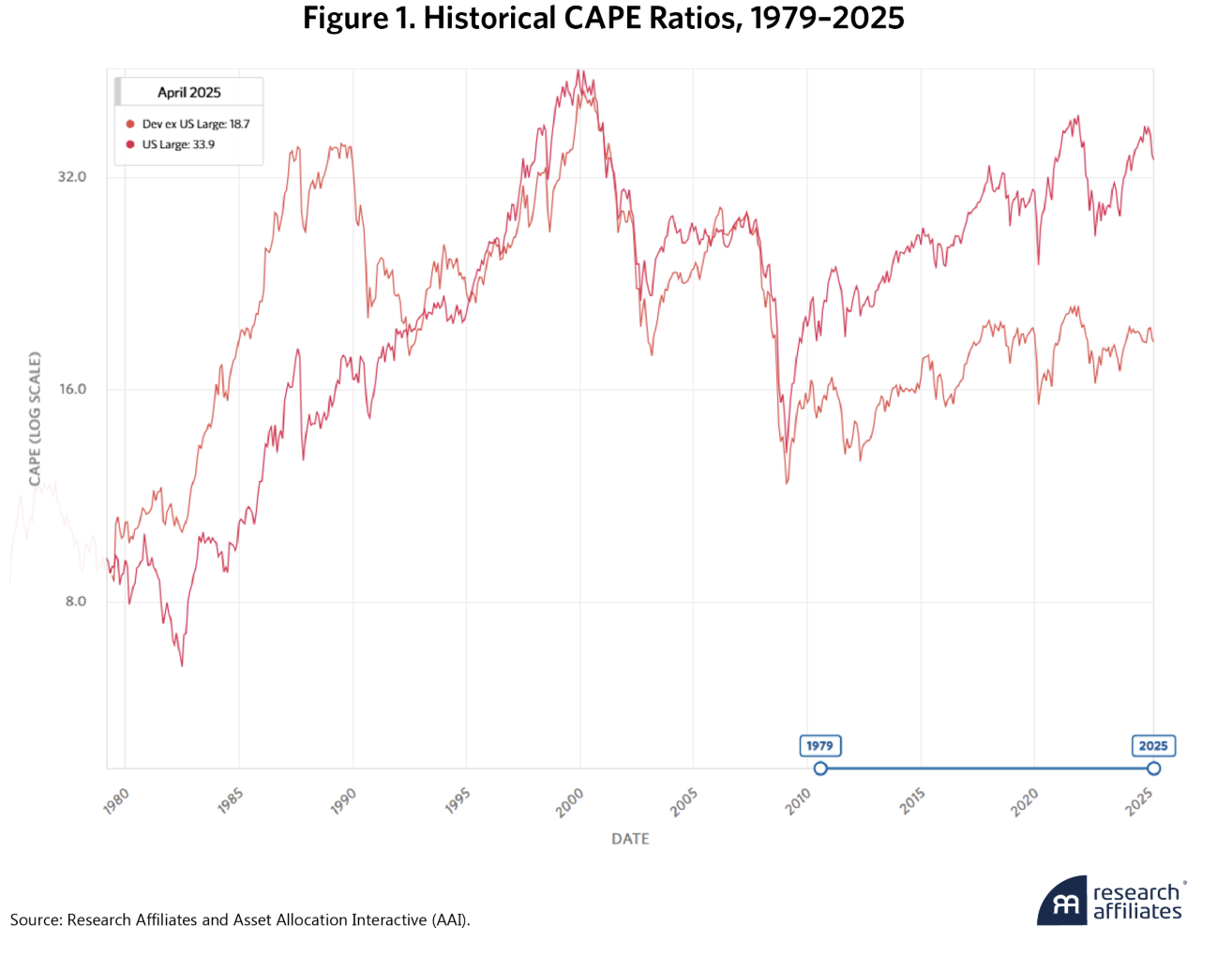

Despite strong year-to-date performance, developed ex-U.S. large-cap equities continue to trade at far more attractive valuations than their U.S. counterparts. Figure 1 shows that developed ex-U.S. large caps have a CAPE ratio of 18.7 compared to 33.9 for U.S. large caps. This wide valuation spread is striking not only in comparison to each other, but also in the context of their own historical valuations. U.S. large caps hover in the 96th percentile (nearly as expensive as they've ever been) while developed ex-U.S. equities quietly sit in the 40th percentile, modestly cheaper than their long-term median.

