Key takeaways:

- The reciprocal tariffs were at the high end of market expectations making it likely that inflation will be higher and economic growth lower in 2025.

- Corporate bond markets largely reacted in line with their credit ratings. More credit sensitive high yield bonds saw their spreads gap wider on the prospect that companies will take a hit to earnings and trade and supply chains will be disrupted.

- Value is potentially emerging as markets can overreact. Our preference is to move up in quality but look for price dislocation across the credit spectrum.

A liberation of sorts

President Trump’s “Liberation Day” – where he revealed the reciprocal tariffs that would be levied on goods from countries coming into the US to help rebalance trade and re-industrialise the US – was a liberation of sorts. Markets at least know how each country is viewed by the administration and the seriousness of Trump’s trade agenda.

What is the pain?

The tariffs announced on 2 April were more draconian than the market expected. Tariffs are being levied according to a formula based on a country’s trade surplus with the US and then discounted. China’s reciprocal tariff rate was set at 34% (this extends to 54% when the 20% rate applied to China to address the Fentanyl crisis is imposed). The European Union rate is 20%. A baseline tariff rate of 10% is being levied on all goods entering the US, so countries such as the UK, which have balanced trade with the US, have a rate of 10%. The baseline tariff rate of 10% takes effect on 5 April, with higher rates from 9 April.1 Certain critical sectors are outside the scope of these reciprocal tariffs such as gold, pharmaceuticals and semiconductors as they face separate investigations, while auto imports face a 25% tariff.

Interestingly, Scott Bessent, US Treasury Secretary, told Fox news that this was the high-water mark if countries do not retaliate,2 while Sebastian Gorka, Deputy Assistant to President Trump, told the BBC there is room for negotiation.3 This opens the door to tariffs potentially being lower, but it relies on countries not retaliating and making concessions to the US. It is too early to tell how that will unfold.

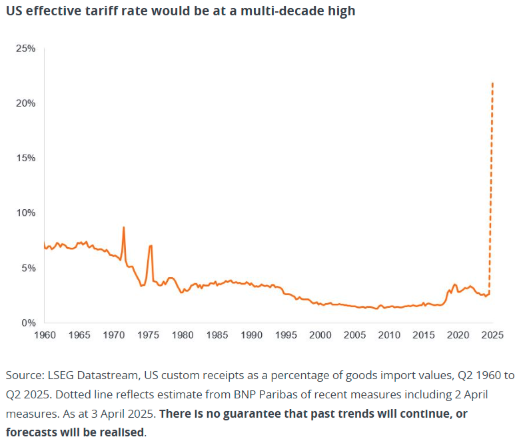

On average, the measures will lift tariff rates on goods coming into the US from around 2.5% last year to around 22% according to early estimates.3 This upends the relatively easy access to the US market that other countries have enjoyed for several generations.

As many questions as answers

There are a lot of variables at play, however, and many questions that only the fullness of time may be able to answer:

-

How much of the tariffs will be passed on to the US consumer? Some will have to be passed on, so expect inflation to be higher in the US. Early estimates are that these tariffs could add more than one percentage point to the US inflation rate.4

-

Will volumes be affected? This will depend on how price sensitive customers are and how much companies seek to redirect trade to markets outside the US. If tariffs act as an extra tax on US consumers, this will weigh on economic growth. Early estimates are that US GDP could take a hit of around 1% and Euro Area GDP growth be lower by 0.4-0.8%.4 There is a risk that countries will seek to dump volume intended for the US on other markets, potentially triggering tariffs elsewhere.

-

Will exporting companies absorb some of the cost? It is likely that corporate profit margins at companies that export goods to the US and import goods from overseas into the US will take a hit. We should get some guidance from companies about the potential hit to earnings in the coming earnings results, but it may take a couple of quarters before we get meaningful data. In the meantime, we will be paying close attention to where sales are generated and the level of cross border trade within companies, to establish how they might be affected.

-

Will exchange rates soften the impact? It is not unusual for currencies to move up or down by 10% in a year in ‘normal’ times so some of the tariff impact may be softened (or aggravated) by currency moves.

-

Will companies alter their capex plans? We have already heard some companies announcing investments in the US, but we would expect most companies to wait a while to see how sales and profits settle before making major changes. For some companies, the tariffs will be a material factor in their decision-making but for others they will make little to no difference. Again, the coming quarterly earnings announcements may give more colour on what companies are thinking.

Fixed income market’s initial reaction

Moves tended to be predictable with those sectors most exposed to trade being hurt more. As expected, high yield took a bigger hit than investment grade given its greater sensitivity to credit risk.

Investment grade markets were fairly composed, with US investment grade credit spreads (the difference between the yield on a corporate bond and government bond of similar maturity) on average widening 10 basis points (bps) on 3 April and Euro investment grade spreads widening 7bps. In fact, declines in government bond yields meant yields on investment grade bonds on average dipped slightly on the day. We saw bigger falls in US high yield bond prices than in European high yield, with some bonds falling by up to ten percentage points. US high yield spreads widened by 59bps, taking the average yield to worst up to 8.0%, while Euro high yield spreads rose 21bps, taking the average yield to 6.0%.6 Among the sectors being hardest hit were retail given the high propensity for imports within the sales mix. For example, a BB-rated bond issued by Wayfair, the online retailer, in mid-March has seen its price fall 8 points since issuance and its yield rise from 7.75% to close to 10%.7 Wayfair’s supplier base is heavily exposed to China and Vietnam. Similarly, energy has taken a hit as concerns grow that lower economic growth could feed into lower oil and gas prices.

The auto industry breathed a sigh of relief as it appears to have avoided additional tariffs beyond those implemented on 26 March. A 25% tariff will be imposed on imported passenger vehicles, including sedans, SUVs, crossovers, minivans, and cargo vans, as well as light trucks. Key automotive components such as engines, transmissions, powertrain parts, and electrical components will also face this tariff. Trump described these tariffs as “permanent” and expressed disinterest in negotiating exemptions, contrasting with the reciprocal tariffs announced on 2 April, which allow room for negotiation.

Do we lean into a cheaper market?

Markets can overreact and we think some value is emerging. We are sharpening our pencils to analyse which issuers will be most affected. On average, however, valuations are not excessively cheap – most credit sectors, for example, are not pricing in a recession.

Therein lies the hardest part to predict. How will these tariffs affect demand? Tariffs can act as a consumer tax that burdens spending and confidence, and consequently affect earnings and cash flow. Markets were of the view that real GDP growth in the US in 2025 would be around 2.5%8 coming into this year. The US Federal Reserve in March lowered its projection to 1.7%.9 If the tariffs announced do knock one percentage point off GDP we need to remember that will not be evenly distributed, so we need to ascertain which companies will escape (or even benefit) and which will take a hit. The most significant impact is likely on discretionary big-ticket items (such as household goods and home projects), while businesses with pricing power, like auto parts and luxury goods, may face less impact. Conversely, domestically-focused businesses such as food producers, supermarkets, and defensive quick-service restaurants might experience a bit more relief.

Recall that back in 2022 economists were predicting recession as the US Federal Reserve hiked interest rates, yet this never transpired. There has been recent evidence of softness in consumer sentiment survey data, but it is not yet reflected in hard economic data, which remains resilient. It is possible that tax cuts and reliefs help the US consumer, while in Europe, extra fiscal spending in Germany and rearmament compensates for some of the hit to exports. If European growth suffers, we expect the European Central Bank to relax monetary policy to boost growth given the more favourable inflation outlook in Europe. Similarly, we might expect China to implement some form of stimulus.

We recognize there are a lot of moving parts but that is because the situation remains fluid. We still do not know whether or how countries will retaliate. In this environment of uncertainty, we are assessing different bull and bear scenarios to better understand potential outcomes. Ultimately, our preference is to move up in quality, but we are looking to take advantage of price dislocations across the credit spectrum.

1Source: ww.whitehouse.gov, 2 April 2025.

2Source: Fox News, ’Treasury Secretary Bessent tells countries not to retaliate after sweeping Liberation Day tariffs’, 2 April 2025.

3Source: BBC, Newsnight, 2 April 2025.

4Source: BNP Paribas, 3 April 2025. There is no guarantee that past trends will continue, or forecasts will be realized.

5Source: Deutsche Bank, 3 April 2025. There is no guarantee that past trends will continue, or forecasts will be realized.

6Source: Bloomberg, ICE BofA US Corporate Index (investment grade), ICE BofA Euro Corporate Index (investment grade), ICE BofA US High Yield Index, ICE BofA Euro High Yield Index, Govt option-adjusted spreads, yields to worst, 3 April 2025. Yields may vary and are not guaranteed.

7Source: Bloomberg, Wayfair 7.75% 15 Sep 2030, price and yield movement between 12 March 2025 and 3 April 2025 (intraday). Past performance does not predict future returns.

8Source: Aggregation of World Bank, OECD and IMF forecasts, 1 January 2025.

9Source: Federal Reserve, 19 March 2025

Definitions

The ICE BofA Euro Corporate Index tracks EUR denominated investment grade corporate debt publicly issued in the Eurobond or Euro domestic markets.

The ICE BofA Euro High Yield Index tracks EUR denominated below investment grade corporate debt publicly issued in the euro domestic of eurobond markets.

The ICE BofA US Corporate Index tracks US dollar denominated investment grade corporate debt publicly issued in the US domestic market.

The ICE BofA US High Yield Index tracks US dollar denominated below investment grade corporate debt publicly issued in the US domestic market.

Basis point (bp) equals 1/100 of a percentage point, 1bp = 0.01%.

Capital expenditure (capex): Money invested to acquire or upgrade fixed assets such as buildings, machinery, equipment or vehicles in order to maintain or improve operations and foster future growth.

Cash flow: The net amount of cash and cash equivalents transferred in and out of a company.

Corporate bond: A bond issued by a company. Bonds offer a return to investors in the form of periodic payments and the eventual return of the original money invested at issue on the maturity date.

Credit rating: An independent assessment of the creditworthiness of a borrower by a recognised agency such as S&P Global Ratings, Moody’s or Fitch. Standardised scores such as ‘AAA’ (a high credit rating) or ‘B’ (a low credit rating) are used, although other agencies may present their ratings in different formats. BB is a high yield rating.

Credit spread: The difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Default: The failure of a debtor (such as a bond issuer) to pay interest or to return an original amount loaned when due.

Gross domestic product (GDP). A measure of the size of the economy.

High yield bond: Also known as a sub-investment grade bond, or ‘junk’ bond. These bonds usually carry a higher risk of the issuer defaulting on their payments, so they are typically issued with a higher interest rate (coupon) to compensate for the additional risk.

Inflation: The rate at which prices of goods and services are rising in the economy.

Investment grade bond: A bond typically issued by governments or companies perceived to have a relatively low risk of defaulting on their payments, reflected in the higher rating given to them by credit ratings agencies.

Issuance: The act of making bonds available to investors by the borrowing (issuing) company, typically through a sale of bonds to the public or financial institutions.

Maturity: The maturity date of a bond is the date when the principal investment (and any final coupon) is paid to investors. Shorter-dated bonds generally mature within 5 years, medium-term bonds within 5 to 10 years, and longer-dated bonds after 10+ years.

Tariff: A duty or tax imposed on goods entering a country.

Yield: The level of income on a security over a set period, typically expressed as a percentage rate. For a bond, at its most simple, this is calculated as the coupon payment divided by the current bond price.

Yield to worst: The lowest yield a bond with a special feature (such as a call option) can achieve provided the issuer does not default. When used to describe a portfolio, this statistic represents the weighted average across all the underlying bonds held.

Volatility. A measures of risk using the dispersion of returns for a given investment. The rate and extent at which the price of a portfolio, security or index moves up and down.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Janus Henderson Investors

Read more commentaries by Janus Henderson Investors