Autumn leaves—and interest rates—have started to fall. Yet investors are entering the home stretch of 2024 with some spring in their step—with good reason. While growth is slowing, it’s doing so at a gentle stroll, not a rush to recession. We think that more clarity on the path of rates will boost investor confidence and support capital formation and transaction activity across private markets.

Lower rates will also reduce the cost of capital—a welcome respite for many borrowers after the rapid rise in borrowing costs over the last two years. We think this is likely to stimulate M&A activity and demand for directly originated middle market loans.

Meanwhile, the secular trend of bank disintermediation—particularly in consumer lending—should spark new opportunities for investors who want to grow and diversify exposure within private credit.

A New Economic Backdrop

Navigating the economic environment may get more challenging in the months ahead. While major central banks in the US, UK and Europe all appear committed to gradual rate cuts, it’s possible that growth may stall more abruptly in 2025, mandating more aggressive easing.

But predicting which segments of the economy might suffer most and where defaults may appear is difficult. In our view, nobody should expect to predict any of that with accuracy.

A better way to prepare portfolios, in our view, is to reduce exposure to potential downside risks and bolster diversification. This doesn’t have to be difficult. We think it comes down to having a laser-like focus on quality and ensuring that overall private-credit allocations are diversified across multiple forms of debt.

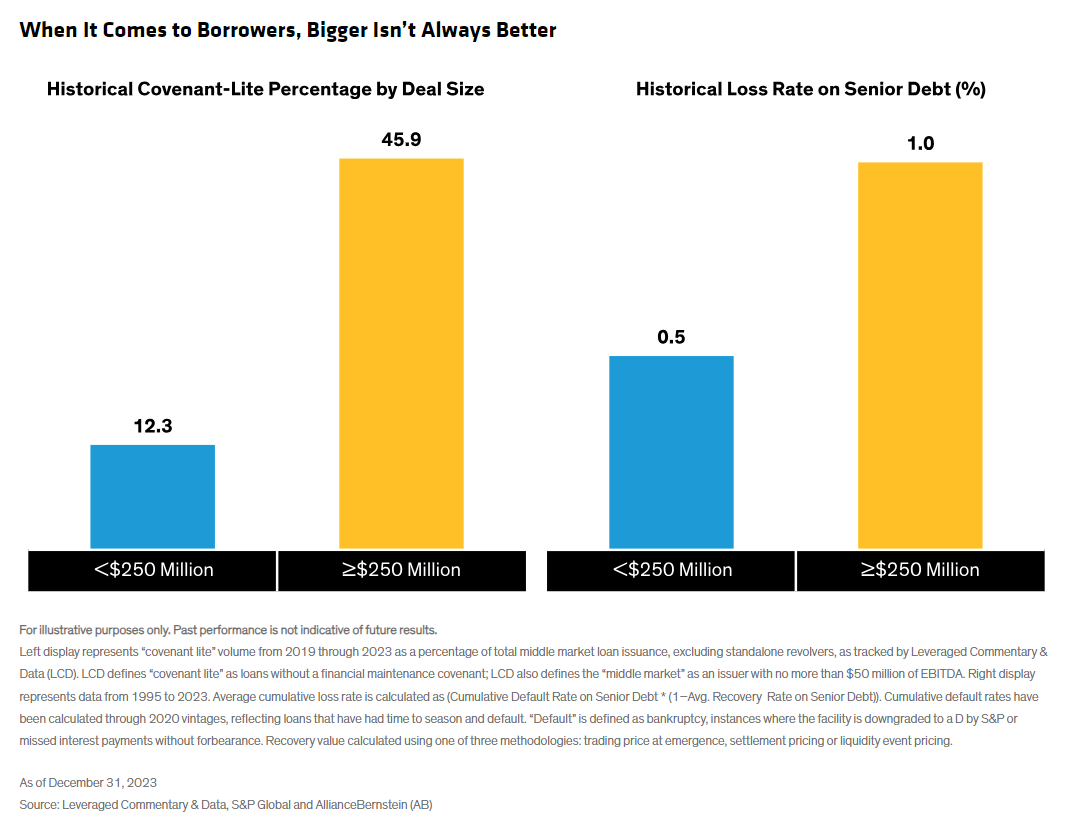

Middle Market: Quality over Quantity

For many investors, corporate credit is the linchpin of their private allocation. Because these loans are directly negotiated, they often come with attractive return premiums and stronger protections than broadly syndicated loans. According to Preqin, direct lending to companies today stands at about $1.5 trillion and is expected to nearly double over the next five years.

But like many financial assets, not all private debt is created equal. With loans to core middle market companies—often defined as those with an enterprise value between $200 million and $2 billion—lenders typically have more power to negotiate strong protective covenants. These include caps on the amount of leverage a borrower can have or a required minimum level of liquidity. Covenants provide lenders with negotiating leverage to amend loan terms in their favor if a borrower underperforms, which may improve downside mitigation potential (Display).

Such features are always valuable, but perhaps never more so than in uncertain conditions. It’s less common to find these covenants in loans to companies at the larger end of the middle market. This is in part because these borrowers typically have more options for credit, including tapping the broadly syndicated bank loan market. The result: typically, more favorable terms for the borrower—and less protection potential for lenders.

What’s more, core middle-market lender groups tend to be smaller and more like-minded. This allows them to act nimbly and work effectively together with borrowers should issues arise.

We also think it’s important to take a nuanced view of risk across corporate direct lending. Pinpointing risk drivers is important. For example, investors should ask where revenue drivers are coming from. Consumer spending? Corporate spending? If corporate spending is the source, is it from capital expenditures, which tend to be less predictable? Or is it tied to mission-critical operating expenses?

The answer may help investors determine the best balance between risk and reward lies.

Consumer Credit: The Great Diversifier?

It may seem counterintuitive to embrace consumer credit in an uncertain growth environment. But we believe a careful approach can increase return potential and diversify asset allocations.

There’s no “free lunch” in investing. But the next best thing, in our view, may be diversification.

We think an effective approach is to partner with bank and nonbank originators to acquire pools of whole consumer loans. Weighing in at more than $6 trillion—and forecast to hit $10 trillion by 2028—this form of asset-based finance helps grease the gears of the real economy. It provides much of the financing for auto loans, mortgages and point-of-service loans, as well as some commercial and residential property.

The correlation to corporate credit has been low thanks to a broad range of sectors and investments that often comprise hundreds, if not thousands, of underlying collateral assets and loans.

Consumers do face challenges today, including a weakening labor market. Despite some bearish signals, we don’t see signs of broad weakness. Consumers aren’t monolithic, nor is consumer debt performance throughout a cycle. And mixed signals can create a promising environment for investors with strong sourcing relationships and underwriting skills.

A Burgeoning Market Offers Growth and Diversification

We expect the opportunity set to keep growing as private credit expands into various forms of lending that used to be provided by banks. And just as importantly, more investment options will provide more ways to fine-tune allocations to suit the macroeconomic environment.

Matthew D. Bass

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein