After starting the year on a high note with the S&P 500 index of U.S. Large Cap stocks posting an all-time high on February 19th, equities retreated during the second half of the quarter, officially falling into correction territory (down 10 percent) on March 13. Increased uncertainty about tariffs and fiscal policy drove the decline. As equities faltered, bond yields declined (yields and bond prices move inversely to each other), with the yield on the 10-year Treasury dropping from 4.79 percent on January 14 to close the quarter at 4.2 percent. Simply put, this drop in yields helped return bonds to their more traditional role of hedging equity downside risk, with the Bloomberg Aggregate Bond Index posting a 2.78 percent gain for the quarter. Indeed, despite rising inflation and elevated concerns about debt levels, longer-dated Treasurys (as represented by the ICE U.S. Treasury 20 Year Plus Bond Index) provided the strongest fixed income return, notching a 4.76 percent advance for the quarter.

Within U.S. equity markets, the S&P 500 fell 4.28 percent and ended the quarter off 8.66 percent from its record high. However, unlike what happened in the fourth quarter of 2024 and for much of the past two years, when the index was driven higher by a select few names, many of those same stocks reversed course and drove the index lower. The “Magnificent Seven” stocks fell 14.76 percent on a market-cap-weighted basis and ended the quarter down 18.3 percent from their record high on Dec. 24, 2024. By contrast, the equal-weighted S&P 500 was nearly flat (down just 0.61 percent). The market “broadened” as more than 62 percent of the S&P 500 index stocks outperformed the overall index, and 50 percent of them actually posted positive returns. By contrast, as we noted in last quarter’s commentary, the fourth quarter of 2024 saw just 29 percent of stocks in the index outperform the overall index. Interestingly, seven of the 11 S&P 500 sectors finished the quarter in positive territory, with industrials (down 0.19 percent), communication services (down 6.21 percent), technology (down 12.65 percent) and consumer discretionary (down 13.8 percent) posting losses. Lastly, value stocks finished slightly higher (up 0.29 percent), while growth stocks faltered—down 8.48 percent. The poor performance of growth stocks pushed the Nasdaq composite index down 10.26 percent for the quarter. In a nutshell, much of the downside in Large-Cap stocks was concentrated.

While the Large-Cap market broadened, the more economically sensitive U.S. Mid- and Small-Cap stocks declined, losing 6.11 and 8.94 percent, respectively. Interestingly, after Large Caps began faltering on February 19, the performance of Large, Mid and Small Caps was nearly identical. Perhaps this is because Small and Mid Caps are viewed by some as insulated from the impact of tariffs, or maybe (as we have reasoned) it’s because these parts of the market have been left behind for much of the past few years and were already trading at lower valuations already aligned with a weaker economy. We continue to believe these segments of the market offer compelling value and return opportunities for intermediate- to long-term-focused investors, regardless of what occurs in the coming weeks and months.

Contrary to what many expected would happen if tariffs became more than just rhetoric, the best-performing equity markets were found internationally. The MSCI International Developed Markets (EAFE) rose 6.86 percent, which was bolstered by Europe’s 12.17 percent return, while the MSCI Emerging Markets Index rose 2.93 percent, largely thanks to China’s 15.02 percent advance. Some of the performance of international stocks was fueled by weakness of the U.S. dollar, which declined 4.3 percent. We believe we are in the early stages of international stocks benefiting from a weaker dollar. The retreat for the dollar also helped push up the Bloomberg Commodity Index to an 8.88 percent gain for the quarter.

While this was generally a tough quarter for investors, the reality is that those with a diversified portfolio were able to weather the storm. The question moving forward is this: Will these recent trends continue?

Near term

Unfortunately, we believe in the near term economic worries and market volatility are here to stay. The overriding questions that have caused volatility over the past couple of years haven’t changed:

- Given that the economy is increasingly bifurcated between those who benefit or are not harmed from higher interest rates and those who struggle, can inflation return to 2 percent without an economic downturn occurring?

- How will the Fed’s reaction to economic developments help shape that outcome?

- Will the Fed cut rates even if inflation is still above 2 percent?

While the Fed did cut rates in late 2024 in reaction to growing labor market weakness, interest rates actually rose on intermediate- and long-term Treasurys in the aftermath as inflation expectations drifted higher and inflation remained stubbornly stuck in the upper 2 to lower 3 percent range. Put simply, it did not alleviate the pain on interest-sensitive segments of the U.S. economy.

These questions have become more complicated in light of uncertainty about recently announced tariff policies that are part of the Trump administration’s agenda. Broadly speaking, we believe this agenda is geared toward restructuring how the U.S. government operates domestically and altering how the country engages in global trade and defense. We believe the administration has a vision for what it wants to attain. However, getting to that goal involves many moving parts and raises plenty of questions about whether the end goal is achievable, what it accomplishes and how much near-term disruption it will cause. Not all parts fit together in a nice and neat manner. For example, the administration wants lower interest rates and has specifically talked about wanting lower yields on 10-year Treasurys. However, tariffs might push inflation and interest rates higher unless there is a recession. There is also talk from the administration of a strong dollar policy. Tariffs could amplify this in the nearer term, but as was the case from 2000 to 2010, a weaker dollar could aid in shrinking the U.S. trade deficit and enhance the country’s global trade competitiveness.

These questions have led to discussion about “international agreements,” like the so-called Mar-a-Lago Accord, which lays out a blueprint for the economy based on a November 2024 paper by Stephen Miran, chair of the Council of Economic Advisers. It has only added to investors’ questions about how all the pieces will come together. “Stagflation” has become a term economists and investors have increasingly used to describe the risks from tariffs, which are slower economic growth and rising inflation. During the first quarter, signs of stagflation began to emerge, with companies raising prices as anticipation of tariffs grew. Consequently, investors began pricing in greater risks of near-term inflationary pressures. The two-year Treasury inflation breakeven climbed and finished the quarter yielding 3.28 percent—this, after its yield had risen from 1.47 percent on Sept 10 (the week before the Fed cut on Sept 18) to 2.54 percent to end 2024.

Importantly, sentiment surveys have increasingly shown that consumers expect inflation to be higher in the future. The most telling of these surveys is the University of Michigan Consumer Sentiment reading of inflation expectation five to 10 years from now. This measure shows inflation expectations jumped from 3 percent at the end of 2024 to 4.1 percent at the end of the first quarter, which is the highest level since 1992. Much has been made about the political polarization that shows up in these surveys, but political biases have always factored into survey results. While consumers’ views of inflation are often tied to their politics, we note that inflation expectations among independents have risen from 3.1 percent to 3.8 percent during the quarter.

As inflation concerns have risen, growth expectations have weakened. The Atlanta Federal Reserve GDP Now tally, which provides an unadjusted snapshot of the economy based on the latest available information, suggests that first-quarter economic growth declined 3.7 percent. An alternate calculation that adjusts for the potential distortion of imports and exports of gold shows the economy contracting by 1.4 percent. Many shrug this off and note that much of the decline has been in soft data that comes from surveys, as opposed to hard data that represents actual actions. We shall see if feelings turn into actions, but certainly the deterioration in current sentiment has been noticeable, and the rise of uncertainty is unmistakable.

Rising uncertainty is likely to cause consumers and business leaders to be increasingly cautious and wait for clarity. This pullback in economic growth and the markets’ overall retreat has led many to wonder whether the president would back away from his tariff threats, or the Fed would seek to steady the economy through another rate cut. Put differently, at what level would a market “put” from either the president or Fed take hold?

We continue to believe both so-called “puts” are unlikely in the near term. The president and his administration have made it clear that they want to restructure the U.S. economy and are willing to pay a nearer-term price if need be. Certainly, a 5 percent drop in U.S. Large-Cap stocks doesn’t appear to be changing minds in the administration, and it’s worth noting that in late 2018, the market fell nearly 19.8 percent without President Trump intervening. The administration has been clear that it is willing to stay the course and is making the case that the president’s agenda is focused on Main Street and not Wall Street.

Alternatively, we don’t believe the Fed can ride to the rescue and preemptively cut rates because such a move would risk showing investors, consumers and businesses that it values the growth-over-price-stability (inflation) mandate. Put differently, inflation expectations (especially in surveys) have risen, while inflation as measured by the Personal Consumption Expenditures (PCE) index has been above the Fed’s 2 percent target since 2021. Most importantly, Core PCE (the Fed’s preferred measure) has been hovering between 2.8 percent and 3.0 percent since late 2023.

For the time being, it appears both the Fed and the Trump puts are unlikely to materialize. As such, markets are likely to face ongoing volatility in response to tariff and fiscal policy news. The economy and markets have to stand on their own. Please note this is not a judgment on the entirety of the current policy that may emerge from Washington. There are policy goals such as tax cuts, deregulation and increased foreign investment in the U.S. that investors will likely view positively. However, even here there are likely to be countervailing factors, especially on any measures that threaten to increase the budget deficit. The U.S. deficit is currently equal to 7.2 percent of gross domestic product (GDP). This level has typically occurred only during world wars and financial crises, not during times of economic expansion. The size of the debt, along with higher interest rates, amounts to annual interest payments that are equal to 3 percent of GDP and exceed what the country spends annually on defense. This is important given that a stated goal of Treasury Secretary Scott Bessent is to bring the deficit down to 3 percent of GDP in the coming years.

In the near term, we believe volatility will remain high as the country moves toward the administration’s desired destination. Uncertainty is a regular fixture of the economy and markets, and in the nearer term tariffs represent an additional shock. But here’s the good news: The U.S. economy remains dynamic. While the possibility of economic and market interruptions exists, historically, the economy has always adapted to new challenges and stocks have eventually risen.

Intermediate to long term

We also note that there is a shift occurring in the world landscape away from globalization as the U.S. alters how it engages in trade and defense. Whether or not this deepens and causes a recession is an open question; regardless, we believe the economic backdrop and market leadership is likely to shift. Think about these comments in terms of Europe getting the message that it must spend more on defense and infrastructure given the shift in U.S. policy. Indeed, after the recent German election that saw historic gains for fringe parties, the more mainstream parties have agreed to launch a 500-billion-euro defense and infrastructure fund, with the broader eurozone likely following suit. Similarly, Japan appears to have halted a 30-plus-year trend of deflation with their recent policies. Indeed, we believe that in the long term, inflationary pressures are likely to remain elevated as economies around the globe “deal” with elevated debt levels. We believe this shifting backdrop was likely a reason behind the International Developed Market’s strong first-quarter relative performance.

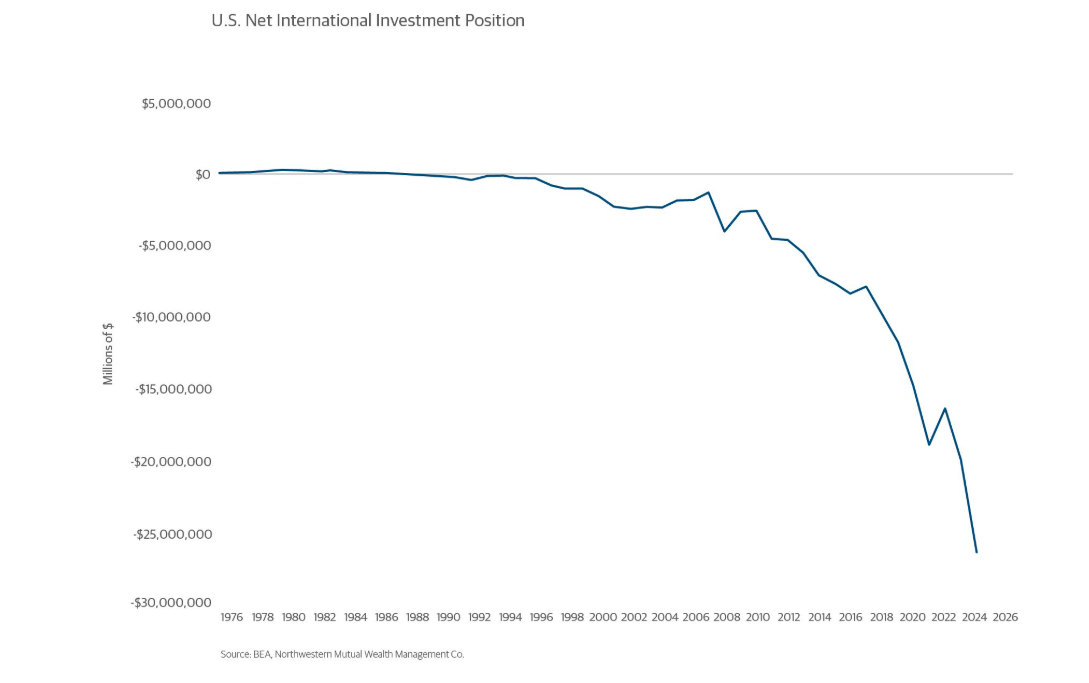

More broadly, we invite investors to consider how this potential new economic reality impacts markets. The administration’s tariff policies are in reaction to the large current account (trade) deficit the U.S. is currently running. The flip side of a trade deficit is the financial account surplus, which is tied to the large trade imbalance. Put simply, when the U.S. runs trade deficits, the dollars that are sent abroad are often recycled back into U.S. financial assets; think investments in equities and fixed income markets. This has resulted in foreign investors now owning $26 trillion more of U.S. assets than U.S. citizens own of foreign assets. If the U.S. cuts its trade deficit, it is likely that foreign capital may flow out of U.S. assets. We highlight this not to imply that it's a good or bad approach but instead to recognize that a likely result of balancing the trade deficit is less demand for U.S. financial assets. These realities threaten to change the future market calculus. Likely less demand for U.S. assets and a weaker dollar would help to restore U.S. manufacturing competitiveness.

Investing implications

There is an antidote for uncertainty that has allowed investors to successfully navigate historical unknowns. Working with an advisor to create a financial plan that focuses on prudent diversification for the investment aspects is key. The reality is that your plan and asset allocation, which you worked with your advisor to develop, account for the facts that markets rise and fall and economies have expansion and contractions. While tariffs may be somewhat unique compared to other headwinds of the recent past, the volatility they are causing is not. But regardless of the cause, your response to volatility should be consistent knowing that your plan was developed to account for temporary downturns.

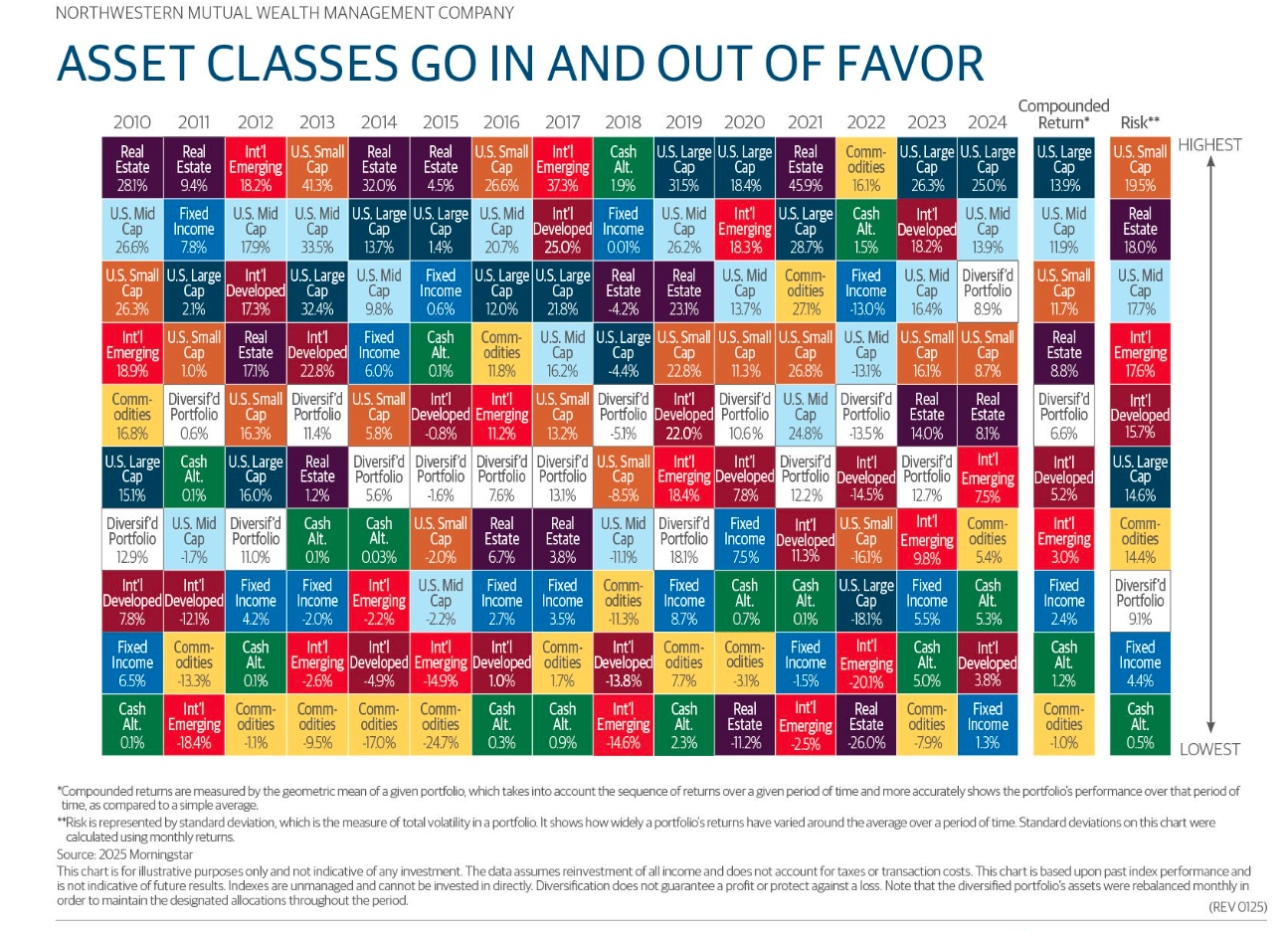

Despite some questioning the value of diversification in the recent past, we remain committed to the concept and encourage investors to do the same. As you can see in the performance quilt below, U.S. Large-Cap equities have reigned as the darlings of investors given their relative outperformance over the past seven years. Unfortunately, this has led many investors to conclude diversification is unnecessary.

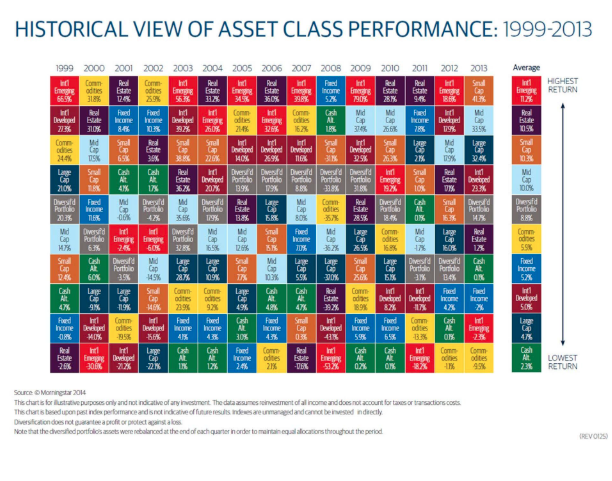

The question we often get after investors look at this table: “Why would we do anything else but invest in U.S. stocks looking forward?” However, investors who base their current and future allocation decisions solely on a review of past winners would have likely gravitated toward different asset classes in years prior to 2017. Perhaps, looking back at a performance quilt from 2013, they would’ve been tempted to invest solely in Emerging Markets or REITs based upon their prior success while under-allocating to the worst-performing equity asset class over the prior 15 years: U.S. Large-Cap equities.

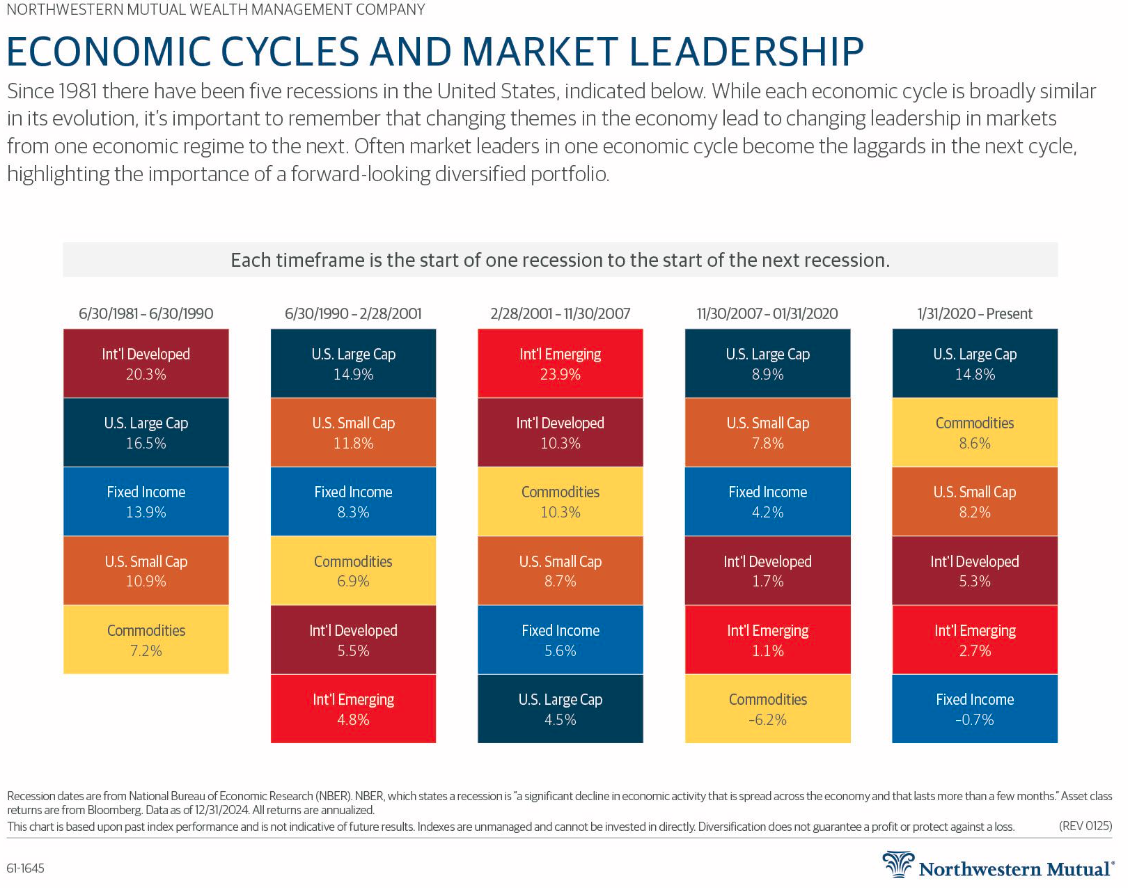

The reality is that economic and market trends can remain in place for some time, and investors often extrapolate them to last forever. This leads them to bid up parts of the market that they believe will continue to benefit from the trends. As we have noted in the past, recessions are often the catalysts for change. The reason is that the movement toward a recession is often a progression in which different parts of the economy are affected based upon their interest rate sensitivity. Unfortunately, as we get closer to that event, markets become concentrated because the economy narrows, which causes investors to abandon underperforming markets for those that are rapidly appreciating. History is littered which such examples, from Japan in the 1980s and tech stocks in the late ’90s to China and emerging markets in the late 2000s and most recently to the Magnificent Seven and U.S. tech stocks. Yet as you can see in the table below, after each recession, a new asset class emerged as the performance leader.

Whether or not a recession occurs is an open question; however, as we have noted in this commentary, we believe the economic backdrop is shifting as the U.S. restructures its role in global matters. We have noted that this period reminds us of late 1995 to 2000, when perceived U.S. exceptionalism and U.S. tech stock dominance had driven investors toward concentrating in U.S. Large-Cap equities above almost all else. Much like today, U.S. stocks were expensive relative to all other asset classes. Then a recession hit, and the narrative changed, with market leadership shifting dramatically. In each circumstance, as the chart narrative shows, the prior concentrated leadership shifted to the next cycle’s laggards. While we could dissect each economic cycle and show how performance leadership changes, we think the quilt below is best at illustrating why we believe in the value of diversification.

Over the past 25 years there have been various asset classes that have taken their turns in a leadership position. The reality is that no one can time those shifts. Rather than trying to shift concentration between various markets over time, we believe a much better strategy is that of diversification. Our research underscores this view.

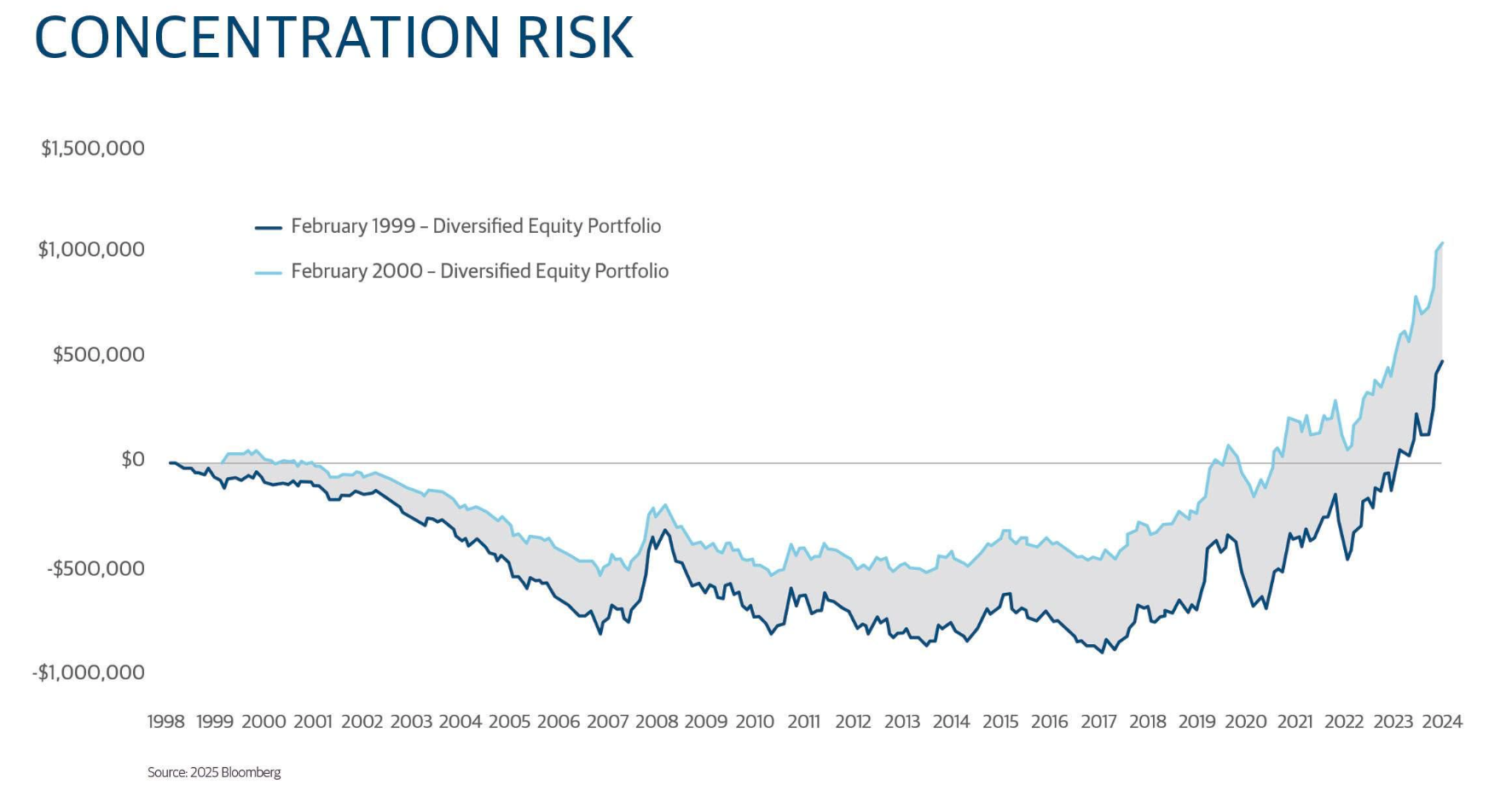

The chart below shows the results had one invested $1 million on January 1, 1999, at the end of each month in one of two portfolios. We chose to end the initial investment window in March of 2000 because that is when the market downturn began. The first portfolio is the S&P 500 alone, and the second one is a diversified portfolio of different equity asset classes (42 percent S&P 500, 11 percent S&P 400, 5 percent S&P 600, 7 percent Real Estate, 24 percent International Developed and 11 percent International Emerging). The diversified portfolio was then rebalanced monthly. We then took each one of these portfolios and charted their relative performance until the end of 2024. As you can see, the diversified portfolio provides stronger performance up until recently, when the S&P 500 produced historically strong returns. The $1 million invested in February 2000 was the first to break even in mid-2021, while the $1 million invested in February 1999 was the last to break even, 25 years later in February 2024. All of the others were in between.

While many will note the S&P 500 has now eclipsed the diversified portfolio, we note two important considerations: First, this comes after a strong U.S. stock market run over the recent past that has returned us in many ways to where we were in 1998 and 1999: near record-high absolute and relative valuations coupled with a belief of American exceptionalism driven primarily by a narrow slice of companies tied to a technology theme (the internet then versus artificial intelligence today). When you couple that with the above discussion, the question has to shift to what happens next? And second, think about all those years in between when individuals may have needed to draw from their portfolios—or perhaps a more important question is whether you would have stayed with the concentrated S&P 500-only strategy during those years of underperformance.

Maybe this time is truly different; maybe history won’t repeat. But what if it does? We continue to believe that diversification is the answer for investors to reach their goals and objectives. It is a tried-and-true philosophy that has helped guide investors through volatile markets of the past.

Against this backdrop, we believe the best course is to stay true to your plan and the process; stay true to diversification and a long-term focus. Doing so should result in the coming months registering as little more than a blip on your long-term path to gaining or keeping financial security.

Commentary is written to give you an overview of recent market and economic conditions, but it is only our opinion at a point in time and shouldn’t be used as a source to make investment decisions or to try to predict future market performance.

There are a number of risks with investing in the market; if you want to learn more about them and other investment-related terminology and disclosures, click here.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Northwestern Mutual is the marketing name for The Northwestern Mutual Life Insurance Company and its subsidiaries. Life and disability insurance, annuities, and life insurance with longterm care benefits are issued by The Northwestern Mutual Life Insurance Company, Milwaukee, WI (NM). Longterm care insurance is issued by Northwestern Long Term Care Insurance Company, Milwaukee, WI, (NLTC) a subsidiary of NM. Investment brokerage services are offered through Northwestern Mutual Investment Services, LLC (NMIS) a subsidiary of NM, brokerdealer, registered investment advisor, and member FINRA and SIPC. Investment advisory and trust services are offered through Northwestern Mutual Wealth Management Company (NMWMC), Milwaukee, WI, a subsidiary of NM and a federal savings bank. Products and services referenced are offered and sold only by appropriately appointed and licensed entities and financial advisors and professionals. Not all products and services are available in all states. Not all Northwestern Mutual representatives are advisors. Only those representatives with Advisor in their title or who otherwise disclose their status as an advisor of NMWMC are credentialed as NMWMC representatives to provide investment advisory services.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Northwestern Mutual Wealth Management

Read more commentaries by Northwestern Mutual Wealth Management