What Will Fed Rate Cuts Mean for the U.S. Dollar?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe U.S. dollar has declined by about 4% since July against a basket of currencies including the euro, British pound and Canadian dollar and is now hovering near the low end of a broad trading range that has prevailed since late 2022. Over those past two years, every time the U.S. dollar index has dropped to this current level, it was due to expectations for lower American interest rates. Each time it fell, it rebounded.

Now, with the Federal Reserve embarking on what appears to be an extended rate-cutting cycle, the foreign exchange value of the U.S. dollar has the potential to continue falling. However, we don't expect a long-term dollar bear market to develop. The strength of the U.S. economy relative to its major trading partners—such as Mexico, Canada, China and Japan—tends to support the value of the dollar.

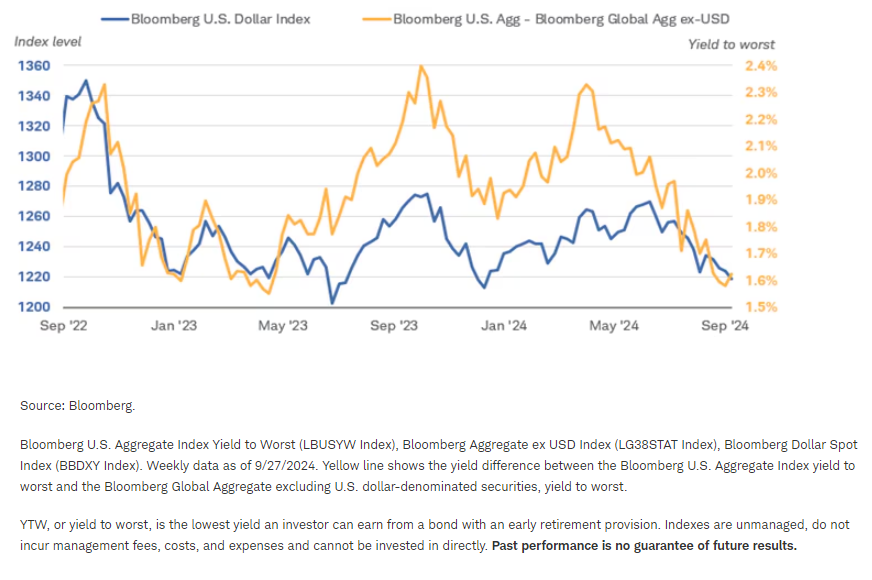

Relative yield changes have contributed to the dollar's decline

The factors pushing the dollar higher relative to other major currencies for much of the past decade remain largely intact. U.S. economic growth has continued to outpace growth in other major countries, and U.S. interest rates are higher than those in the rest of the Group of 10 (G-10) countries.1 Stronger growth and higher yields on government bonds tend to attract foreign investment and discourage outflows of capital.

However, those differences have narrowed over the past few months as the Fed kicked off its rate-cutting cycle with a larger-than-expected 50-basis-point (0.50%) cut. The yield on the Bloomberg U.S. Aggregate Bond Index has fallen compared to the Bloomberg Global Aggregate Bond Index excluding the U.S. (ex USD). It is now at its narrowest level in two years. In general, higher relative yields tend to make a currency more attractive to hold, as expected returns are higher.

With a yield differential of more than 150 basis points (or 1.5%), holding U.S. dollars is still more attractive than holding lower-yielding currencies, all else being equal, but the advantage has declined. If the Fed were to continue lowering rates at a more aggressive pace than other major central banks, it could weaken the dollar further.

U.S. bonds currently yield more than international bonds

Central banks in most G10 countries are in rate-cutting mode, but the pace has been slower as central banks outside the U.S. deal with a mix of inflation and growth concerns. Moreover, the starting point on yields is lower outside the U.S., giving most foreign central banks less room to cut at a rapid pace. Based on the expected path of the federal funds rate suggested in the Fed's quarterly Summary of Economic Projections released in September, yield differences appear likely to tighten further, weighing on the dollar in the near term. However, the bulk of the narrowing in differentials has probably already occurred.

