Why Does Volatility Often Lead to Strong Emerging Equity Returns?

Emerging-market (EM) stocks might not seem an obvious choice for anxious investors during a trade war. But history suggests that past volatility peaks have created favorable moments to invest in EM stocks.

President Donald Trump’s tariff agenda has fueled extraordinary market volatility. Given that many EM countries have significant exports to the US, you might think that EM stocks would be relatively weak. Yet this year through mid-April, the MSCI Emerging Market Index fell by less than the S&P 500. In our view, this indicates that much of the bad news from tariffs was already priced into EM assets while US stocks needed to adjust.

Understanding the Fear Factor

But that’s just the very short term. What can we expect in the coming months? While past performance never guarantees future results, history suggests that EM stocks have performed relatively well after spikes in market turbulence.

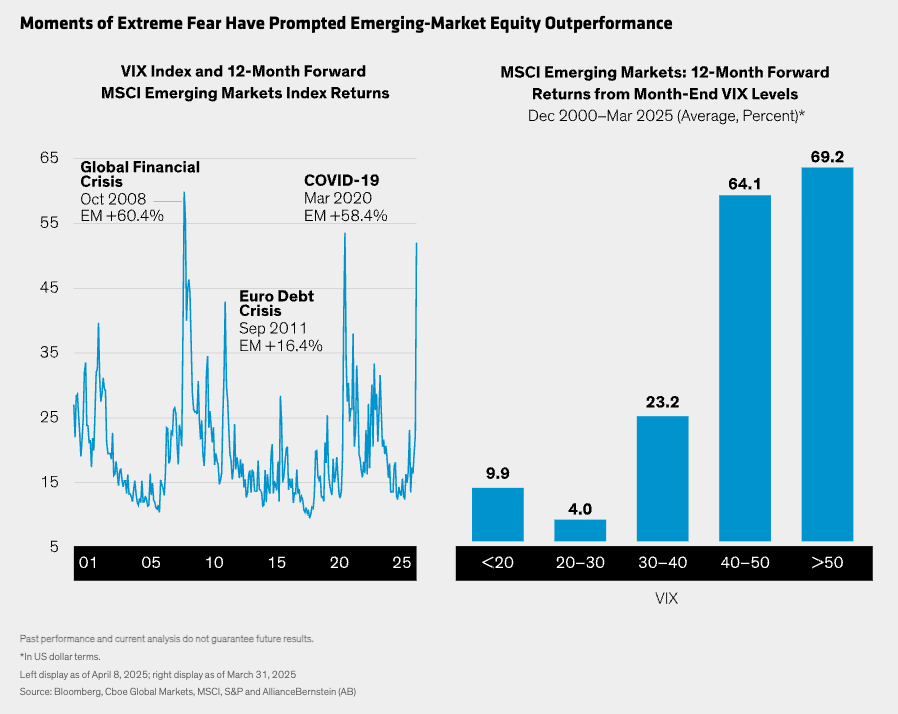

The VIX Index, an index of US equity market volatility, is widely known as the fear index. We looked at market returns after different month-end VIX levels since December 2000 (Display). Extreme VIX readings are uncommon; the index only exceeded 40 nine times at month-end during the 24-year period surveyed above.

When the VIX ended the month between 40 and 50—indicating heightened anxiety—EM stocks returned more than 64% in the subsequent 12-month period on average, well ahead of developed-market (DM) stocks. At even more volatile moments, when the VIX breached 50, EM stocks performed even better over the next 12 months, delivering a 69.2% return on average and widening the gap with their DM counterparts, which returned 34.7%.

It sounds counterintuitive, especially since EM stocks are generally perceived to be riskier than their DM counterparts. So how can we explain this observation? In our view, it comes down to market psychology. Markets often overreact to negative news and bad news gets priced in. When the VIX touches extremely high levels, we think it indicates that investors fear the worst. Yet often, the future turns out better than worst-case scenarios.