Gridlock

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsPrivate equity transaction volumes remain limited despite predictions for a boom in 2025. With interest rates remaining elevated and the economic backdrop increasingly uncertain, executing acquisitions and IPOs is proving a challenge, leading financial sponsors to hold portfolio companies for longer. This impasse has significant ramifications, not least for credit markets. The lack of fresh deals leads to an absence of new supply for the leveraged credit markets that generally provide funding for M&A and LBOs. Meanwhile, elevated yields have increased investor demand for credit, creating the supportive supply/demand dynamic that helps constrain spread widening. Even with the recent volatility relating to fluctuating global trade policy, that’s what we’ve seen in credit: relatively limited defaults, unremarkable spreads, but compelling coupon income.

An Absence of Deals

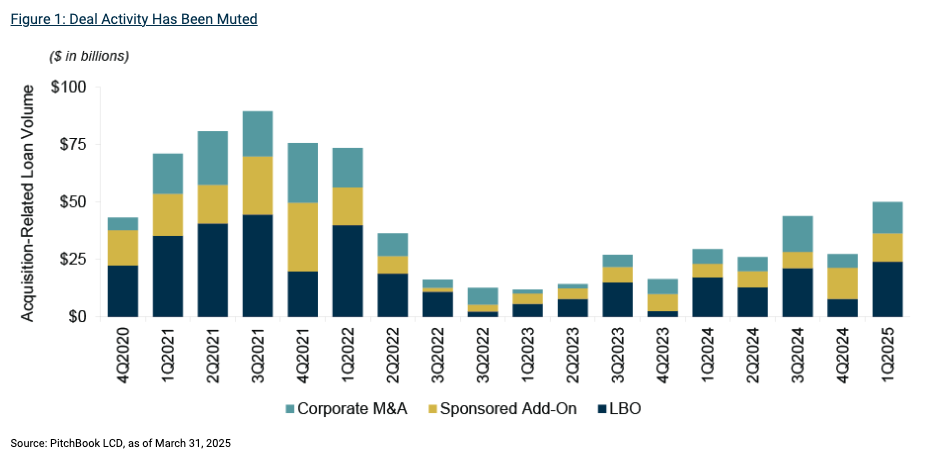

It’s no secret that M&A and LBO activity has struggled to recapture the heady days of 2021 when low interest rates and a flood of liquidity supported record deal levels – and the accompanying debt issuance. The post-pandemic deal boom came to a screeching halt in 2022 as central banks raised rates in an attempt to curtail rampant inflation. Private equity funds have since struggled to exit portfolio companies at their desired valuations and new deals have dwindled. Though we’ve seen some signs of recovery, predictions for a resurgence in 2025 appear to have been overly ambitious. (See Figure 1.)

All Roads Lead to Rates

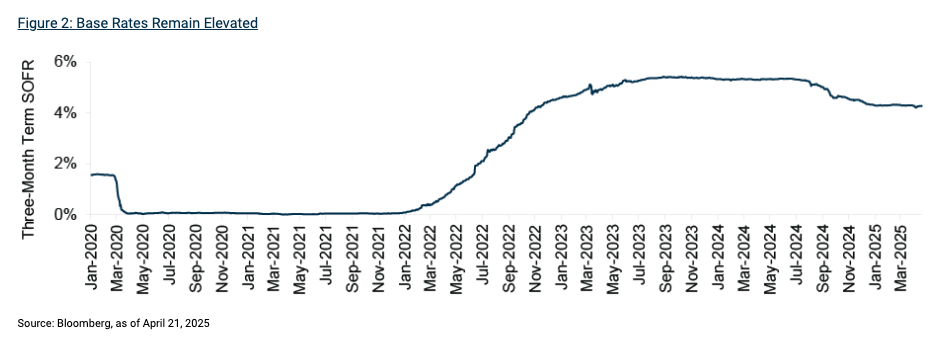

In 2022-23, an increase of over 500 bps in the fed funds rate marked an end to the era of ultra-cheap leverage that commenced in the aftermath of the Global Financial Crisis. Private equity sponsors accustomed to getting seven turns of leverage for buyouts and paying a 4% coupon on their loans soon faced a new environment where that leverage level was largely unrealistic and their interest costs had doubled.1 While the rapid rate increases were designed to halt very apparent inflation, market participants have been caught off guard by how long it would take for rates to moderate again, with SOFR still well above 4%. (See Figure 2.) What’s caused this prolonged elevation? Chiefly, the surprising strength of the U.S. economy, led by a strong consumer benefitting in many cases from mortgage rates locked in at record-low levels. Rather than the anticipated economic slowdown as interest rates rose, strong jobs data and ongoing price increases have made it challenging for the U.S. Federal Reserve to make meaningful rate cuts. Whereas the Fed had latitude to become more accommodative during the Covid-19 crisis, now that prices of consumer goods have already risen significantly over the last few years, any policy change that fuels inflation may cause further struggle for lower/middle-income consumers.

Capital Cost Mismatch

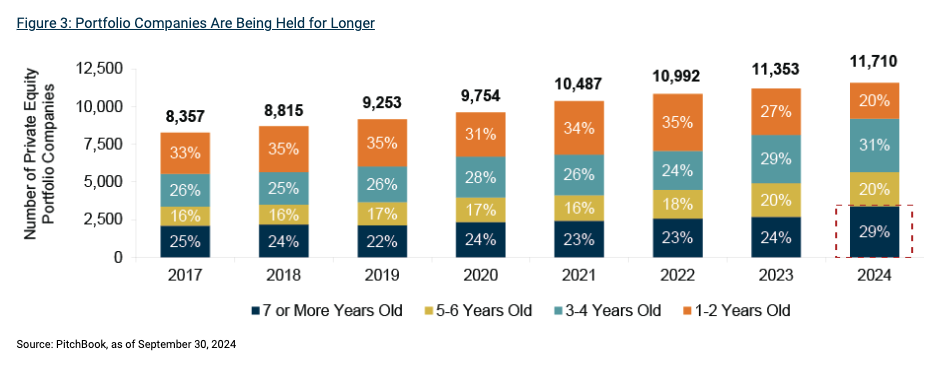

Crucially, higher interest rates impact the salability of private equity portfolio companies. With a drastically higher discount rate than that between 2009-21, the valuations portfolio managers believe their holdings are worth have been challenged: potential sellers refuse to compromise while potential buyers aren’t eager to increase their bid. Because of this deadlock, hold periods have increased, with almost 30% of portfolio companies in 2024 having been held for over seven years. (See Figure 3.)

What’s led to this impasse? Prospective sellers purchased companies at a much lower cost of capital than potential buyers now face to fund purchases of the same assets, leading to a mismatch. Notably, over 60% of buyout deal returns in the low-interest-rate era were attributable to broad market multiple expansion and leverage.2 With these levers challenged, a private equity manager may need to sell to a buyer with a lower cost of funding to achieve their desired exit multiple: a situation that might not be forthcoming. Private equity managers can’t get the exits they want and could face a renewed lack of buyers as uncertainty over trade policy pushes potential buyers to the sidelines.

Seeking Distributions

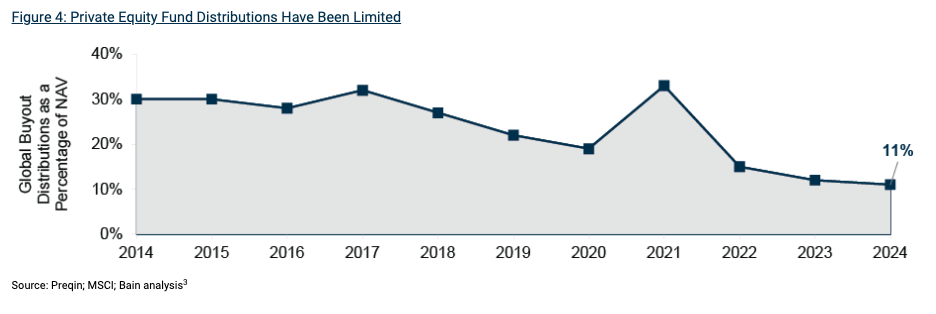

As hold periods increase, private equity LPs are left waiting for distributions: in 2024, distributions from buyouts funds dropped to just 11% of fund NAV, down from around 30% in 2021. (See Figure 4.) As pressure mounts to improve DPI (a measure of distributions from a fund), private equity managers are seeking creative ways to return capital to LPs without selling assets at undesirable valuations. This includes a variety of fund financing methods, perhaps most prominently NAV financing. NAV loans allow sponsors to borrow money against the value of their fund portfolio, with this capital generally used to fund value-creation initiatives at portfolio companies and to make distributions to investors. Continuation vehicles have also soared in prominence, providing a way for GPs to retain promising assets after the end of a fund’s life, with existing LPs given the opportunity to sell their share. These methods of liquidity generation may provide LPs with the capital to invest in new buyout funds (and thus support transaction activity) but may do little to ease the backlog of private equity portfolio companies.

Lenders Await Supply…

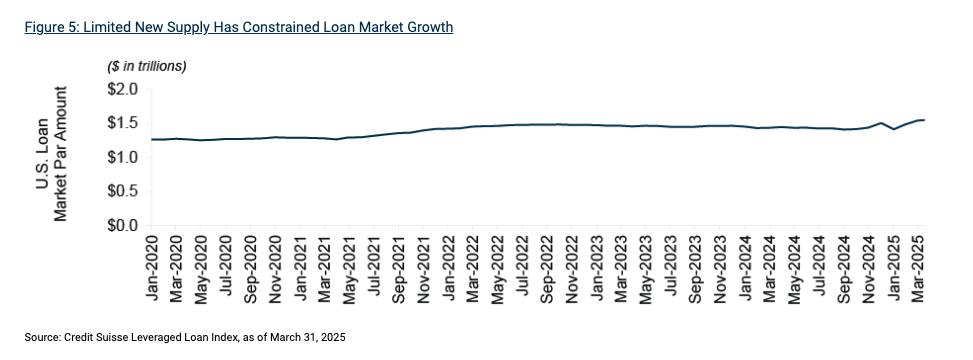

With hold periods increasing for portfolio companies, the leveraged credit markets have mostly seen supply in the form of refinancings, rather than debt issued to fund acquisitions: refinancings have constituted over 85% of supply in the loan market so far this year.4 Transactions that effectively just extend the maturities of existing debt don’t directly increase market size, leaving investors fighting over the same amount of paper. In the three years ending in March 2025, the U.S. loan market grew by a total of just 6.1%.5 (See Figure 5.) Meanwhile, the prospect of high single-digit coupons has enticed income-seeking investors.

…While Investors Demand Credit

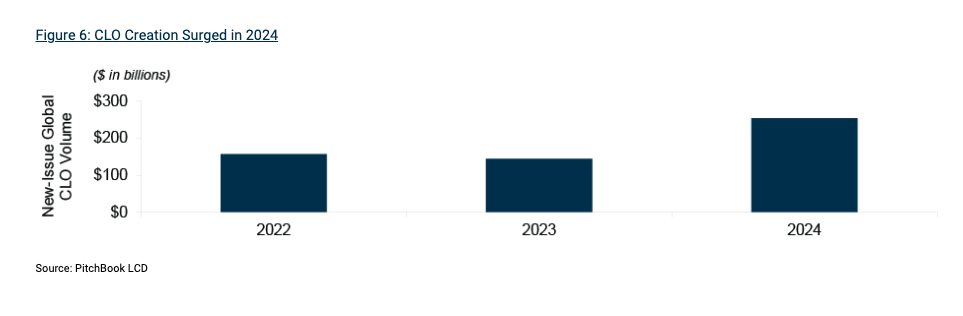

While supply has been limited, demand for credit has been strong; for exactly the same reason! After being stuck with mediocre yields for over a decade, credit investors have jumped at the chance to buy high yield bonds and senior loans at a roughly 8% yield, and, of course, an even greater yield in private credit.6 Demand for high yield bond and senior loan mutual funds was strong in 2024 while particularly remarkable has been the record levels of CLO creation, which has turbocharged demand for senior loans. (See Figure 6.) Though high yield bonds lack a structural buyer akin to CLOs, the limited growth in this market – exacerbated by issuers leaving the market upon achieving an investment grade rating – means the supply/demand balance is also tilted toward demand. Recent market volatility may briefly take the edge off the demand for credit, as shorter-term capital pulls back, but elevated credit yields are likely to be a persistent tailwind for credit demand.

