Key takeaways

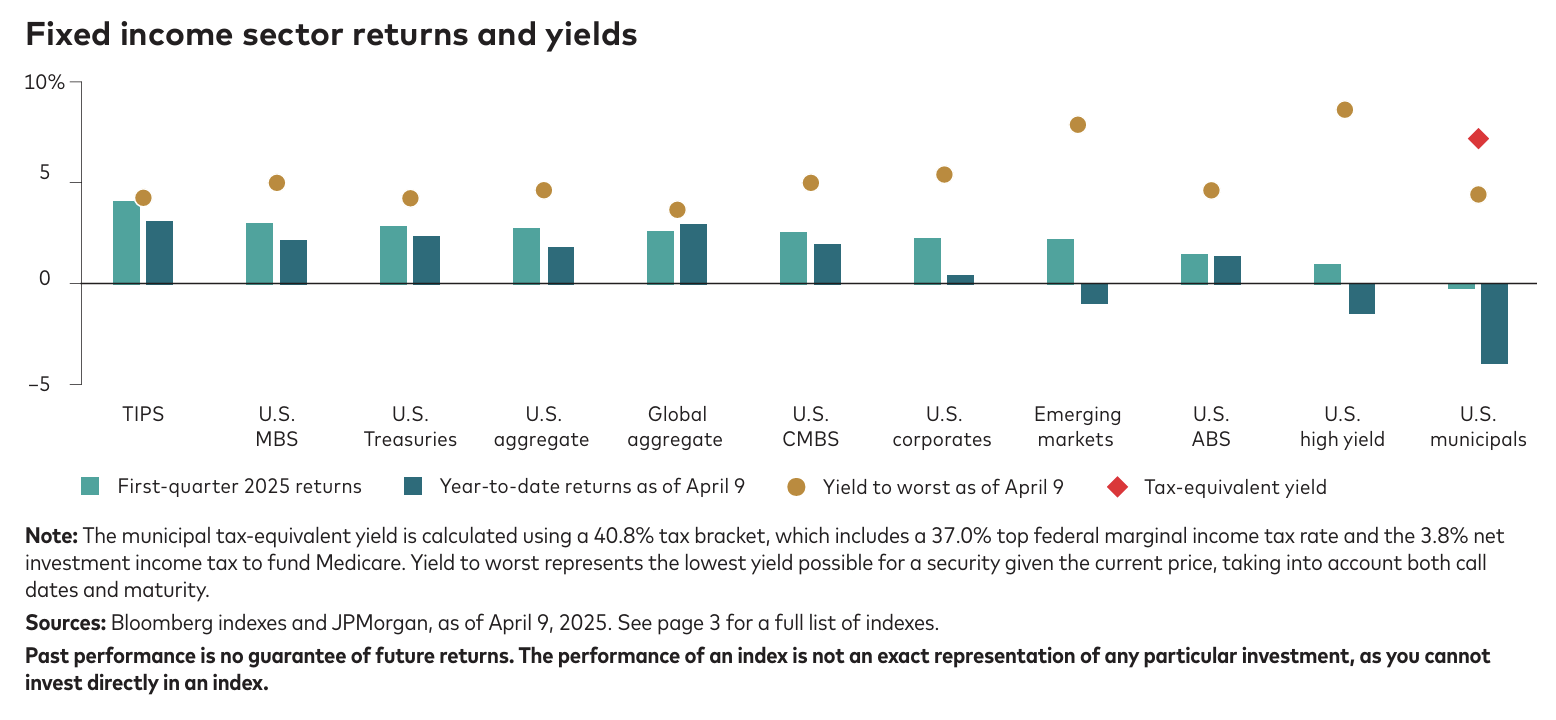

Performance recap

Higher-quality bonds have outperformed so far this year as Treasury yields broadly declined and credit spreads widened. Tariff policy vacillation and weaker consumer sentiment data sparked fears of an economic growth slowdown. Positive bond returns helped cushion the volatility in U.S. stocks.

The big picture

The implementation of higher-than-expected tariffs in the U.S. will have substantial economic impact if maintained. Consequently, we revised our growth and labor market forecasts down and increased our outlook for inflation. While the likelihood of a recession has risen, the underlying economic fundamentals still show signs of strength. Inflation pressures could limit the Federal Reserve’s policy options.

Our approach

Before the tariff announcements, we trimmed credit risk and moved up in quality. We remain optimistic on interest rates, favoring intermediate maturities as a hedge against our credit exposure. Credit valuations have improved, but not sufficiently to offset the increased uncertainty. We are overweight sectors that are more resilient to growth and policy risks. In municipal bonds, we anticipate strong flows into the summer months and see significant value in high-quality bonds at the long end of the curve.

A tidal shift

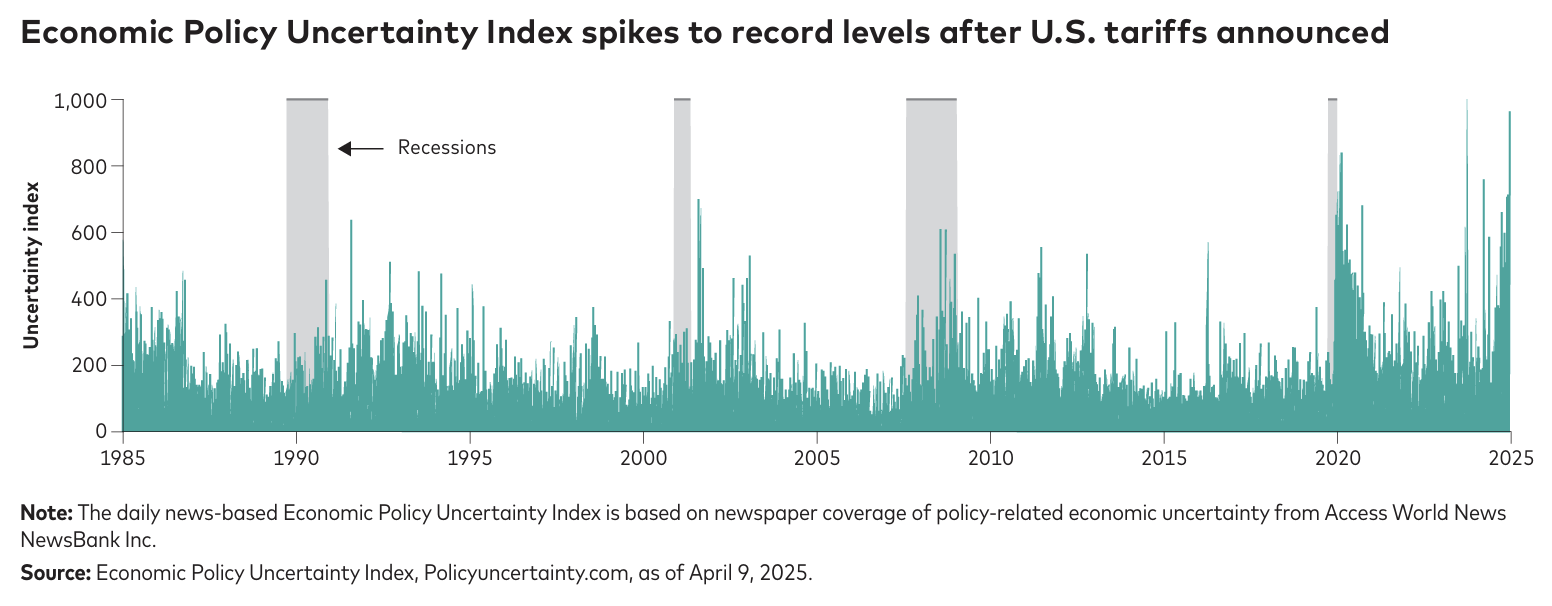

There is a tidal shift ongoing in the global economy. The Trump administration surprised the market with a broad new round of tariffs on April 2 before declaring a pause for many partners a week later. Uncertainty remains about where negotiations will go, which tariffs will ultimately be implemented, and how long they will last. These and other questions, such as the burgeoning federal debt levels, are complex, structural issues that will not be resolved quickly.

