The US housing market faces a delicate balancing act in 2025, influenced by lingering effects of the pandemic and persistently high mortgage rates. The current landscape reveals a market of contrasts: regions experiencing booming inventory due to post-pandemic migration, while others contend with persistent shortages, all amid price growth that continues to challenge affordability.

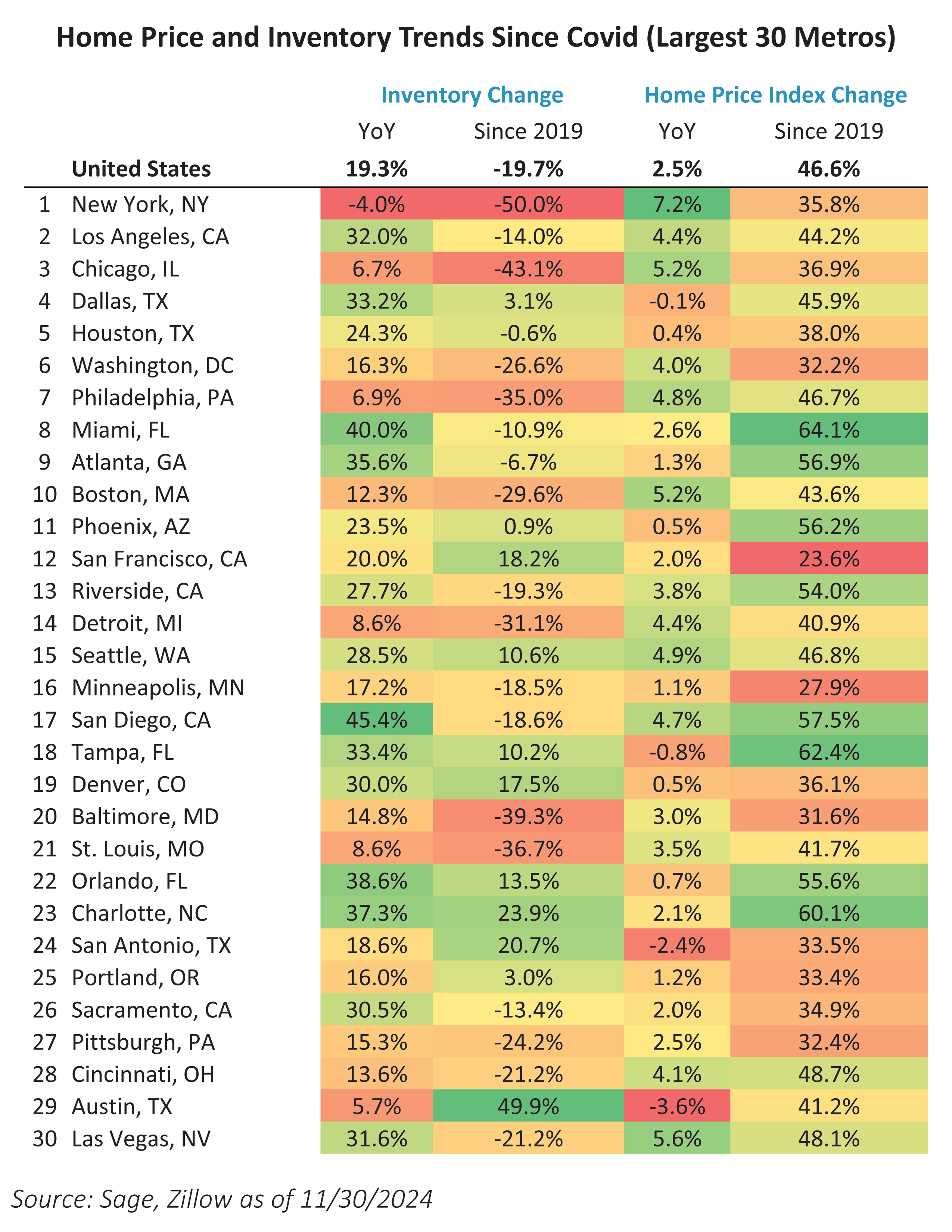

Given the slowdown in home sales, inventory levels have risen on a year-over-year (YoY) basis in most cities, with the national average showing a 19.3% YoY increase. However, inventory remains 19.7% below 2019 levels, indicating a long-term shortage compared to pre-pandemic norms. This persistent inventory gap highlights the broader challenges of housing supply in a post-pandemic world.

Nationally, home prices grew 2.5% YoY but have surged 46.6% since 2019. Notably, the metros that have seen little inventory growth since 2019, such as New York, Boston, and Chicago, have had the highest home price appreciation on a YoY basis. Conversely, cities such as Austin, Denver, Tampa, and San Antonio exhibited signs of price stabilization or modest declines amid higher post-pandemic inventory increases.