Technical Support

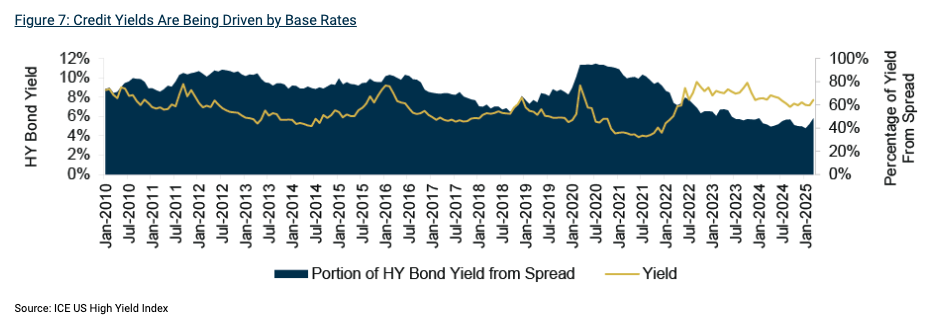

When supply is low but demand and rates are high, we have the situation we’ve been experiencing over the last few years: unexciting credit spreads but attractive yields. Even with the recent increase in spreads, over half of the yield on high yield bonds is currently coming from rates compared to only 25% on average since 2010. (See Figure 7.) Happily for investors, elevated rates are bumping the yield on high yield bonds to around 100 bps above the average level since 2010.7

Uncertainty Redux

Adding to the complex backdrop, markets were roiled in April by seismic shifts in global trade policy. An already-limited M&A market immediately paused: it’s extremely difficult to underwrite new deals when economic conditions are entirely uncertain and debt costs are rapidly fluctuating. Even prior to the tariff announcement on April 2, we’d seen the lowest number of M&A transactions in over a decade, with this deal impasse constraining supply in the leveraged credit markets.8 As managers wait for new deals, a prudent approach may be to avoid compromising on underwriting standards in grasping for limited supply, while also cautiously accessing dislocation in the secondary market as it presents itself. Trade policy is a new variable for investors to contend with, but as Howard Marks recently reminded us ‘‘there’s no such thing as foreknowledge here, just complexity and uncertainty, and we must accept that as true.’’

Credit Markets: Key Trends, Risks, and Opportunities to Monitor in 2Q2025

(1) The Backdrop Is Even More Uncertain than Usual

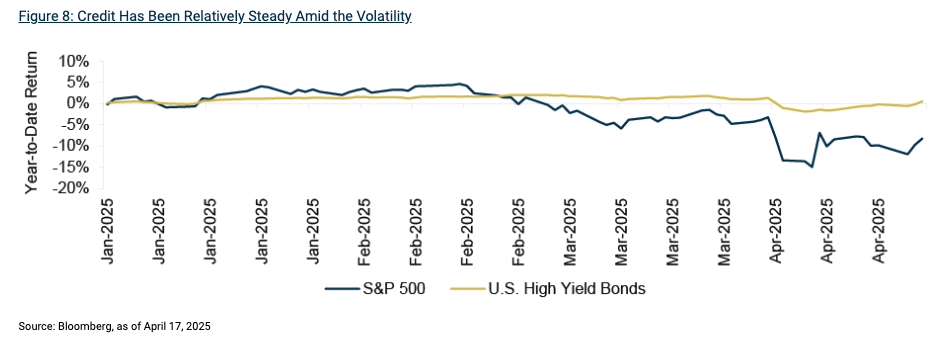

Volatility and uncertainty stemming from President Trump’s tariff announcements have taken market participants on a roller-coaster-like journey. Equity markets experienced some of their biggest moves in decades, with the S&P 500 dropping by over 10% in the two days after the initial tariff announcement. Credit hasn’t been immune to the recent volatility but has done its job and held in well versus equities: it’s in these uncertain times that investors can take particular comfort in the fact that credit returns are contractual – based on company survival rather than business excellence. (See Figure 8.)

Looking ahead however, tariffs – or simply the uncertainty surrounding their implementation – could have a significant effect on credit markets, creating both risks and opportunities. Though President Trump appears to have softened his tariff measures, the overall tariff rate remains considerably above its 2024 level. And crucially, this episode has left the policy environment more challenging, geopolitical tensions – between the U.S. and China especially – appear elevated, and market participants lack clarity on the direction of fiscal and monetary policy.

The future is always uncertain but even more so now. What will happen when the current pause on tariff implementation elapses? How will negotiations between the U.S. and China progress? Will equity markets recover their lost ground in the coming weeks – or fall even further? Will Fed policy change? We don’t know, nor do we believe anyone does.

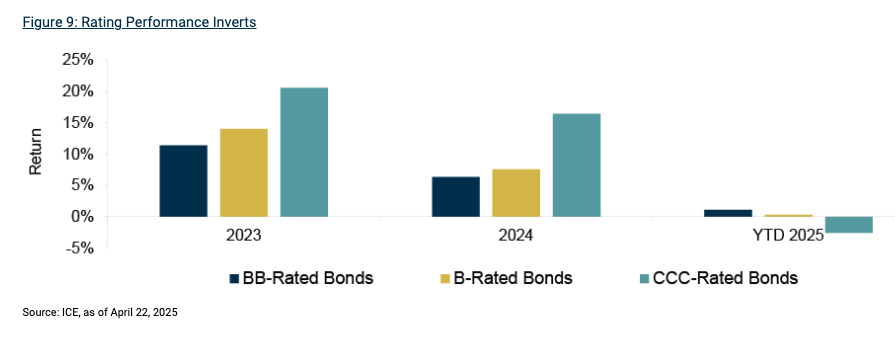

(2) The Market’s Riskiest Names Feel the Volatility

After the significant drawdown in 2022, the highest-risk credits have consistently outperformed.9 As fears of a hard landing dissipated, buyers of CCC-rated bonds have generally enjoyed healthy price appreciation. (See Figure 9.) However, the recent bout of volatility led to a repricing of risk: CCC-rated bonds were trading within a 700-bps spread in February but blew out to 1,100 bps at the start of April.10 CCCs had led the market for two years but a shift in the economic outlook left many of the weaker names undesirable.

Though it’s worth noting that CCCs don’t make up a significant portion of the high yield market: indeed, over half the market is rated BB, which helps the market remain resilient amid the volatility.11

(3) A Change of Course in Europe

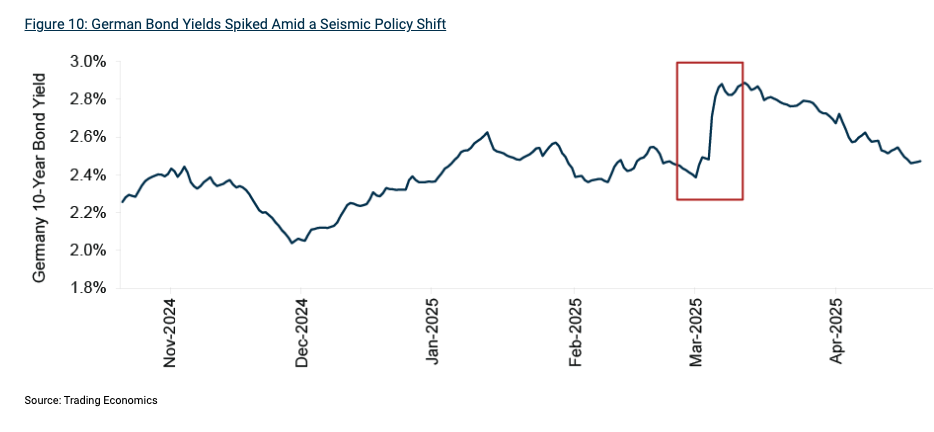

European equities lagged the U.S. by significant margins in 2023 and 2024, with that relationship inverting so far in 2025.12 While the S&P 500 remains negative year-to-date, the STOXX Europe 600 is marginally positive, with German equities a notable bright spot.13 Germany’s reform of its debt brake was particularly notable, paving the way for a historic increase in defense and infrastructure spending.

Accordingly, the yield on the ten-year German Bund increased by 30 bps in one day, the largest single-day increase in decades. (See Figure 10.) This then unwound as investors bought up German bonds amid the tariff tumult in the U.S., seeing the Bund as an alternative haven amid volatility. Away from sovereign bonds, investors in European corporate bonds must assess the benefits and risks to their holdings from a potential new economic paradigm, including increasing government spending, the impact of potential tariffs, and ongoing geopolitical volatility.

Assessing Relative Value

Strategy Focus

High Yield Bonds

Market Conditions: 1Q2025

U.S. High Yield Bonds – Return: 0.9%15 | LTM Default Rate: 1.2%16

- Within the various rating tiers, BB-rated bonds were the top performers: BB-rated bonds generated a solid return of 1.5% during the period. On the other hand, CCC-rated bonds were the worst performers, recording a -0.7% return in the quarter. B-rated bonds returned 0.7%.

- High yield bond issuance was steady during the first quarter: Issuance totaled $68bn in the period. With M&A activity still slow, refinancings dominated the new issue landscape.

European High Yield Bonds – Return: 0.9%17 | LTM Default Rate: 1.5%18

- Spreads widened during the first three months of the year: At the end of the first quarter, spreads increased to the middle of the historically normal range of 300–500 bps. Yields in the market also remain elevated.

- Overall quality in the high yield bond market remains strong: BB-rated bonds make up roughly 60% of the European high yield bond market, and B-rated bonds make up roughly 30%.

Opportunities

- High yield bonds continue to be priced at a discount to par: Investors can potentially earn capital appreciation and high coupon income.

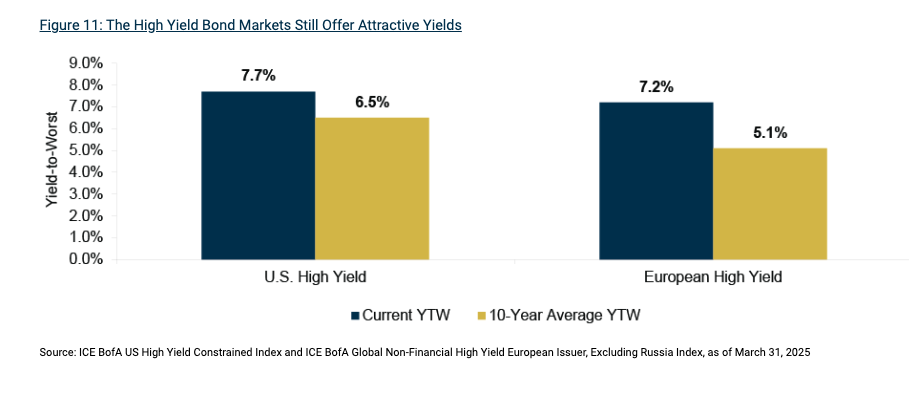

- Attractive yields are still on offer in the high yield bond market: Elevated yields continue to give investors the opportunity to earn attractive contractual returns. (See Figure 11.)

- Issuers’ fundamentals remain robust: Interest coverage is comfortably above the historical average. With less than 10% of the high yield bond market set to mature by 2027, the risk of near-term defaults is limited.

Risks

- Elevated inflation and high labor costs may impair issuers’ fundamentals: Input costs remain high even though inflation has slowed.

- Heightened geopolitical risk may put pressure on economic growth: Geopolitical tensions and uncertainty around global trade policy may lead to increased volatility.

Senior Loans

Market Conditions: 1Q2025

U.S. Senior Loans – Return: 0.6%19 | LTM Default Rate: 1.2%

- U.S. senior loans recorded a positive return in 1Q2025: The asset class experienced positive returns in January and February but wasn’t immune to the tariff-related volatility, which caused performance to decline in March, marking the first monthly loss since October 2023.

- Gross issuance remained robust: Activity in the loan primary market was healthy in 1Q2025, totaling $337bn. However, refinancings/repricings continued to dominate issuance. We entered 2025 expecting a rise in M&A activity and new money issuance due to anticipated regulatory leniency under the Trump Administration, lower borrowing rates, and significant private equity dry powder. Although we saw an uptick in new money deals through the end of March, issuance fell short of expectations due to market volatility caused by uncertainty regarding global trade policy.

European Senior Loans – Return: 1.0%20 | LTM Default Rate: 0.6%

- European loans generated a positive return during the quarter: Strong coupon income continued to drive returns, and helped mitigate spread widening over the period.

- New issuance was robust in 1Q2025: The European market recorded €42bn of newly issued debt in the first quarter, with refinancings/repricings continuing to dominate.

Opportunities

- The financial health of many loan issuers has improved: Many primary loan deals done in the last two years were created with capital structures capable of managing leverage in a higher-rate environment. This – coupled with company-specific cost-cutting measures in recent years – has resulted in more financial stability among loan issuers today compared to 2021-2022.

- Market volatility may present buying opportunities: Market fluctuations can lead to mispricings, creating an opportunity to acquire high-quality bank loans at significantly discounted prices.

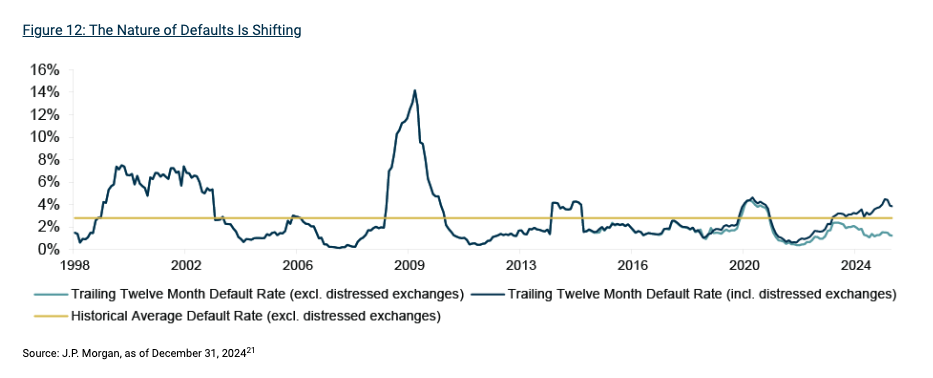

- Loan managers within large, diverse credit-focused organizations are well-positioned: Defaults in the loan market have shifted from predominantly bankruptcies to distressed exchanges. (See Figure 12.)

Risks

- Fluctuations in U.S. foreign trade policy have introduced a high degree of uncertainty into global markets: Weaker companies without the pricing power to pass through cost increases to consumers may struggle.

Investment Grade Credit

Market Conditions: 1Q2025

Return: 2.4%22

- Investment grade corporate bonds performed well in the first quarter: Interest rates across the U.S. Treasury curve declined during the period while credit spreads widened in response to growing fears surrounding global trade tensions.

- Higher-quality credit outperformed in 1Q2025: AAA-rated corporate bonds, which also tend to be the longest duration bonds, outperformed the lowest-rated segment of the investment grade market by over 30 bps in the first quarter.23

- Issuance was extremely robust during the period: Gross issuance of investment grade bonds totaled $556bn in the first three months of the year, surpassing the $544bn issued in 1Q2024 to become the largest first quarter on record. Investor demand for investment grade credit persists within the primary market despite some macro volatility, with an average oversubscription rate of 3.5x.25

Opportunities

- High-quality bonds offer the potential to insulate portfolios in a volatile environment: With a higher average credit rating and longer duration than high yield bonds, investment grade credit serves as an attractive diversifier and potential source of resiliency in risk-averse markets.

- Short-duration, investment grade credit could help investors navigate interest rate and credit volatility: High-quality, short-maturity bonds may outperform longer dated assets in an uncertain interest rate environment.

-

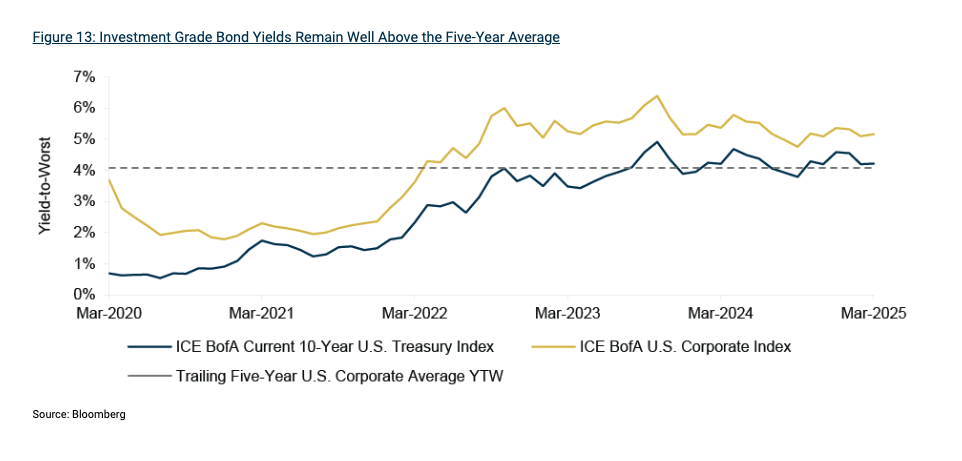

Investment grade bond yields remain elevated: High-quality corporate debt yields ended the quarter at 5.2%, meaningfully exceeding the five-year average of 4.1%. (See Figure 13.)

Risks

- If interest rates don’t decline as much as currently anticipated, fixed-rate asset classes may struggle: Concerns surrounding trade and immigration policies and, ultimately, inflation could lead the Fed to take a patient approach to cutting interest rates or delay a “Fed put” in a recessionary scenario.

- Investment grade credit could face competition from ultra-short duration assets: While the U.S. Treasury curve is no longer inverted – as measured by the difference in the ten- and two-year yields – money market funds and bills with one-year or less remaining offer yields near or above the ten-year Treasury rate. Historically, investors looking to minimize volatility utilize these assets, however they may find market yields less attractive once those holdings mature.

Emerging Markets Debt

Market Conditions: 1Q2025

EM Corporate High Yield Bonds – Return: 2.3%26

- EM corporate high yield bonds were stable in the quarter: Shortly after quarter-end, EM bond price volatility emerged upon the escalation of U.S. tariff measures and concerns about global growth, stagflation, and lower commodity prices.

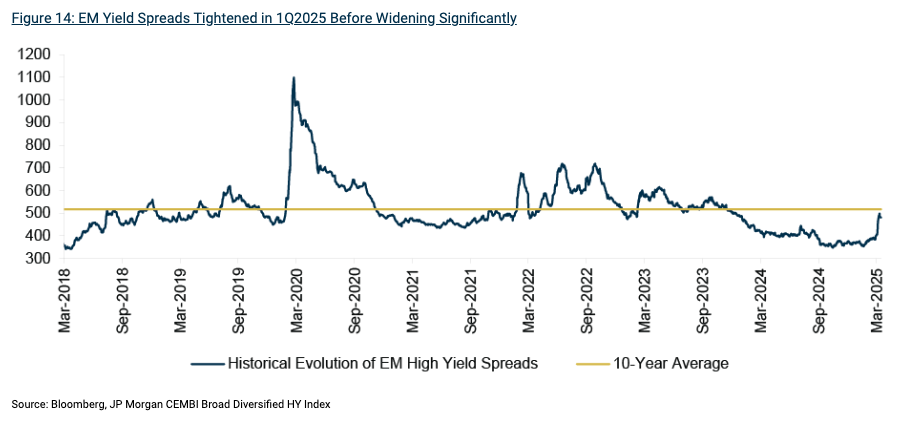

- EM bond issuance remained robust amid low bond yield spreads: EM high yield issuance was 30% higher than in the first quarter of 2024. Companies benefitted from EM bond yield spreads approaching seven-year lows. After quarter-end, yield spreads widened toward their historical average. (See Figure 14.)

- EM markets had a resilient start to 2025: EM equities outperformed U.S. equities, Latin America benefitted from currency appreciation and expectations of continued trade and policy alignment with the U.S., China targeted another stimulus-driven year of 5% growth, and financial conditions were sanguine in the first quarter of 2025. However, these trends moderated amid economic uncertainty relating to U.S. trade policy and the adverse impact of lower oil prices on many EM segments.

Opportunities

- Volatility can cause high-quality companies to be mispriced: Price volatility sparked by shifts in global investor sentiment could lead to indiscriminate selling activity and an exodus of short-term-oriented investors. Companies that have first-quartile cost positions in their industry and ample balance sheet runway may become available at attractive prices.

Risks

- A slowdown in global trade may put pressure on EM export-driven economies: Global trade conflicts could impact large EM economies and reroute trade flows, reshaping global trade dynamics. Direct targets of tariffs, such as Chinese and Vietnamese exporters and the global auto sector, may face outsized impacts.

Global Convertibles

Market Conditions: 1Q2025

Return: 1.4%27 | LTM Default Rate: 2.9%28

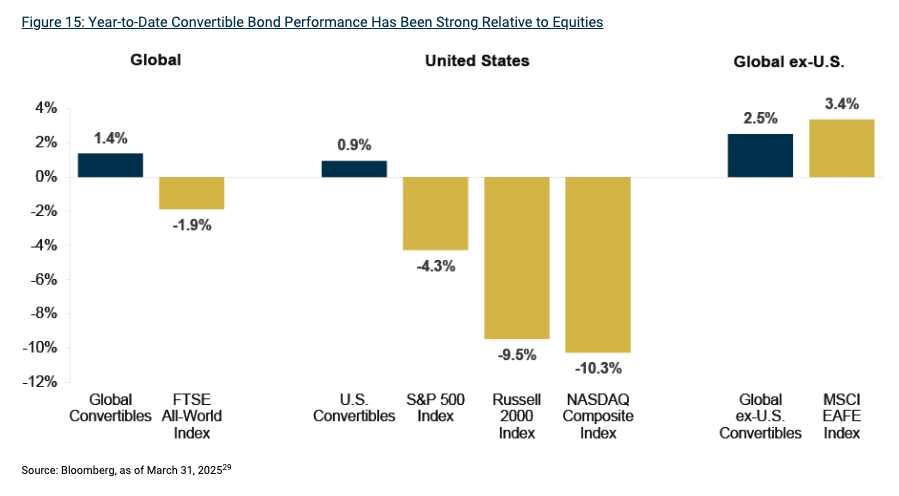

- Convertible bond prices increased in the first quarter, despite weak equity market performance: Risk assets fluctuated against a backdrop of mixed economic data, declining consumer confidence, and tensions surrounding global trade. President Trump, who formally took office in January, proposed a variety of tariffs (with a formal announcement – and subsequent iteration – coming after the end of the quarter). In response to the uncertainty, global equities declined, with the FTSE All-World Total Return Index ending the quarter down by 1.9%. Amid this heightened volatility, convertible bonds continued providing downside protection and generated a gain of 1.4% during the period. (See Figure 15.)

- Primary market activity remained healthy in 1Q2025: New issuance of global convertibles totaled $22.8bn across 40 new deals in 1Q2025. The majority of issuance was concentrated in the U.S., and primarily within the technology and consumer discretionary sectors.

Opportunities

- Market volatility may present buying opportunities: Fluctuations in the market can lead to the mispricing of high-quality companies, creating an opportunity to acquire securities at a discount.

Risks

- Shifts in U.S. foreign trade policy have introduced a high degree of uncertainty into global markets: Uncertainty regarding tariffs could have meaningful geopolitical and economic impacts.

Structured Credit

Market Conditions: 1Q2025

Corporate – BB-Rated CLO Return: 0.7%30 | BBB-Rated CLO Return: 1.1%31

- Collateralized loan obligation (CLO) spreads widened during the quarter, continuing to offer a premium over equivalent corporate bonds: BBB-rated CLO spreads widened to 333 bps at the end of 1Q2025, a difference of roughly 30 bps from the first quarter; this represents an attractive premium of over 200 bps over BBB-rated corporate bonds.

- Primary market activity varied significantly in 1Q2025: Issuance of U.S. CLOs was marginally lower in the first quarter of 2025 compared to the same period in 2024, while the inverse occurred for European CLOs. CLO issuance in the U.S. and Europe totaled $45bn and €18bn, respectively, in the period, versus $48bn and €11bn in 1Q2024.32

Real Estate – BBB-Rated CMBS Return: 3.8%33

- Real estate structured credit recorded positive performance during the quarter: The asset class continues to benefit from improving investor sentiment around the real estate sector, which was largely driven by the 2024 interest rate cuts.

- Valuations in the commercial real estate (CRE) market show signs of recovery: Green Street’s Commercial Property Price Index increased by 0.3% quarter-over-quarter and by 4.9% year-over-year, while the office subsector index remained flat year-over-year.34 While many property types have come off their recent lows, signaling a shift toward stabilization, the all-property index remains approximately 18% below 2022 peak values.

- Activity in the primary market continues to accelerate: At quarter-end, year-to-date private-label commercial mortgage-backed security (CMBS) issuance amounted to $46bn, more than twice the issuance levels seen during the same period last year, and nearly equivalent to total 2023 issuance.

Opportunities

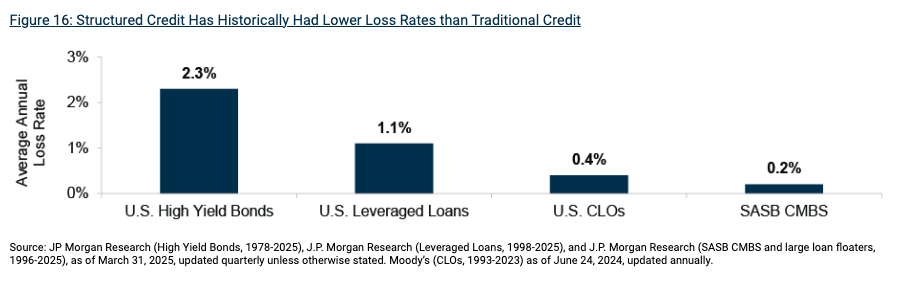

- Corporate structured credit may prove resilient in an economic downturn: CLO debt has shown significant resilience throughout various market dislocations since the Global Financial Crisis, including the pronounced fluctuations in 2020 and 2022-23, as evidenced by their low long-term loss rates. (See Figure 16.)

- Despite stabilizing valuations in the CMBS market, banks remain sidelined due to an excess of CRE loans made before 2022: The retrenchment of banks from this space has created a substantial capital void for borrowers seeking to refinance existing assets or acquire new ones, offering an attractive opportunity for non-bank lenders with available capital and limited problems in their existing portfolios.

Risks

- Limited new loan supply could lead to underwriting compromises: The heightened demand but limited supply of new loans could result in some CLO managers filling warehouses with low quality paper.

- Weakness in the office sector may persist: The sector continues to face multiple headwinds, and its performance may continue to weigh on real estate structured credit indices throughout 2025.

Private Credit

Market Conditions: 1Q2025

- Continued uncertainty surrounding tariff negotiations and their potential impact on the U.S. economy will likely slow M&A activity: We expect management teams in the coming weeks to turn inward to ascertain their companies’ tariff exposure and how tariffs will impact their companies’ cost structure and profitability. As they attempt to tackle the uncertainty within their companies, they’re less likely to pursue acquisitions of other companies, whose tariff exposure would be even more opaque to them. As to private equity sponsors, we expect them to focus on understanding their current portfolio companies’ exposure rather than pursue near-term buyouts. This dynamic will likely reduce demand for private credit.

- BDC redemptions in the face of a market downturn could reduce the supply of private credit: A handful of fast-growing perpetual business development companies (BDCs) have put downward pressure on private credit pricing over the last several years. A sudden reversal in asset flows from their retail investor base could cause these BDCs, who have been a major force in private credit lending, to step back from the market. This reduction in the supply of private credit could potentially offset the lower demand mentioned above.

Opportunities

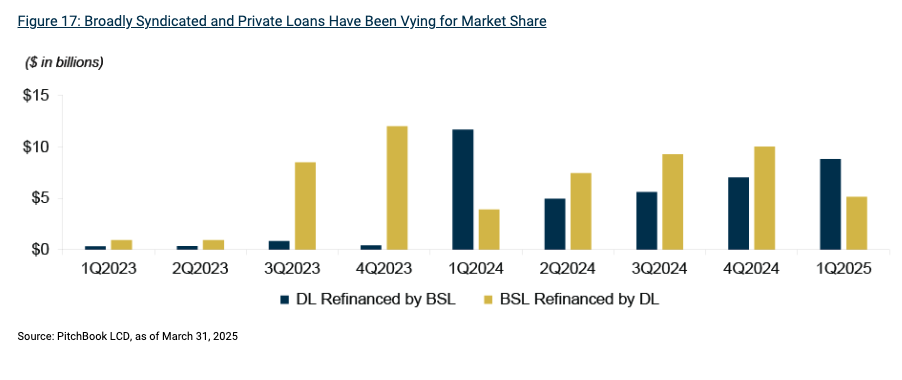

- Private credit could be poised to win market share: With the broadly syndicated loan remaining open only for the highest-quality buyers, direct lenders are leveraging their flexibility and specialized strategies to offer financing solutions that traditional banks are hesitant to provide under current conditions. The volume of private loans refinanced by the broadly syndicated loan (BSL) market in 1Q2025 increased relative to prior quarters, but we believe this trend may reverse amid tariff-driven uncertainty. (See Figure 17.) Even if M&A activity trickles to a halt, there is a material amount of below-investment-grade debt set to mature in the next two-three years. Borrowers tend to address their maturities 18-24 months in advance and if the BSL market remains challenged, this could drive substantial deal flow for direct lenders.

