A Deep Dive into Covered Call ETFs

Membership required

Membership is now required to use this feature. To learn more:

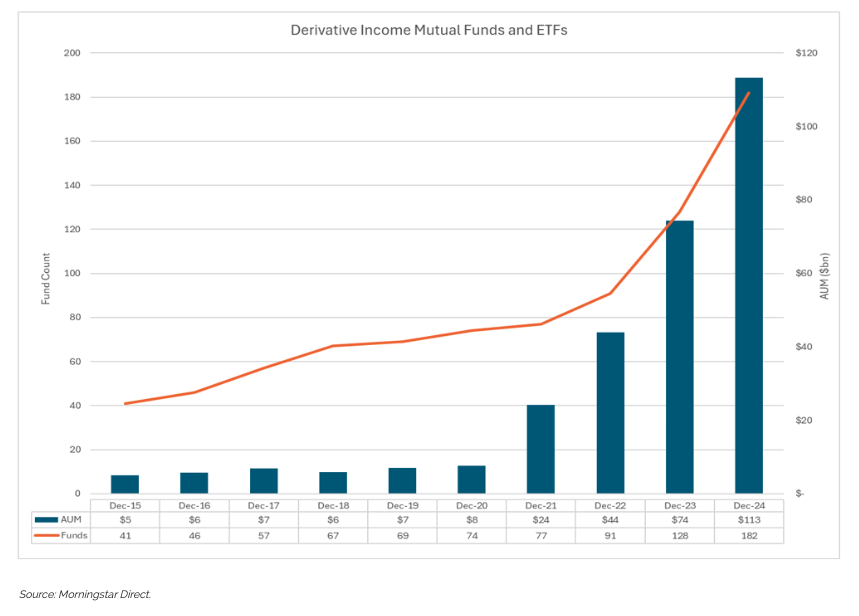

View Membership BenefitsCovered call strategies have been around for a very long time, but covered call ETFs have recently enjoyed a massive increase in popularity.

The reasons for this surge are discussed in a separate post, but it is worth reminding investors to know what you own. What are the drivers of returns for covered call ETFs or derivative income funds? What are the risks? What conditions will be favorable and what will be unfavorable?

We’ll dive into those questions in this post.

Uncovering the Covered Call

With a traditional, long-only portfolio, these questions are easy to answer: an investor owns the stocks because he hopes the stocks will increase in value. “Buy low, sell high” – it is as simple as that. However, a covered call strategy is a bit more nuanced.

With a covered call strategy, the investor has dual goals of capital gains and ongoing income. A covered call strategy owns a portfolio of stocks and hopes for capital appreciation. However, to realize gains sooner rather than later, the strategy will write or short call options on those equities. In exchange for the immediate premium or “income” the investor receives from writing a call, the investor agrees to surrender all the gains if the stock exceeds a pre-defined price point within a given time span.

Are the goals of long-term capital gains and immediate income complementary or are they at odds with one another? Is the investor rooting for the stock to go up, so that he experiences capital gains? Or is he hoping his stocks don’t go up, since he might have sold away those potential gains?

The answer is: It depends.

This is why it is essential for those who are considering a covered call ETF to understand the specifics of the covered call strategy they might be utilizing, and what the variables are in play. In other words, it is important to ‘know what you own’.

Key Due Diligence Considerations for Covered Call ETFs

Some of the key variables in a covered call strategy are:

- What is the underlying stock portfolio?

- Are the options being written on individual stocks or on an index?

- At what price point are further stock gains sold off?

- What time window are the options covering?

- How volatile are the underlying stocks?

- Is the portfolio manager of the covered call strategy passive or actively managing the risks?

We will discuss each of these in turn.

What is the underlying stock portfolio?

The stock portfolio can be based upon a broad-based index like the S&P 500 or the Nasdaq 100. Alternatively, it can be a portfolio of stocks with certain desirable features, like high dividends or strong growth potential. A covered call strategy can also be run on an individual stock rather than a portfolio of stocks. Understanding what the underlying portfolio consists of is the first step in the process.

Are the options being written on individual stocks or on an index?

One can buy or write options on just about anything. When it comes to covered call strategies, another important question is “are the options being written on individual stocks or a broad market index?” Each has its pros and cons. Broad market index options tend to be very liquid and highly traded. However, the premium available for writing call options on an index tends to be less. On the other hand, options on individual stocks tend to have more premium associated with them. This is because the volatility of an individual stock is almost always higher than the volatility of a market index.

At what price point are further stock gains sold off?

This is a key question and refers to the “strike price” of the call option. As mentioned previously, when one writes a call option, one agrees to surrender further gains if the price of the underlying stock exceeds a certain price point. But where is that price point? If the call is written “at the money,” the ATM call writer will receive a higher premium, but won’t participate in any potential capital gains. Alternatively, a call can be written “out of the money,” in which case the call writer has some “run room.” For example, a call option written 3%, 5%, or 10% OTM allows the call writer to enjoy the returns up to, but not beyond those breakpoints. Obviously, the further out of the money a call is written the less premium will be collected.

There is no free lunch.

What time window are the options covering?

Another key variable is the time to expiration. Every option eventually expires. The investor who has written the option is hoping that the option expires worthless. If the option is out-of-the-money at expiration, the call writer will pocket the premium and be free of further obligation. The longer the time to expiration, the greater the risk that the option will go in-the-money and expose the writer to losses. Naturally, this will be reflected in the premiums available when options are written. Shorter-term options offer less premium because they carry less risk, and longer-term options generate higher premiums because they are riskier for the call writer.

How volatile are the underlying stocks?

Volatility is another key driver of option premium. A stock whose price movements tend to be range-bound has a lower probability of its options going in-the-money. This lower probability will translate to a lower premium available to the call writer. Conversely, a stock with high volatility has an increased chance of its options going in-the-money. To compensate for this heightened risk, option writers demand higher premium. Again, the “no free lunch” trade-off is evidenced in pricing.

Is the portfolio manager of the covered call strategy passive or actively managing the risks?

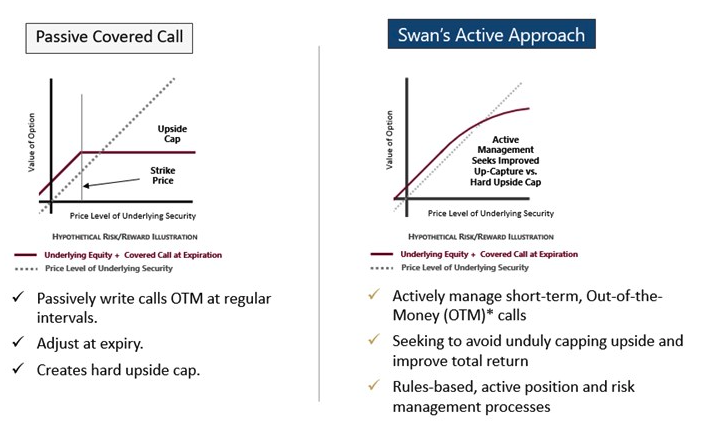

Up until now, all these factors have to do with the trade-off between risks and returns. A risk to the call writing strategy is that a call option will go in-the-money and the call writer forgoes any further gains in the underlying stock. Anything that increases that probability will translate to higher premiums to compensate the call writer for taking on that risk.

The other major consideration when understanding a particular call writing strategy is to ask: “How does the fund manage those risks?”

It is Swan Global Investments’ opinion that actively managing a derivative income strategy offers advantages over a passively managed approach. If the risk is a written call going in-the-money and forfeiting further capital gains, it makes sense that a portfolio manager should do what they can to minimize this risk. An active manager will have many tools available, including:

- Shutting down the trade early

- “Rolling” the trade to higher strike prices

- Having the flexibility to set the strike prices at different points

- Having a wider range of time frames or expiration cycles to write

- Having the freedom not to write calls at all, and wait for a more opportune environment

A passive call writing approach might not have any of these tools available to them. Depending on how the strategy is designed, a passively managed, “set it and forget it” call writing approach might simply let the chips fall where they may and surrender any gains past the strike price should a written call option go in-the-money.

Summary

For Swan Global Investments, this last question is one of the most important ones. Since our inception in 1997 as a manager of options, we have believed that active management is essential in increasing the probability of success.

Whether it is managing the Defined Risk Strategy, Swan’s flagship active, hedged equity strategy, or managing its covered call writing derivative income strategies, Swan has always believed in active management. Having a steady hand on the wheel is essential to mitigate the risks of an options strategy.

Marc Odo, CFA®, FRM®, CAIA®, CIPM®, CFP®, Director of Research and Client Portfolio Manager, is responsible for helping clients and prospects gain a detailed understanding of Swan’s Defined Risk Strategy, including how it fits into an overall investment strategy. His responsibilities also include producing most of Swan’s thought leadership content. Formerly, Marc was the Director of Research for 11 years at Zephyr Associates.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Important Disclosures:

Swan Global Investments, LLC is a SEC registered Investment Advisor that specializes in managing money using the proprietary Defined Risk Strategy (“DRS”). SEC registration does not denote any special training or qualification conferred by the SEC. Swan offers and manages the DRS for investors including individuals, institutions and other investment advisor firms.

All Swan products utilize the Defined Risk Strategy (“DRS”), but may vary by asset class, regulatory offering type, etc. Accordingly, all Swan DRS product offerings will have different performance results due to offering differences and comparing results among the Swan products and composites may be of limited use. All data used herein; including the statistical information, verification and performance reports are available upon request. The adviser’s dependence on its DRS process and judgments about the attractiveness, value and potential appreciation of particular ETFs and options in which the adviser invests or writes may prove to be incorrect and may not produce the desired results. There is no guarantee any investment or the DRS will meet its objectives. All investments involve the risk of potential investment losses as well as the potential for investment gains. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. Further information is available upon request by contacting the company directly at 970-382-8901 or www.swanglobalinvestments.com. 046-SGI-031325

1099 Main Avenue | Suite 206 | Durango, CO 81301 | 970.382.8901

Swan Global Investments is a SEC-registered investment advisor providing asset management services utilizing the Swan Defined Risk Strategy, allowing our clients to grow wealth while protecting capital. Please note that registration of the Advisor does not imply a certain level of skill or training. Swan Global Investments, LLC is affiliated with Swan Capital Management, LLC, Swan Global Management, LLC and Swan Wealth Advisors, LLC. Prior performance is not a guarantee of future results and there can be no assurance, and investors should not assume, that future performance will be comparable to past performance. Disclosure notice and privacy policy.

©2025, Swan Global Investments (“Swan”, "SWAN"), Investing

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All