Today’s market outlook seems more challenging for investors—including defined contribution (DC) plan participants. We expect lower real, or inflation-adjusted, returns in the decade ahead—a result of less robust stock returns and higher inflation rates. Because target-date solutions play a critical role in retirement outcomes, we see a need to further diversify glide paths across a broader set of assets.

The Need for New Asset Frontiers in Target-Date Glide Paths

Some public markets offer fewer options for diversification than they have in years past. For example, the number of publicly traded US companies has fallen from a peak of over 7,000 in 1996 to fewer than 4,000 today. We expect a growing number of firms to tap private capital, given that the US commercial loan market has shrunk as a share of gross domestic product (GDP) over the past five years.

Growing concentration in public equity markets has also raised the stakes on risk management. The combined weight of the S&P 500’s top 10 companies—less than 20% of the index in 1996—is over 35% today. And while the stock-bond correlation will likely decline from its highs of the past few years, it may not return to the substantially negative levels of past decades that made it a diversification staple.

Integrating Private Assets in Glide-Path Design

For investors seeking new avenues to enhance return and diversification potential, private markets have become an increasingly popular dimension. We think they make sense for DC savers, too, with their long-term investing focus.

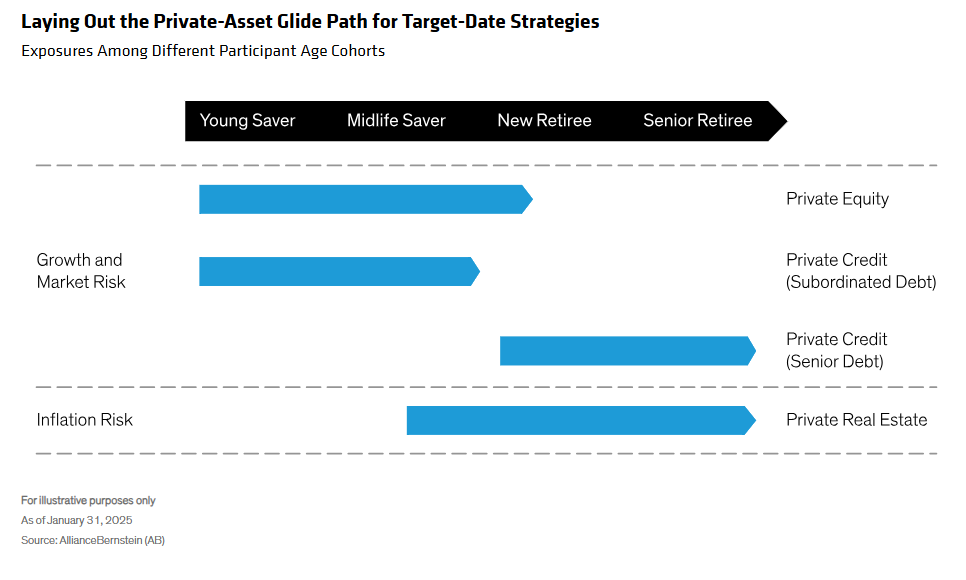

Because the mix of risks evolves during participants’ lives, the mix of private assets must adapt along the glide path (Display). Private equity, for example, offers strong growth potential but brings substantial risk. That’s why we think it makes sense mostly for young and midlife savers, enhancing the return potential of public equities and adding diversification. For older participants, we think equity exposure should come mainly in public markets, which have less risk and offer more liquidity.

Private real estate, which generally offers less return potential and risk than private equity, has historically provided robust income and been an effective cushion during inflation spikes. This nature, in our view, makes it effective primarily for participants near retirement or already there. For younger participants who require more long-term return potential, we think public real estate investment trusts should be the main access point for any real estate exposure needed.

Private credit has offered higher return potential than public credit and has been less correlated with public equity. It may help manage growth risk and market risk, though allocations may vary widely depending on the specific strategy. For young and midlife savers, we believe allocations should focus on strategies with higher potential returns, such as subordinated debt, which carries more risk because it’s lower in borrowers’ capital structures. The higher volatility that comes with this potential may not be suitable for participants with shorter investment horizons, so allocations should shift more toward higher-quality strategies as participants approach and enter retirement.

Aligning private asset exposures with the glide path may seem relatively straightforward at the surface level, but it’s vital to dig deeper into several elements of this new diversification dimension.

Assess return potential, which can vary substantially. Return potential is wide-ranging, influenced by many factors. For example, based on our assessment, many “DC friendly” private real-estate strategies have less opportunistic exposure and more core exposure, with lower return potential but less risk than traditional private real-estate strategies. In private credit, the wide range of strategy types could also produce wide-ranging return potential. And performance potential in private markets evolves over time. In private equity, a stockpile of dry powder and a change in the path of interest rates could dampen future returns. Outperformance potential, especially within private equity, depends a lot on the specific manager, too. And the stakes are high, with alpha potential generally accounting for a larger share of private equity returns.

Fully account for true underlying economic risks. The short-term volatility of private assets might seem muted versus public assets, but much of that gap stems from less-frequent pricing. In reality, private assets are driven by the same economic factors as public assets—including inflation, real interest rates and economic growth. And they’re not immune from systemic shocks, such as the Global Financial Crisis. Private assets generally exhibit higher long-term risk than public assets. Characteristics such as leverage and holdings concentration can vary substantially, as can their impact on returns and risks. And factor exposure may overlap with public allocations, requiring a top-level evaluation of overall exposures.

Manager selection is always critical. Alpha is typically a sizable share of private-asset returns, especially within equity and real estate. In our view, this puts a premium on choosing the right manager. What’s more, our research suggests that underperforming private equity managers have historically trailed poor-performing public equity managers by a sizable margin, emphasizing the manager selection point. And with the private equity market outlook facing headwinds, we believe outperformance will require very astute selection of managers going forward to enable outperformance. For private credit, we also believe it’s crucial to select managers with diversified investments: unlike other private assets, credit has a capped upside, and individual losses will likely dominate its return risk.

Consider operational and fiduciary aspects. Private market allocations offer potential to enhance target-date returns and diversification, but they’re highly likely to increase the total expense ratio of an overall portfolio, so allocation decisions should consider any fee constraints. Also, major selloffs in public markets such as in 2022 may leave overall private-market exposure higher, a result of liquidity and rebalancing constraints. The size of private allocations should ensure a buffer to help avoid costly forced selling in these events. Also, public allocations should be designed to provide an added liquidity buffer and tool to help manage daily cash flows. Plan sponsors might find custom target-date solutions to be suitable for accommodating the unique operational considerations of private assets.

In our view, bringing the private-market dimension to target-date glide paths has the potential to improve retirement outcomes, enhancing returns and diversification alongside public exposures. Developing an in-depth understanding of how these exposures behave is a critical step.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

“Target date” in a fund’s name refers to the approximate year when a plan participant expects to retire and begin withdrawing from his or her account. Target-date funds gradually adjust their asset allocation, lowering risk as a participant nears retirement. Investments in target-date funds are not guaranteed against loss of principal at any time, and account values can be more or less than the original amount invested—including at the time of the fund’s target date. Also, investing in target-date funds does not guarantee sufficient income in retirement.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

© AllianceBernstein

Read more commentaries by AllianceBernstein