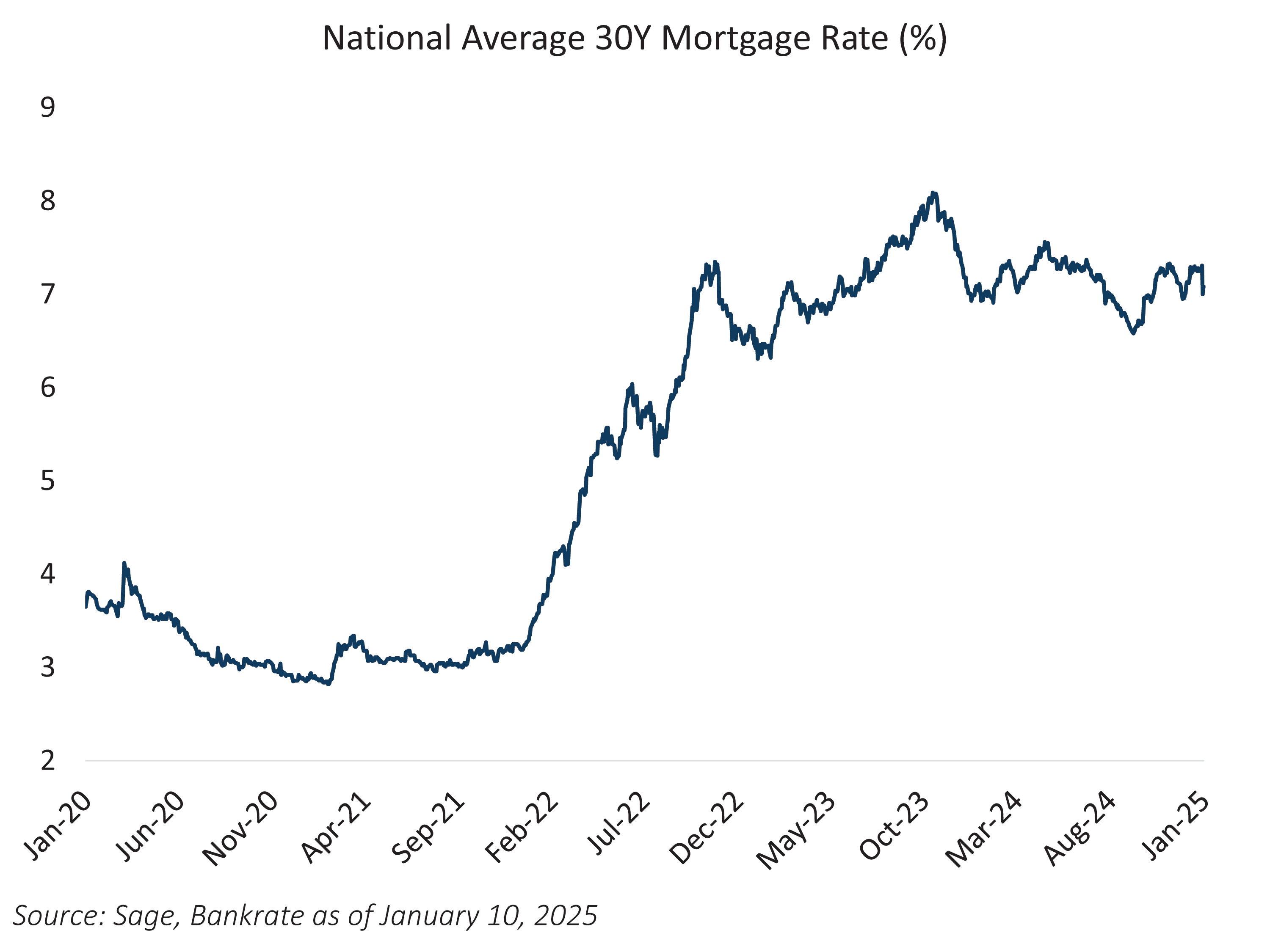

Meanwhile, mortgage rates have remained elevated, hovering above 7% after peaking above 8% in late 2023. This steep rise, from sub-3% rates in early 2021, has had a profound impact on affordability, particularly for first-time homebuyers, leading to decreased purchasing power and tempered overall demand.

Amid robust economic expansion and persistently strong labor, economic activity, and inflation data, expectations for the federal funds rate have shifted upward. As a result, markets now anticipate one additional hike during the current cycle, with rates rising again starting in 2026 — a significant departure from the deep cuts projected just a month ago. This change underscores a transition in Fed pricing from a "soft-landing" to a "no-landing" scenario, reinforcing the likelihood of a prolonged period of higher rates for the housing market.

The higher-for-longer rate environment could have several implications for the housing market:

- Limited Inventory Growth: Sellers may hesitate to list homes due to "golden handcuff" effects, where existing low mortgage rates are too attractive to give up. This could continue the trend of negative housing supply nationally.

- Regional Disparities: Markets with historically higher price volatility, such as Las Vegas, NV, and Phoenix, AZ, may experience increased sensitivity to rate changes. Meanwhile, resilient markets like New York City may continue to see steady demand.

- Shift to Renting: As affordability challenges persist, more prospective buyers may turn to the rental market, potentially exacerbating rental inflation in already tight markets.

While resilient home prices and limited inventory reflect underlying economic strength, persistently high rates and affordability concerns could dampen demand in the near term. The housing market is at a critical juncture in 2025 – it is supported by strong economic and labor market conditions while grappling with high borrowing costs and potential economic policy shifts from a new administration.

Originally published at Sage Advisory

For more news, information, and strategy, visit the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more commentaries by Sage Advisory