Looking Beyond the Recent Past

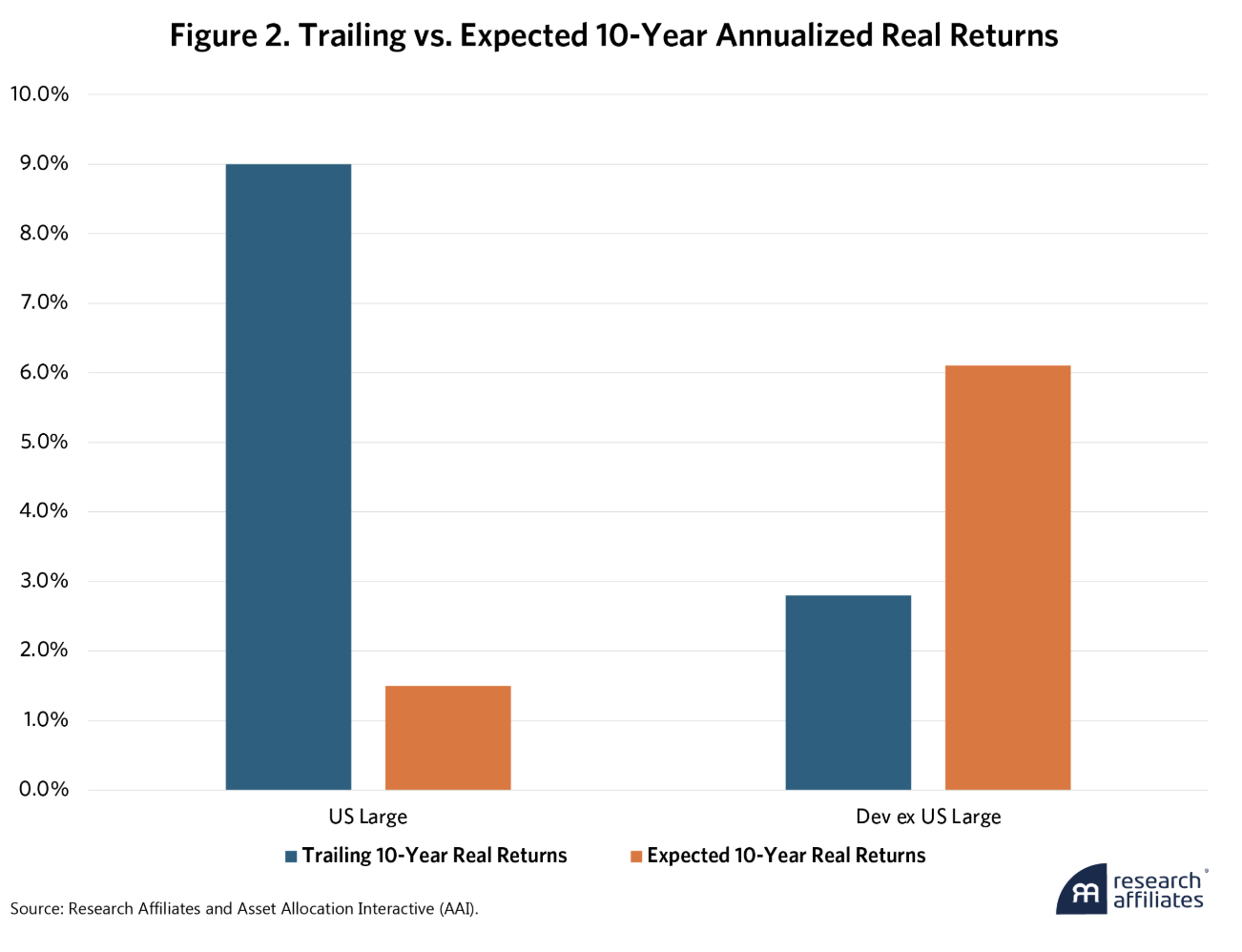

Investors might be tempted to dismiss non-U.S. developed markets based on their recent history. As Figure 2 shows, developed ex-U.S. large-cap equities delivered only a 2.8% annualized real return over the past 10 years, significantly trailing U.S. equities. But anchoring expectations to past performance can lead investors astray. History teaches us that today’s laggards are often tomorrow’s leaders, especially when supported by superior valuations.

Our capital market expectations suggest the pendulum is poised to swing. For comparison, Figure 2 also shows our 10-year forward looking expected returns. We anticipate developed ex-U.S. large caps to generate 6.1% annualized real returns, more than four times the 1.5% we project for U.S. large caps.

