Over the years, the high-yield markets have advanced to the point where investors can be increasingly selective about how they source income. Given today’s elevated yields and wide array of high-quality offerings, generating income doesn’t necessitate a white-knuckle roller-coaster ride. But it may require broadening your horizons. We believe investors looking to prioritize efficient income—maximizing income while managing downside risk—should consider a global, multi-sector approach.

Increasing Income Opportunities by Going Global

Sourcing efficient income typically includes US high-yield corporate bonds—that’s part of the recipe. But it’s not the sum total. In our view, some of the most compelling avenues for generating efficient income lie beyond US shores. The global high-yield corporate universe is roughly twice the size of the US high-yield market, so going global opens significantly more possibilities than a US-only strategy.

One of the biggest benefits of a global opportunity set is the ability to diversify portfolio risk. After all, one region of the world may be at an entirely different stage of the economic cycle than another while companies in the same industry may be operating under different interest-rate regimes—allowing for idiosyncratic opportunities at the issuer and security level. This kind of desynchronization means investors can pull different levers to target desired risk levels—allowing for a more defensive posture when needed.

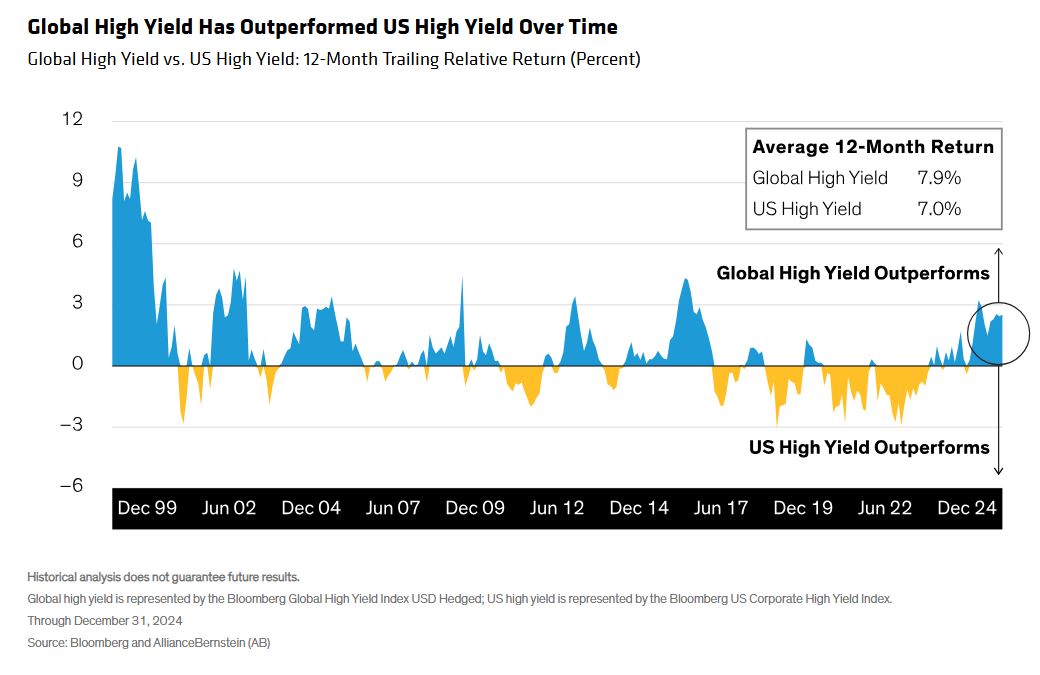

We believe that investing globally can also shore up portfolio yields and help generate alpha. US high-yield bonds periodically outperform their global peers, and vice versa. These fluctuations in market leadership tend to occur in cycles. After several years of US high-yield dominance, global high yield has reasserted itself over the past 24 months. Over longer periods, the Bloomberg Global High Yield Index has outpaced the Bloomberg US Corporate High Yield Index by 0.9%, on average, since 1999 (Display)—a general trend we expect to continue over the next couple of years.

Finding Income Opportunities Beyond US High Yield

We believe that today’s income-oriented investors should also consider a multi-sector approach that goes beyond US high-yield corporates. For example, today we see benefits from opportunistically investing in emerging-market (EM) corporates, securitized debt, euro high yield and even investment-grade credit.

- EM corporate bonds have historically allowed for participation in rising markets while, somewhat counterintuitively, exposing investors to less downside during market downdrafts. Our research suggests that EM corporates with revenues tied to the US dollar are likely to benefit from a stronger dollar. EM corporates can also tap the potential of fast-growing markets in the developing world.

- Securitized debt instruments, such as select residential mortgage bonds, offer competitive yields. And our analysis shows that, in many cases, these investments carry less risk than US high-yield bonds. Certain parts of the securitized markets also provide diversified exposure to the US consumer.

- In Europe, high-yield bond yields look historically attractive from our vantage point. Starting yields have frequently been a good predictor of future returns over the ensuing three to five years, irrespective of market conditions. And in today’s market, a global approach to bond investing can boost yields further if bonds denominated in foreign currencies are hedged back to the US dollar.

We believe that, in addition to providing plentiful opportunities to capture more income and strengthen potential returns, a multi-sector approach helps diversify portfolios and acts as a bulwark against geopolitical disruptions and other shocks.

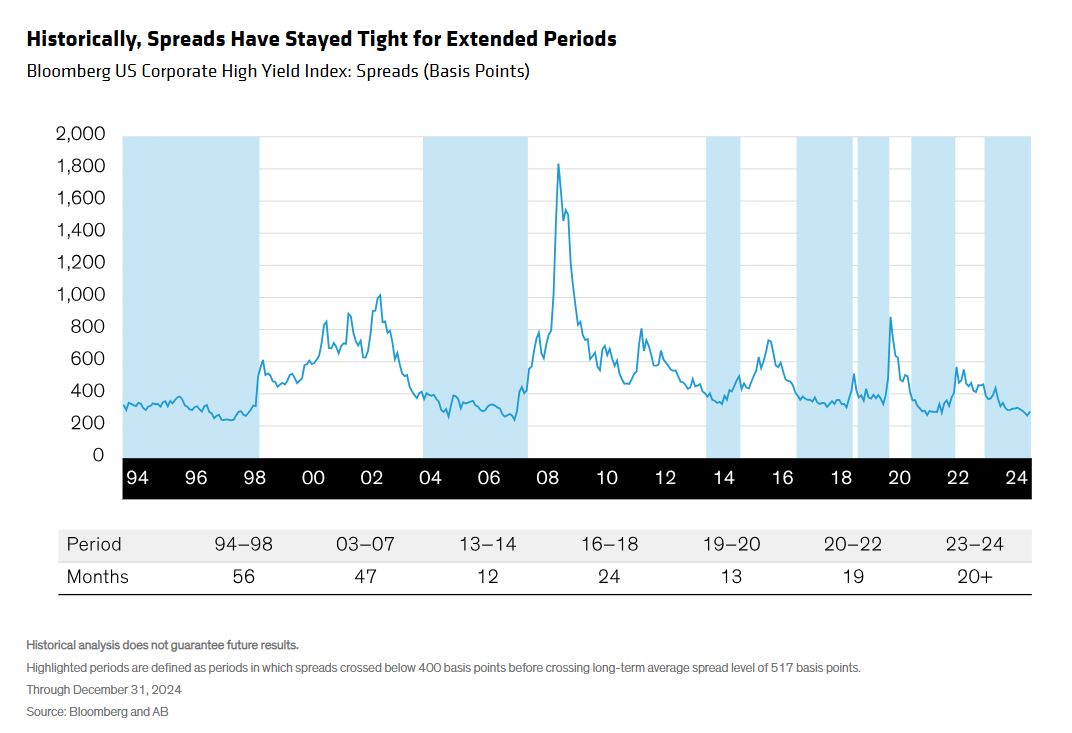

Tight Spreads Shouldn’t Deter Investors

Some investors are concerned about narrow yield spreads in the corporate credit markets. We agree that credit spreads are indeed tight. However, we don’t think that’s a reason to avoid corporate bonds today. For one thing, historically, spreads have remained tight for more than two years, on average (Display). We don’t expect them to widen meaningfully anytime soon.

Moreover, we believe spreads are narrow for good reason. Corporate fundamentals are sound, which has supported demand—particularly on the long end of the yield curve. With a new US administration taking the reins, we expect this trend to continue in the US credit markets. Key provisions of 2017’s Tax Cuts and Jobs Act are expected to sunset this year, and any extensions or enhancements to this legislation could keep spreads range-bound.

Tactically De-Risking with High-Yield Bonds

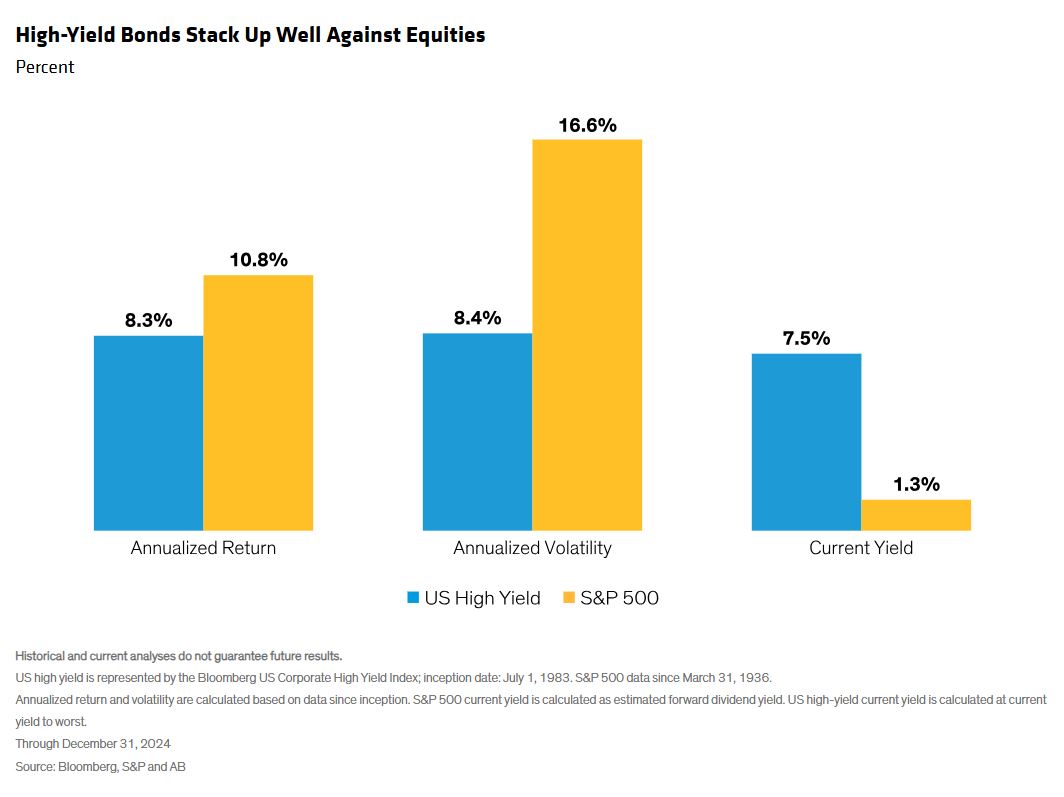

Beyond expanding their horizons, we believe investors should consider reframing their view of high-yield bonds. Even though high-yield bonds look like other bonds, they don’t necessarily act like them. In fact, over time, high-yield bonds have produced 75% of the return of equities with just half the risk (Display).

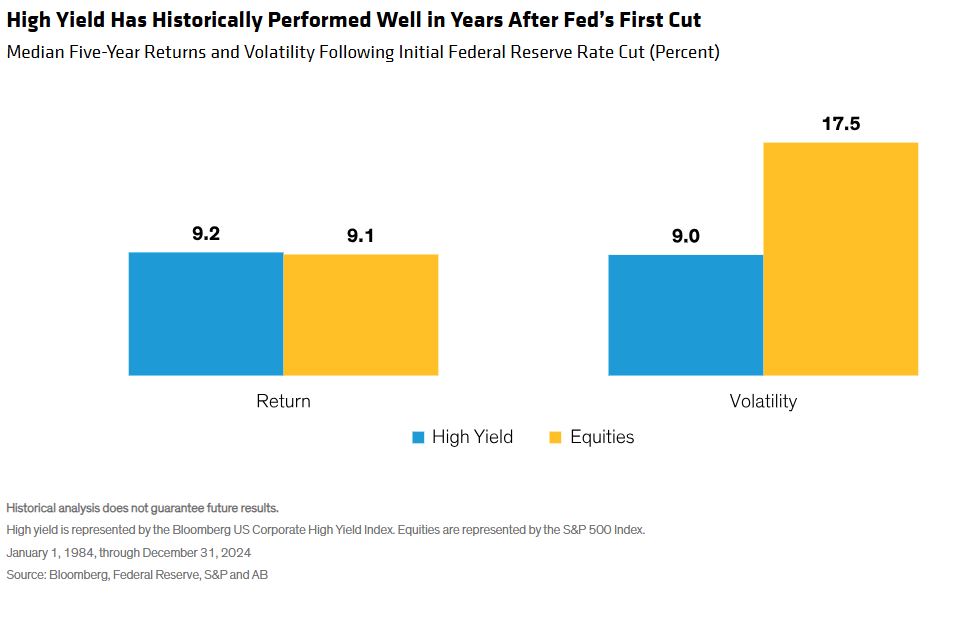

What’s more, during major equity sell-offs, equities have generally declined more sharply than high yield while high-yield bonds have recovered more quickly. That could prove timely if growth slows, equity returns moderate and stock valuations come off their current lofty levels over the coming years, as we expect. Meanwhile, high yield has historically outperformed in the years following the Fed’s initial rate cut (Display). That’s why, in our view, high-yield bonds may be a sensible substitute for a small portion of an investor’s equity allocation today.

The coming year presents no shortage of potential risks and policy uncertainty. But dialing down risk doesn’t have to mean sacrificing income. For opportunistic investors, a global, multi-sector approach may be just the formula for navigating an uncertain market environment.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams and are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein