My father always reminds me that there’s no such thing as a free lunch in life. We must now apply that lesson to investments and question whether anything is truly risk-free.

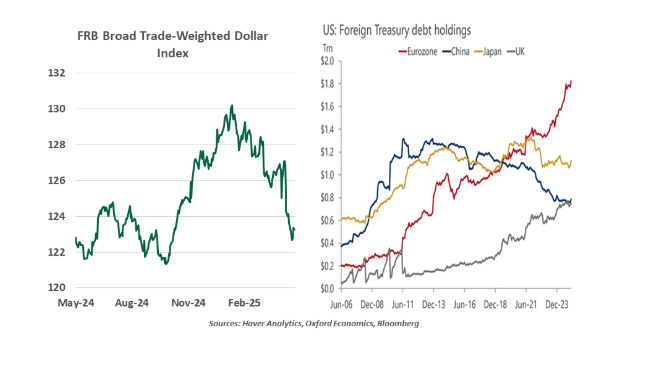

For decades, U.S. Treasuries have been universally regarded as a benchmark and a safe haven asset during periods of turmoil. But of late, U.S government bonds are being traded as a more risky asset. Instead of taking refuge in Treasuries amid equity market volatility, investors have been looking elsewhere. Within days of the U.S. tariff announcement on April 2, the dollar’s value and bond prices tumbled, pushing the yield on the 10-year Treasury up by 50 basis points.

Inflation risks and the uncertainty over the impact of trade policy on the U.S. economy have prompted investors to demand higher returns on bonds. An unwinding of large leveraged bets on Treasury prices amplified the correction.

A broader shift away from dollar assets has also played its part. Policy flip-flops eroded confidence in the U.S. dollar, leading investors to favor emerging market, Japanese and European bonds. Since April 2, emerging market local currency bonds have recorded an inflow of $2.4 billion, up from $500 million in March. A weaker dollar will make imports and commodities more expensive, fueling inflation and potentially keeping the Fed on hold for a while.

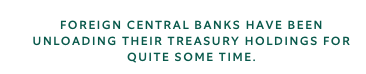

The relatively sharp sell-off also gave rise to conjecture that foreign central banks were selling their Treasury holdings as retribution for America’s war on global trade. However, the evidence for this is thin. Japan and China are the two largest holders of American government bonds and have been reducing their holdings for quite some time. China’s official Treasury holdings have shrunk by almost half to under $800 billion over the past decade, with a focus on maintaining currency stability. Japanese investors were sellers of foreign debt in the first two weeks of April, but they increased their holdings again thereafter.