Valuation Compression vs. Expansion

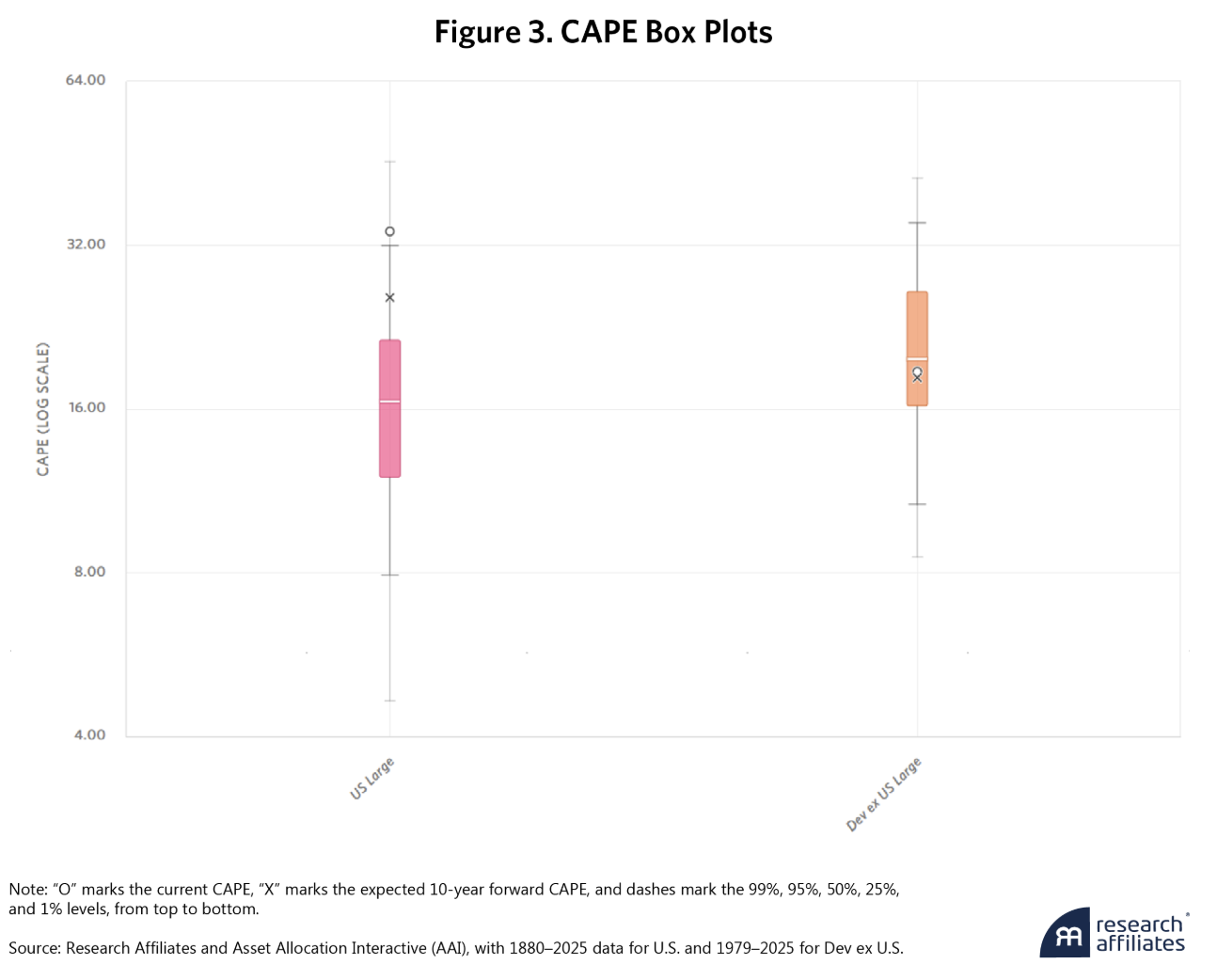

As detailed in Figure 3, our CAPE-based modeling anticipates valuation compression in the U.S. market, from a current CAPE of 33.9 down to an expected 25.7 over the next decade. In contrast, we foresee no meaningful compression (or expansion) in developed ex-U.S. markets. Importantly, developed ex-U.S. equities do not need expanding multiples to generate strong returns. With an expected 3.0% dividend yield and 2.8% real earnings per share growth, there is already a solid foundation for long-term performance.

Momentum is Also with Dev Ex-U.S.

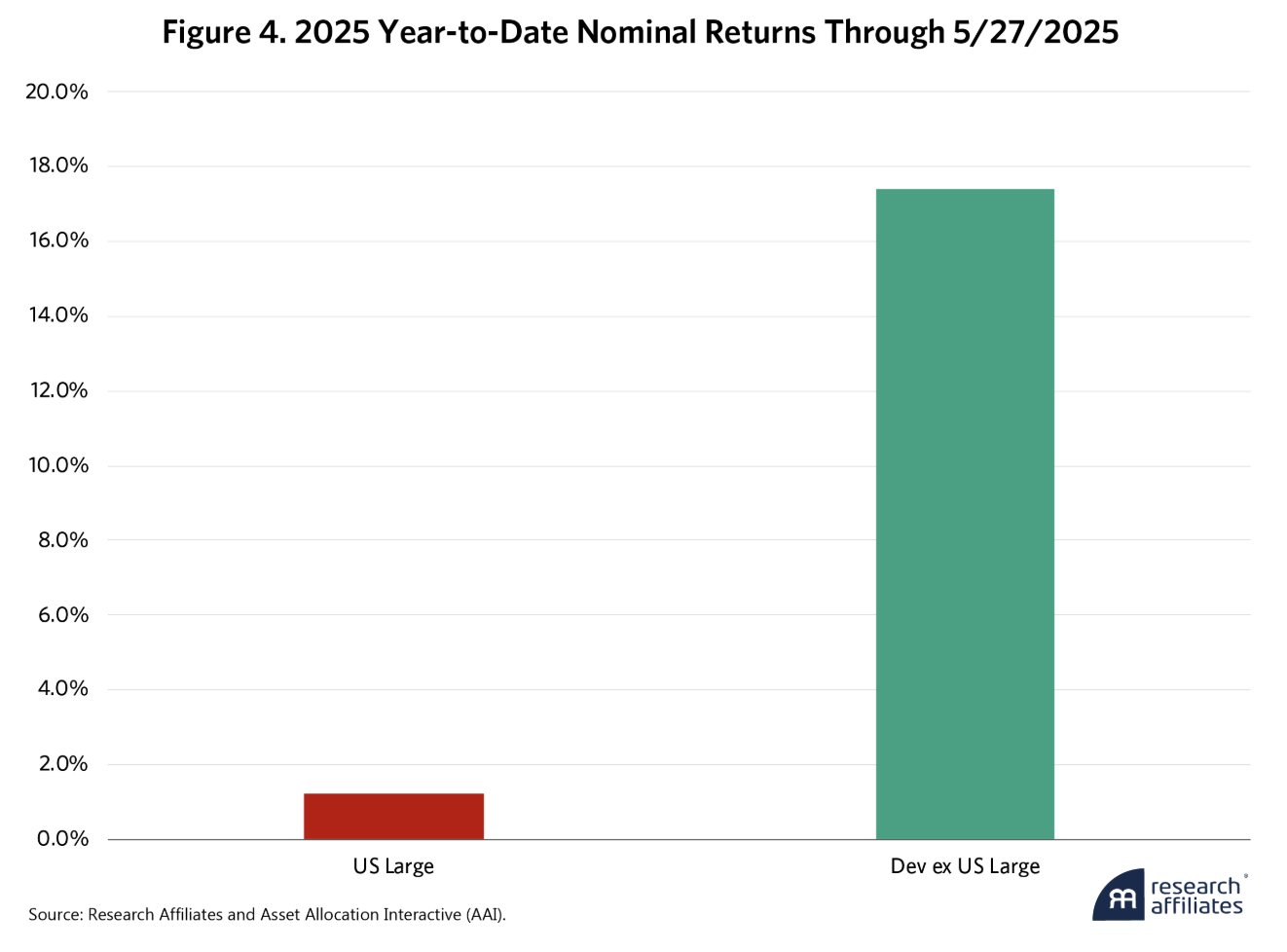

Dev ex-U.S. equities are no longer just attractive from a valuation standpoint. Recent price action indicates that momentum is now on their side as well. As shown in Figure 4, developed ex-U.S. large caps have posted double-digit nominal returns year-to-date, handily outperforming U.S. large caps, which have delivered negative returns through the end of April. More notably, in the trailing 12 months, developed ex-U.S. large caps have outperformed U.S. large caps by approximately 0.8% in nominal terms. Now that both valuation and momentum are aligned, this asset class looks increasingly attractive.

For investors anchored to U.S. benchmarks, now may be an opportune time to consider tilting allocations toward developed ex-U.S. markets. The combination of lower starting valuations and positive momentum suggests that developed ex-U.S. equities may offer a more attractive risk-return tradeoff than their U.S. counterparts. At Research Affiliates, our Asset Allocation Interactive (AAI) tool empowers investors to examine these dynamics and construct diversified portfolios aligned with long-term expected returns, not recent headlines.

Valuation remains one of the most reliable predictors of long-term performance. With developed ex-U.S. markets trading below historical norms and offering meaningful expected return premiums, we believe the case for global diversification is as strong today as it’s been in over a decade. We encourage investors and advisors to explore these insights further on our AAI platform, where a more data-driven approach to asset allocation awaits.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Research Affiliates

Read more commentaries by Research Affiliates