The far-reaching economic implications have led us to reassess our 2025 outlook. We believe this stagflationary impact will dampen growth and help hold inflation higher in coming months. The rising risk of a recession keeps us optimistic on interest rates and defensive on credit for now. We are navigating increasingly uncertain waters, where the global economic tidal transition has taken on a more unsettled tone.

In recent weeks, U.S. fixed income has seen credit spreads widen to their highest levels since the onset of the COVID-19 pandemic in March 2020, and before that, the 2008 global financial crisis. Treasury rates were volatile, sharply declining at the end of the quarter due to recession fears, which triggered a flight to quality. They then retraced, especially on the long end of the yield curve, where technical factors exacerbated price movements.

From risks to realities

We expect higher market volatility to continue. The economic and policy focus has shifted from assessing potential risks to managing realities. Soft sentiment indicators will soon give way to hard results on inflation, trade balances, employment, wages, and earnings. In the meantime, businesses will reassess their costs and plans, even as governments weigh their options.

Monetary policy is also at the center of attention. We anticipate that the Fed will be reluctant to reduce rates until it has greater clarity around the near- and medium-term impacts from higher tariffs. If the labor market weakens materially and recession concerns rise, we think the Fed can and will support the economy as necessary, provided long-term inflation expectations are stable.

Investors will need the durability that comes through diversification. We believe bonds remain well positioned to offer attractive income and higher returns if downside risks increase. We have put our global capabilities to use in identifying opportunities, and we think investors will find that fixed income diversification will help their portfolios retain buoyancy in these swirling seas.

U.S. economy and policy

While recent U.S. economic activity remains firm, questions remain regarding when and to what degree recent negative signs in soft data points— the so-called “vibecession”—will flow through to hard data such as retail sales, employment, and growth over the coming months.

In recent years, the correlation between soft and hard data has been weak. However, given the magnitude of the recent tariff announcements, not to mention fiscal cost cutting, we anticipate broader economic weakness in the months ahead. Persistent uncertainty will act as a tax on the economy, further restraining corporate and household spending.

An evolving outlook

Our central case scenario for the U.S. entering 2025 called for continued strong growth, with inflation stuck in the mid-2% range. We acknowledged more possibilities due to expected policy changes and highlighted several prospects beyond our base case.

We’ve updated our outlook due to the broaderranging tariff policy and added friction from higher levels of business and household uncertainty. A stagflationary-impact scenario is now our base case forecast.

Weaker growth, higher inflation

Our revised outlook for the U.S. accounts for the effective tariff rate to settle above 15%, which represents a substantial increase in the aggregate rate compared to 2024. Even with the pause in reciprocal tariffs, we maintain the following forecasts:

• Gross domestic product (GDP): U.S. 2025 GDP growth below 1%.

• Inflation: Year-end 2025 core inflation (as measured by the Personal Consumption Expenditures price index) increasing by more than a percentage point to nearly 4% year over year.

• Labor: The unemployment rate rising by more than half a percentage point to around 5%.

Higher inflation will challenge the Fed. We anticipate the Fed will be on hold in the near term, but that its year-end 2025 target for the federal funds rate will fall to a range of 3.25%4% as it seeks to support a slowing economy.

• On inflation: The Fed will assess any tariffrelated price increases and determine what can be looked through as a transitory price increase and what may have medium-term effects. This will guide how much the Federal Open Market Committee needs to lean into the inflation side of its mandate and how long policy rates remain restrictive. For the Fed to ease policy, it needs to be confident that medium-term inflation expectations remain anchored at levels consistent with a 2% rate.

• On employment: The labor market is currently balanced, with 1.1 job openings for every job seeker. The hiring slowdown so far primarily reflects a reduction in job openings, which has had a muted effect on the unemployment rate. Additional softening in labor demand will have a bigger impact.

While the probability of a 2025 recession has increased, it is not our base case. However, if that were to occur, we expect that the Fed would meaningfully cut interest rates to support the economy.

Click here to read more

This article was previously published on vanguard.com

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Vanguard

Read more commentaries by Vanguard