- Increased demand for opportunistic capital solutions and/or rescue financings: As traditional lenders take a more cautious approach amid so much uncertainty, they may eschew borrowers with complex capital needs or any sign of stress. This could grant experienced lenders a compelling opportunity to lend to these borrowers on very lender-friendly terms without much competition.

Risks

- Tariffs, significant economic uncertainty, and the potential for a broad-based economic slowdown could weigh heavily on private credit borrowers’ financial health: A prolonged high-tariff regime will likely strain weaker borrowers’ financial health and liquidity. Borrowers may see their input costs rapidly increase as punitive tariffs are levied on raw material imports. And at the same time, their revenues may fall as (a) domestic customers rein in their spending amid an overall environment of higher prices and (b) retaliatory tariffs push foreign customers toward their home markets. Furthermore, given the resultant uncertainty, businesses and consumers may put off major purchases and delay initiatives as they wait for a more predictable environment. This could drive leverage levels higher, push liquidity levels lower, and cause more borrowers to trip their debt covenants. Moreover, borrowers with a near-term maturity may struggle to refinance their debts. If volatility remains, many direct lenders, particularly those who emphasized capital deployment over disciplined credit selection, may find both their attention and capital increasingly absorbed by a growing number of problem loans in their portfolios.

About Oaktree’s Credit Platform

Oaktree Capital Management is a leading global alternative investment management firm with expertise in credit strategies. Our credit platform has $143.6 billion in AUM and encompasses a broad array of strategy groups that invest in public and private credit instruments across the liquidity spectrum.35 All Oaktree investment activities operate according to a unifying philosophy that emphasizes key principles including the primacy of risk-control and benefits of specialization.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Endnotes

1Coupon based on Credit Suisse Leveraged Loan index.

2McKinsey Global Private Markets Report 2025.

32024 data reflects to the end of 3Q2024 (annualized).

4JP Morgan.

5Credit Suisse Leveraged Loan index, outstanding par amount.

6Yields based on ICE BofA US HY Index, CS Leveraged Loan Index, as of April 2025.

7ICE US High Yield YTW; 7.7%, as of March 31, 2025; average of 6.7% since 2010.

8Financial Times, as of March 23, 2025; quoting Dealogic data.

9Based on outperformance of CCCs in ICE BofA US HY Index.

10ICE BofA US HY Index.

11ICE BofA US HY Index.

12Based on S&P 500 versus STOXX Europe 600.

13DAX index.

14The indices used in the graph are Bloomberg Government/Credit Index, Credit Suisse Leveraged Loan Index, Credit Suisse Western European Leveraged Loan Index (EUR hedged), ICE BofA US High Yield Index, ICE BofA Global Non-Financial HY European Issuers ex-Russia Index (EUR Hedged), Refinitiv Global Focus Convertible Index (USD Hedged), JP Morgan CEMBI Broad Diversified Index (Local), JP Morgan Corporate Broad CEMBI Diversified High Yield Index (Local), S&P 500 Total Return Index.

15ICE BofA US High Yield Constrained Index for all references to U.S. High Yield Bonds, unless otherwise specified.

16JP Morgan for all U.S. default rates, unless otherwise specified. This figure includes distressed exchanges.

17ICE BofA Global Non-Financial High Yield European Issuer, Excluding Russia Index (EUR hedged) for all references to European High Yield Bonds, unless otherwise specified.

18UBS for all European default rates, unless otherwise specified.

19S&P UBS Leveraged Loan Index for all data in the U.S. Senior Loans section, unless otherwise specified.

20Credit Suisse Western Europe Leveraged Loan Index (EUR Hedged) for all data in the European Senior Loans section, unless otherwise specified.

21TXU was removed from J.P. Morgan’s twelve-month default rate calculation in April 2015 resulting in a meaningful decrease in the rate in March 2015.

22ICE U.S. Corporate Index for all data in this section, unless otherwise specified.

23ICE U.S. Corporate AAA Index versus ICE U.S. Corporate BBB Index.

24BofA Securities IG Syndicate Deal Recap.

25Ibid.

26JP Morgan Corporate Broad CEMBI Diversified High Yield Index for all data in this section unless otherwise specified. The emerging markets debt section focuses on dollar-denominated high yield debt issued by companies in emerging market countries.

27Refinitiv Global Focus Convertible Index for all performance data, unless otherwise indicated.

28Bank of America for all default and issuance data in this section, unless otherwise specified.

29Global Convertibles represented by Refinitiv Global Focus Convertible Index; U.S. Convertibles represented by Refinitiv U.S. Focus Convertible Index; Global ex-U.S. Convertibles represented by Refinitiv Global Focus ex-U.S. Convertible Index.

30JP Morgan CLOIE BB Index.

31JP Morgan CLOIE BBB Index.

32JP Morgan for all data in this section, unless otherwise specified.

33Bloomberg US CMBS 2.0 Baa Index Total Return Index Unhedged Index.

34Green Street Commercial Property Index, as of March 31, 2025. The index tracks the pricing of institutional-quality commercial real estate.

35The AUM figure is as of March 31, 2025 and excludes Oaktree’s proportionate amount of DoubleLine Capital AUM resulting from its 20% minority interest therein. The total number of professionals includes the portfolio managers and research analysts across Oaktree’s performing credit strategies.

Notes and Disclaimers

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

This document, including the information contained herein may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent of Oaktree Capital Management, L.P. (together with its affiliates, “Oaktree”). By accepting this document, you agree that you will comply with these restrictions and acknowledge that your compliance is a material inducement to Oaktree providing this document to you.

This document contains information and views as of the date indicated and such information and views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that such information is accurate and that the sources from which it has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover, independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.

This article was previously published on oaktreecapital.com

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All