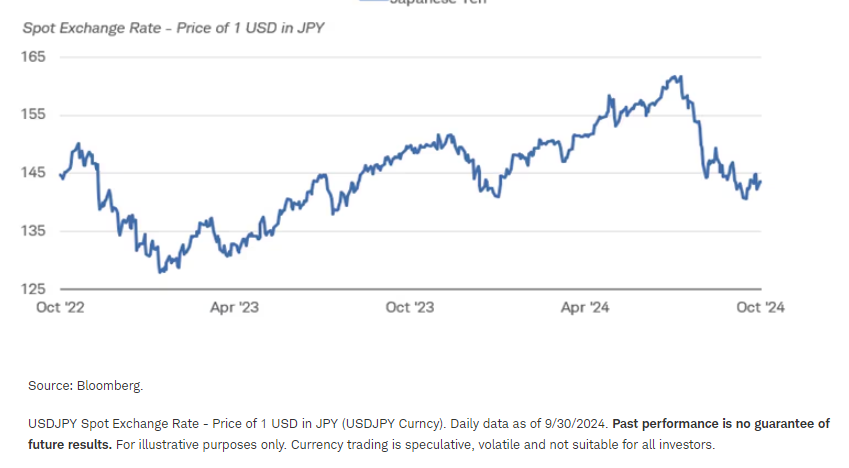

The Bank of Japan is the only major G-10 central bank that is raising interest rates. After decades at zero, the central bank has raised short-term interest rates modestly and is signaling more hikes ahead. As a major exporter of capital, Japan is a major investor in foreign global bond markets. At less than 1%, its 10-year bond yields are still low but if rates continue to move up, domestic investors may repatriate capital from abroad. Consequently, the Japanese yen has soared in the past few months, from more than 160 yen to one dollar before Japan's July 2024 rate cut to about 140 yen to one dollar currently. It would not be surprising to see the yen trade back to the 130 level.

The amount of yen required to buy one U.S. dollar has dropped sharply as the yen's value has risen

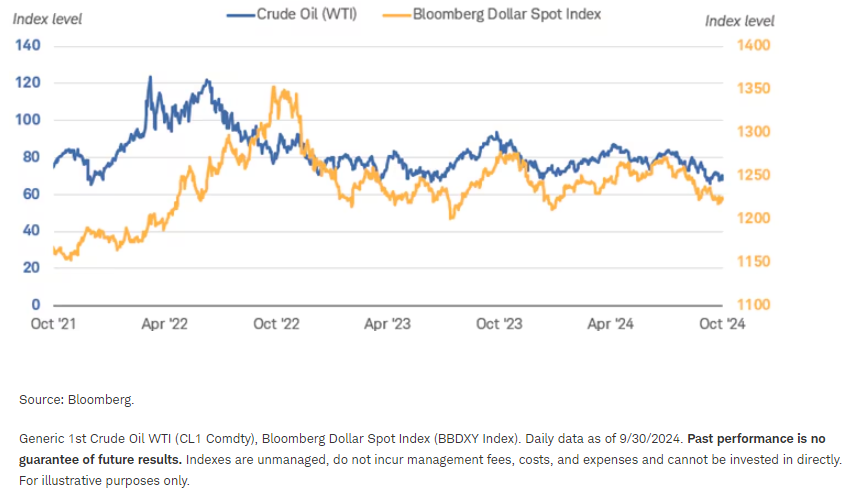

Falling oil prices might also be a drag on the dollar. As America is one of the world's major oil producers and exporters, the U.S. dollar has grown more sensitive to changes in oil prices over the last decade. There have been periods of sharp divergence, but the relationship can reflect expectations about growth, inflation, and Federal Reserve policy. Notably, the recent steep drop in crude oil prices has coincided with a drop in the dollar.

The recent drop in crude oil prices has coincided with a decline in the dollar

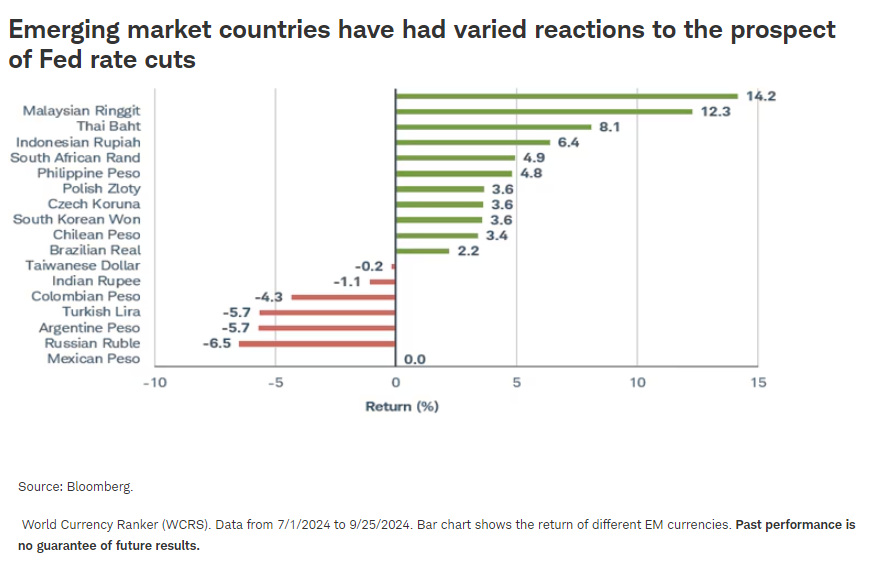

Emerging market currencies are benefiting from Fed rate cuts

In past cycles, emerging market (EM) currencies have tended to appreciate during times when the Federal Reserve was cutting interest rates. The category includes a wide variety of countries with vast differences in growth, inflation, and economic prospects. Consequently, the range of performance has been very wide.

Nonetheless, a Fed easing cycle typically raises prospects for future global growth, which benefits EM countries that rely on exporting goods and services for economic growth. Moreover, many EM countries and companies issue debt in U.S. dollars. When U.S. interest rates decline and the dollar moves lower, the debt is less costly to service.

Since the beginning of July when the Fed began to signal its intention to cut interest rates, many EM country currencies have appreciated sharply, but most are still lower than a year ago.

Assuming that the Fed continues to cut interest rates as projected, and global growth remains relatively firm, then export-oriented EM currencies may continue to appreciate. However, given the wide range of fundamental factors affecting these currencies, there will likely be wide differences in performance.

Do international bonds make sense for U.S. dollar-based investor?

With the dollar's recent decline, the performance of emerging market bonds as represented by the Bloomberg EM USD Aggregate Total Return Index has exceeded the returns on both the U.S. Agg and the Global Agg ex-US by more than 300 basis points as of September 27, 2024. Year to date, as of October 1, 2024, the total return for the Bloomberg EM USD Aggregate Index is 8.4%, with about half of the increase due to price appreciation and about half due to currency gains.

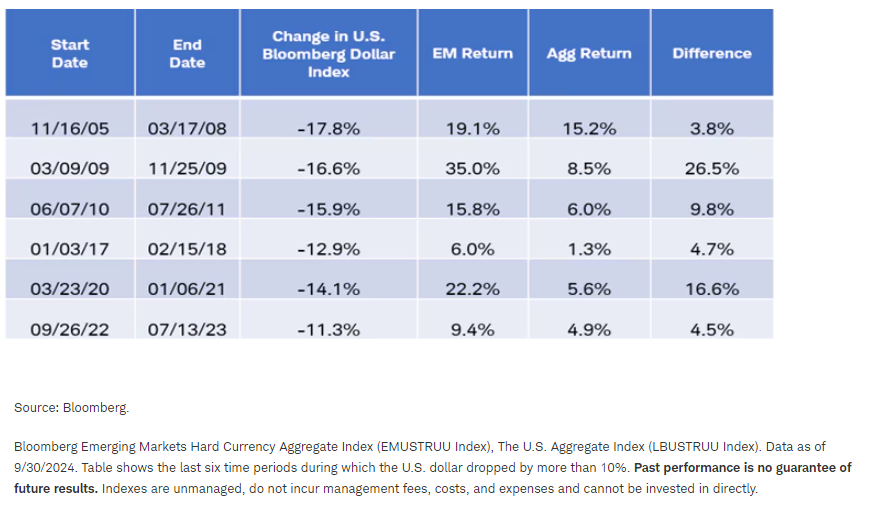

In the past, periods when the dollar was declining generally helped boost EM bond returns relative to U.S. returns. In the table below, we show periods when the dollar has been dropping by more than 10% and compare the returns of the U.S. Aggregate bond index with the returns of the EM bond index.

EM bond returns have been strong relative to U.S. bond returns when the dollar was weak

If the dollar continues lower due to faster rate cuts from the Fed than other central banks, then international bonds can potentially perform well. However, investors need to be aware that the higher returns come with much higher volatility and risk of default. We typically suggest investors limit allocation to riskier segments of the bond market to temper volatility and potential for losses.

For investors looking for some diversification who are willing to take risk, we suggest accessing international bond markets through a mutual fund or exchange-traded fund (ETF), which offer more diversification than typically available with individual bonds, and may help manage downside risks. The Schwab Mutual Fund OneSource Select List® and ETF Select List® can help you identify and research funds that may be right for you.

1 The Group of Ten (G-10) is group of 11 countries that participate in an agreement to provide the International Monetary Fund with additional funds to increase its lending ability. G-10 membership is Belgium, Canada, France, Germany, Italy, Japan, the Netherlands, Sweden, Switzerland, the United Kingdom and the United States.

Investors should consider carefully information contained in the prospectus, or if available, the summary prospectus, including investment objectives, risks, charges, and expenses. You can request a prospectus by calling 800-435-4000. Please read the prospectus carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

Currency trading is speculative, volatile and not suitable for all investors.

Supporting documentation for any claims or statistical information is available upon request.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Commodity-related products carry a high level of risk and are not suitable for all investors. Commodity-related products may be extremely volatile, may be illiquid, and can be significantly affected by underlying commodity prices, world events, import controls, worldwide competition, government regulations, and economic conditions.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Bloomberg Dollar Spot Index tracks the performance of a basket of leading global currencies versus the U.S. dollar. As of June 28, 2024, those currencies were the euro, Japanese yen, Canadian dollar, British pound sterling, Mexican peso, Chinese renminbi, Swiss franc, Australian dollar, South Korean won, Indian rupee, Singapore dollar and Taiwan dollar. It has a dynamically updated composition and represents a diverse set of currencies that are important from trade and liquidity perspectives.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

1024-WTBG

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All