Policy uncertainty and mixed economic signals continue to upend financial markets, generating heightened volatility. While the uptick in volatility may unsettle some high-yield bond investors, we believe the sector provides continued opportunity—and that by focusing on shorter-maturity debt, investors may be able to reduce portfolio volatility without sacrificing income potential.

Higher Yields with Less Volatility: A Potent Mix

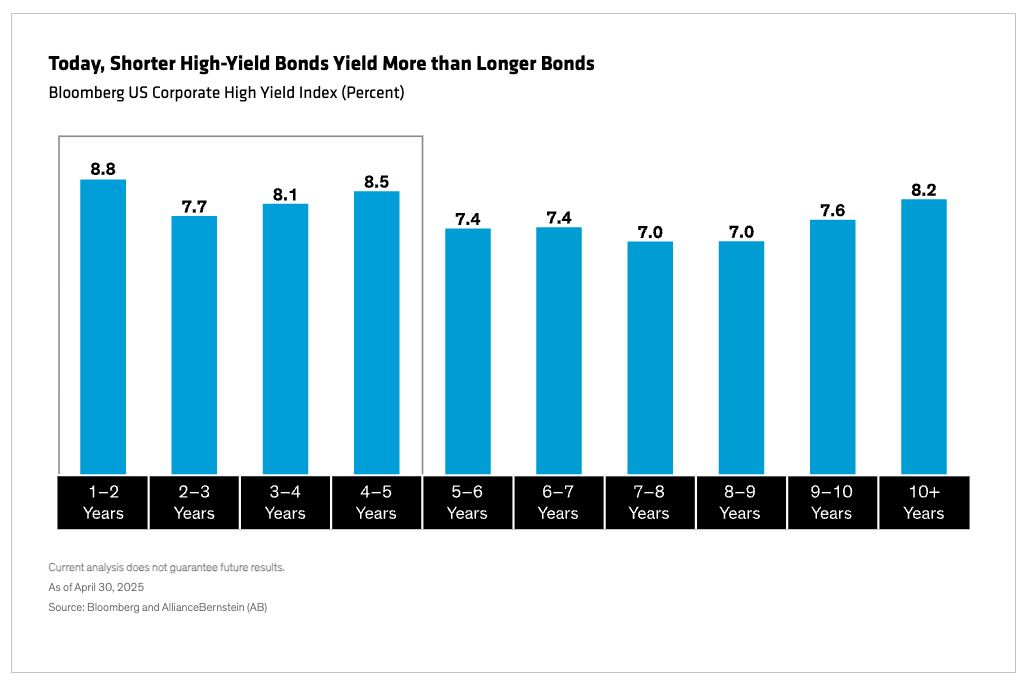

Even in normal times, a shorter-term high-yield strategy can provide high levels of income, albeit with shorter bonds yielding less than longer-dated bonds. Today, however, flatter Treasury and spread curves mean short-maturity high-yield bonds yield more than intermediate- and long-term bonds (Display). That’s a marked departure from historical norms.

What’s more, yields are broadly elevated compared to historical levels of the last decade and a half. Today, yield to worst—a reliable predictor of five-year forward returns—exceeds many 10-year equity return projections. Higher yields provide a buffer against market volatility, as we saw in April, when high-yield spreads widened by roughly 60% owing to tariff concerns, but the sector nevertheless outperformed the equity market.

Short-maturity high-yield bonds also come with a more attractive risk profile than longer-term high-yield bonds, due to their lower sensitivity to changes in spread levels. Investors also have better visibility into near-term financial risks, allowing them to more easily avoid short-term bonds that might default. Typically, you’d expect to sacrifice yield in exchange for those advantages. But right now, investors in short high-yield bonds are being paid more to assume less risk.

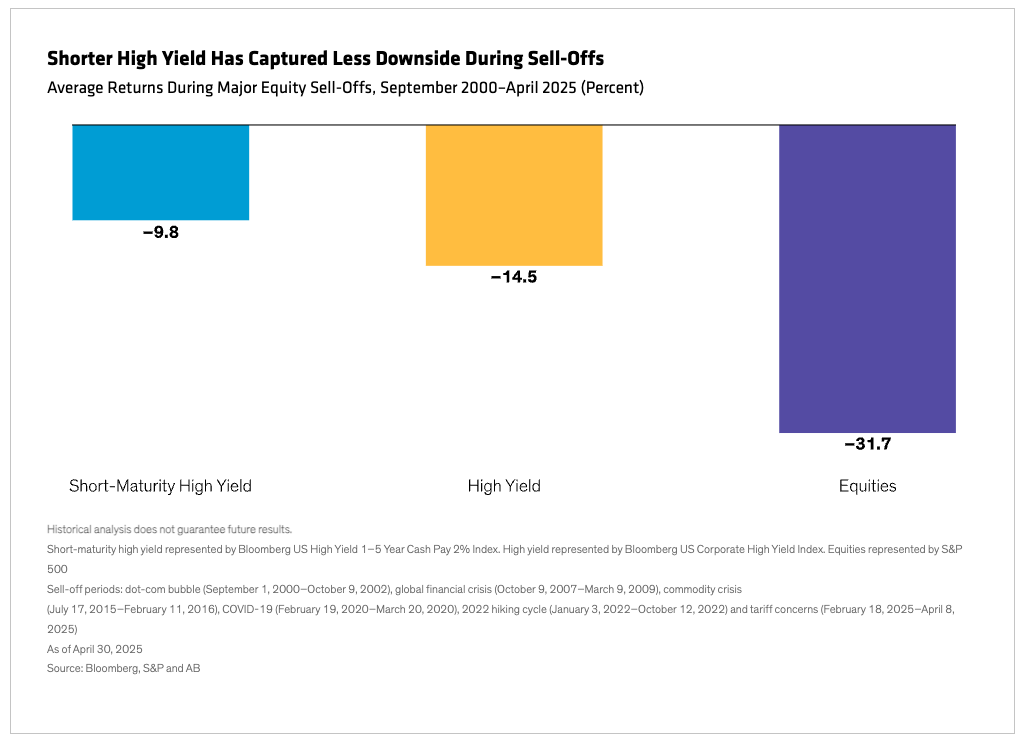

Short Maturity Captures Less Downside

Short-maturity high-yield bonds can really show their mettle during periods of market volatility. During past equity market corrections, short-term high yield captured around three-fourths of traditional high yield’s drawdown, on average, and less than half the drawdown of equities (Display).

Our analysis also suggests that short-maturity high-yield bonds capture most of the broader high-yield market’s upside in risk-on environments, pointing to better potential risk-adjusted outcomes over full market cycles.

Credit Selection Matters

Of course, investors still need to be judicious about how they deploy capital, as heightened volatility can create dispersion among credit issuers. Tariffs may benefit some firms but handicap others, and slowing growth is particularly problematic for cyclicals and CCC-rated bonds—underscoring the importance of active management.

Currently, we see the best opportunities in non-cyclicals and high-yield credits rated B and above. In our view, these are better insulated from economic shocks than CCC-rated issues, which carry meaningfully higher default risk. In fact, historically, a portfolio of short-maturity BB and B-rated bonds has exhibited lower volatility than investment-grade BBB bonds.

For all these reasons, we believe that short-maturity high yield presents a timely opportunity for investors to stem volatility while capturing attractive income potential.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein