Using Fixed Income within Multi-Asset Portfolios

At RiverFront, we like to view fixed income through the lens of multi-asset portfolios. We have previously discussed how understanding fixed income can often be beneficial to valuing equity, in our discounted cash flow (DCF) primer. Beyond equity selection and valuation, we want to discuss how fixed income can be used in portfolio construction, particularly for more equity-oriented portfolios. We believe smaller fixed income allocations, combined with a higher risk tolerance, create opportunities to use certain fixed income building blocks in ways that go beyond just a core allocation. Today’s Weekly View discusses how we view certain fixed income investments within the context of complimenting equity portfolios, specifically focusing on fixed income’s downside protection and total return enhancement.

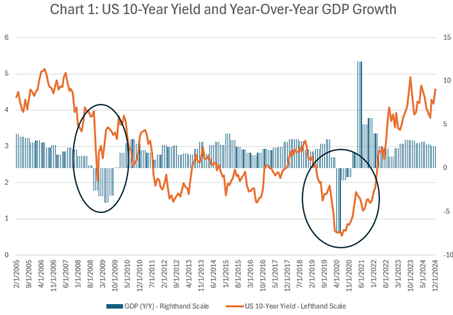

We Believe Long Treasuries Can Be a Good Recession Hedge

As a starting point, in our 2025 Outlook we do not view a recession as the most likely outcome this year, placing a 20% chance on a ‘bear case’ outcome. With that being said, we believe that properly hedging out portfolios against the potential risk of a negative market outcome is important. In our view, long maturity treasuries (government bonds with maturities longer than 10 years) are an efficient way of accomplishing this hedge. This feature is illustrated in Chart 1, below: while the relationship is not perfect, we can see that when US GDP turns negative, 10-year yields tend to drop as well, such as during the recessions of 2008 and 2020 (circled areas).

Source: FactSet, RiverFront. Data monthly as of December 31, 2024. Chart shown for illustrative purposes. Not indicative of RiverFront portfolio performance. Index definitions are available in the disclosures.

This is not to say that all equity investors should be buying the longest tenured bonds possible. We believe these long maturity assets become increasingly attractive when an investor is taking on more risk within their equity portfolio. This creates a two-front decision matrix, where an investor must consider both the relative value of treasuries and the holistic risk profile of their portfolio when considering hedging risk.

Hedging Against Stagflation is a Little More Complicated… Prefer Energy Over TIPS for Risk-Tolerant Portfolios

Another potential downside risk a portfolio manager may seek to hedge is stagflation, or the combination of economic STAGnation and elevated inFLATION. As we discussed in a previous Strategic View, stagflation requires different forms of portfolio protection relative to a ‘garden-variety’ disinflationary recession. Specifically, Treasury Inflation-Protected Securities (‘TIPS’) are often considered a good hedge against inflation within fixed income. For managers who are strictly attempting to beat a fixed income benchmark, TIPS can provide a way to help insulate their portfolio against inflation. However, for a multi-asset portfolio, TIPS with longer maturities often perform poorly in times of rising inflation if interest rates are rising at the same time. In these circumstances, TIPS with shorter maturities can be much more effective, but are not the panacea they are often chalked up to be. For starters, since they tend to be a popular inflation hedge, they can often be overvalued when inflation risk looms. Secondly, given their low coupon rates, they have a large amount of interest rate sensitivity relative to similar maturity current coupon bonds. This becomes an acute issue because when expected inflation spikes, rates usually follow, causing potential losses in TIPS.

Since we are viewing this from the perspective of a multi-asset allocator, we would also point to both energy commodities and energy equities as a potential inflation hedge. Both of these instruments can be effective hedges against inflation but come with their own downsides. Direct investments in commodities come with poor tax treatments and a lack of cash flows, in our view, while we believe energy equities are only good hedges for early stages of stagflation. However, since we put a low probability on stagflation and view energy stocks as currently undervalued, they are our preferred stagflation hedge currently in more risk-seeking portfolios.

Corporate Bonds Can Offer Equity-Like Returns…In the Right Environment

When considering corporate bonds in the context of a traditional fixed income portfolio, yield is often the desired goal. For example, in the current market, the high yield market is yielding 7.43% and defaults are well below historical averages. We believe that these factors combined create an attractive yield opportunity relative to the broad fixed income market.

However, from a multi-asset perspective, we believe an investor must also consider the total return of these bonds, including price appreciation. For corporate bonds, this price appreciation often comes from movements in credit ‘spreads’ (the incremental yield an investor earns over treasuries for taking credit risk). Specifically, when ‘spreads’ contract corporate bond prices rally, and vice versa. This relationship is why context matters when making a credit investment in a multi-asset portfolio. When an investor’s starting point is tight spreads, there is little room for further tightening. Conversely, when investing in credit during a ‘wider’ spread environment, there is more potential for spread tightening and thus total returns that exceed current yields. Considering today’s market again, spreads are currently tight relative to history. Thus, we believe, within the context of a multi-asset portfolio, corporate bonds are less attractive than they are in the context of a fixed income portfolio. This is why we are overweight equities relative to fixed income across our balanced portfolios.

Conclusion: Portfolio Context is Key for Fixed Income

Within the context of multi-asset portfolios, we believe combining longer duration Treasuries with selective credit exposures is an efficient way to enhance total returns and provide protection against recession. However, these features must be considered in the context of the equity portion of the portfolios. For example, our long horizon portfolios are currently overweight equity relative to our global benchmarks, so we have a dedicated position in 25+ year, zero coupon treasuries. Since these bonds do not pay coupons, they are highly sensitive to interest rates, which makes them efficient because it takes less capital to adjust the desired maturity profile of the portfolio. As we either add to or trim our equity allocation, it would follow that we would adjust this hedge to arrive at our desired risk profile for the whole portfolio. A similar dynamic would exist if we began to add more credit risk to these portfolios; we would adjust (or at least reevaluate) the risk profile of our equity selection to make sure we are not unintentionally over risking our portfolio.

For more news, information, and analysis, visit the ETF Strategist Channel.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Important Disclosure Information:

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa). This effect is usually more pronounced for longer-term securities). Fixed income securities also carry inflation risk, liquidity risk, call risk and credit and default risks for both issuers and counterparties. Lower-quality fixed income securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Foreign investments involve greater risks than U.S. investments, and can decline significantly in response to adverse issuer, political, regulatory, market, and economic risks. Any fixed-income security sold or redeemed prior to maturity may be subject to loss.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Dividends are not guaranteed and are subject to change or elimination.

Definitions:

Discounted cash flow (DCF) refers to a valuation method that estimates the value of an investment using its expected future cash flows. DCF analysis attempts to determine the value of an investment today, based on projections of how much money that investment will generate in the future.

The term cash flow refers to the net amount of cash and cash equivalents being transferred in and out of a company. Cash received represents inflows, while money spent represents outflows.

The discount rate is the interest rate the Federal Reserve charges commercial banks and other financial institutions for short-term loans. The discount rate is applied at the Fed's lending facility, which is called the discount window. A discount rate can also refer to the interest rate used in discounted cash flow (DCF) analysis to determine the present value of future cash flows. In this case, investors and businesses can use the discount rate for potential investments.

Free cash flow to equity is a measure of how much cash is available to the equity shareholders of a company after all expenses, reinvestment, and debt are paid. FCFE is a measure of equity capital usage.

Treasuries are government debt securities issued by the US Government. Treasury securities typically pay less interest than other securities in exchange for lower default or credit risk. With relatively low yields, income produced by Treasuries may be lower than the rate of inflation.

The 10-year Treasury bond yield is the interest rate the U.S. government pays to borrow money for a decade, serving as a benchmark for other interest rates and a key indicator of investor sentiment about economic conditions. It matters because it influences borrowing costs, impacts the valuation of financial assets, and signals expectations about inflation and economic growth.

A credit spread, also known as a yield spread, is the difference in yield between two debt securities of the same maturity but different credit quality.

Broad fixed income refers to the types of securities that seek to pay investors fixed interest or dividend payments until their maturity date. Broad fixed income securities assume the same risks as other bonds.

The coupon rate is calculated by weighting each bond's coupon by its relative size in the portfolio. It indicates whether the underlying fund owns more high- or low-coupon bonds. There can be advantages to holding higher coupon bonds, but many funds buy them simply to tempt investors with a high payout. This can be damaging to investors for two reasons. The first is that higher-coupon bonds often carry greater risk than lower-coupon issues. The second is that when these bonds don't carry extra risk, they are old issues that the fund has paid up for and if the offering doesn't amortize the extra yield, investors are likely to find that their principal erodes over time.

Treasury Inflation Protected Securities (TIPS) are Treasury securities that are indexed to inflation in an effort to protect investors from the negative effects of inflation. The principal value of TIPS is periodically adjusted according to the rate of inflation as measured by the Consumer Price Index (CPI), while the interest rate remains fixed. TIPS will decline in value when real interest rates rise. Portfolios that invest in TIPS are not guaranteed and will fluctuate in value.

Commodities include securities that tract bulk goods and raw materials, such as grains, metals, livestock, oil, cotton, coffee, sugar, and cocoa, that are used to produce consumer products. Buying commodities allows for a source of diversification for those sophisticated persons who wish to add this asset class to their portfolios and who are prepared to assume the risks inherent in the commodities market. Any commodity purchase represents a transaction in a non-income-producing asset and is highly speculative. Therefore, commodities should not represent a significant portion of an individual’s portfolio.

Inflation is a gradual loss of purchasing power, reflected in a broad rise in prices for goods and services over time.

Stagflation is the persistent high inflation combined with high unemployment and stagnant demand in a country's economy.

Disinflation is what happens when the inflation rate falls but remains positive. In disinflation, prices continue to increase but at a slower rate.

A recession is a significant, widespread, and prolonged downturn in economic activity. A common rule of thumb is that two consecutive quarters of negative gross domestic product (GDP) growth indicate a recession. However, more complex formulas are also used to determine recessions.

Gross Domestic Product (GDP) is the monetary value of all finished goods and services made within a country during a specific period. GDP provides an economic snapshot of a country, used to estimate the size of an economy and growth rate.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at riverfrontig.com and the Form ADV, Part 2A. Copyright ©2025 RiverFront Investment Group. All Rights Reserved. ID 4250645

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by Riverfront Investment Group