Fed has kicked off an aggressive rate cutting cycle.

This should be good for the economy and stocks…

…but we think most of the decline in bond yields has likely already occurred.

The highly expected interest rate cut by the Federal Reserve (Fed) came last week, 13 months after the last rate hike that took the fed funds rate to 5.33%. While we did not believe that a 50-basis point cut was necessary, the Fed has a bias towards cutting and thus has turned the rate cutting machine on, which will stimulate the economy and likely the equity markets. Bond yields have already fallen in anticipation of this cut with 10-year yields down from 5.0% to 3.7%. We believe that bonds are fully priced and returns will be close to current yields from here. Thus, fixed income investors expecting significant price appreciation from here stand to be disappointed.

Using the Fed’s own forecast for interest rates, we get some insight into the possible timing and magnitude of future rate cuts. The Fed expects an additional 50 basis points of cuts through the rest of the year, with an additional 100 basis points of cuts coming in 2025. Inflation is falling (core CPE is 2.5%) and the unemployment rate is now above 4, both of which suggest further room to cut and so if their forecast is correct, investors would expect the fed funds rate to reach 3.375% by the end of 2025, which we believe is close to the new ‘neutral’ rate (the interest rate that neither stimulates nor depresses economic growth). If the neutral rate is roughly 3%, this leaves limited upside potential in treasuries, mortgages, and corporate bonds.

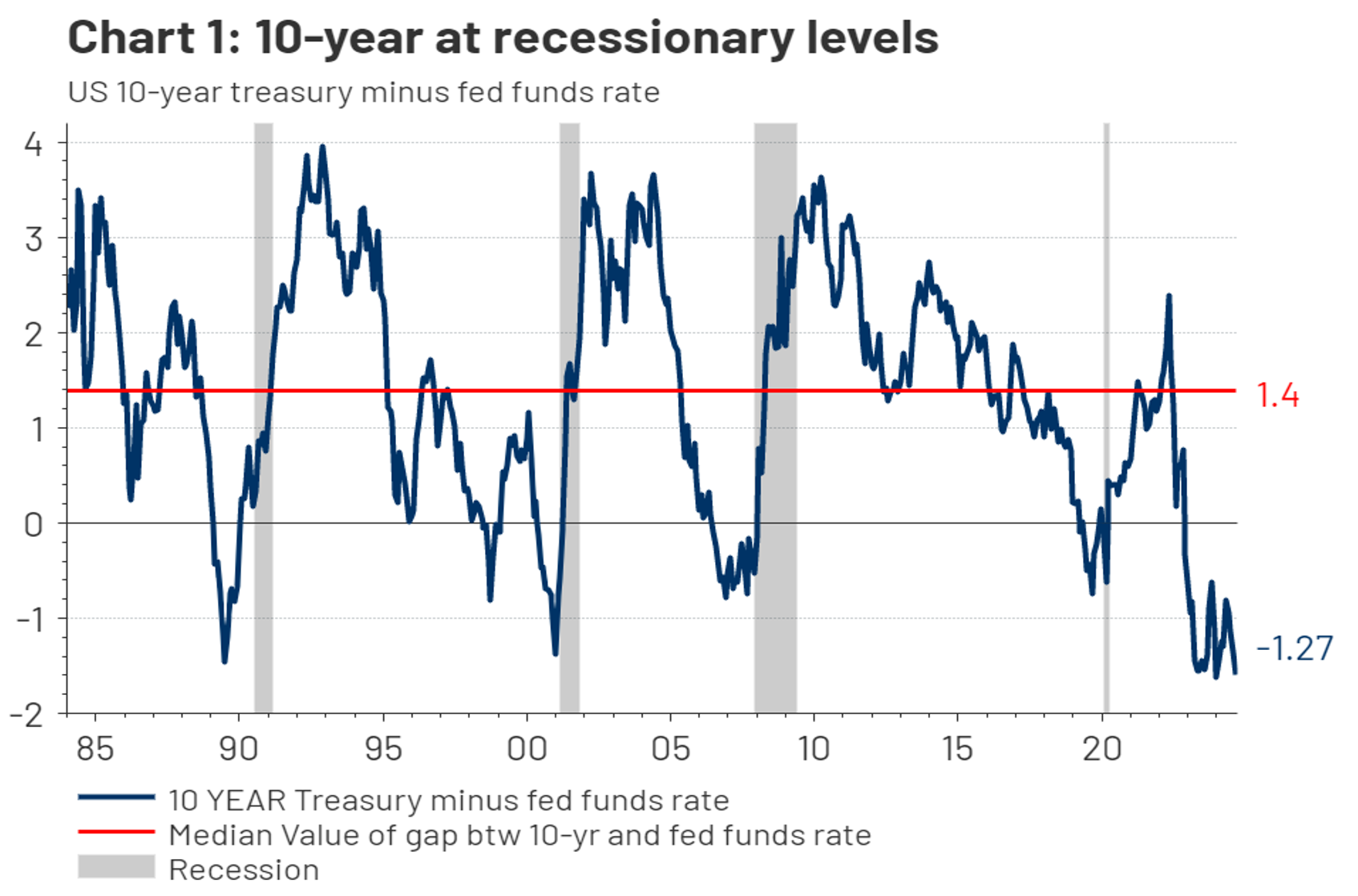

Source: LSEG Datastream, RiverFront. Data weekly as of Sept 20, 2024; gray bars indicate recession. Chart shown for illustrative purposes only. Past performance is no indication of future results.

Treasuries: Short yields fall and long yields stall - Likely to underperform without a recession. We believe that the Treasury market will experience a ‘bifurcated’ reaction to the rate cutting cycle, with short-term rates falling and longer-term rates rising. If history is a guide for what financial markets should expect over the next year, we should see two-year Treasury yields fall slightly from current levels assuming the neutral rate for fed funds is 3%. Why so little? The answer is that history has shown that yields tend to fall more in anticipation of the first rate cut. Hence, in most cases the bond market’s reaction function to actual rate cuts are muted. We think this time will be similar. Absent a recession, we see little further downside for longer term yields and only modest declines for shorter term ones.

The combination of maturities that make up the Treasury yield curve from one-month Treasury bills to the 30-year Treasury bond have been ‘inverted’ (shorter maturity yields higher than longer maturity yields) since the pandemic. We think this dynamic is set to change as the Fed normalizes yields and the yield curve returns to upward-sloping. An upward-sloping yield curve highlights the additional compensation required by investors to lend the US government money for longer periods of time. Given our investment thesis is that the US will avoid recession, and that the yield curve will return to upward sloping, we expect the 10-year Treasury yield to be higher over the next year than it is today.

Chart 1 (above) shows that the 10-year Treasury historically out yielded the fed funds rate by a median of 1.4% percentage points over the last forty years. Hence, this would imply that the 10-year should yield over 4% instead of its current 3.69% if our assumption of 3% is the correct neutral rate on fed funds. Thus, we conclude that the bond market is pricing in a recession based on the yield of the 10-year Treasury currently. If yields revert to their median relationship with fed funds (the red line in the chart), the fed funds rate would need to be around 2.5% to justify current yields.

Mortgages: Prepayments to pick up as newer mortgages are refinanced, but limited upside from here. Over the last two years, potential homebuyers were dissuaded from purchasing a home due to the higher interest rate environment. Many first-time homebuyers opted to rent instead of buying, while many existing homeowners decided to remain in their current homes to preserve their current below market mortgage rate. The lack of existing homeowners selling their homes reduced prepayments of mortgages, and thus extended the payment schedules of mortgage-backed securities (MBS). However, now that the Fed has begun cutting interest rates the fortunes of MBS will change, in our opinion. We expect prepayments to pick up some as homebuyers who bought within the last year will likely opt to refinance as rates have come down from a high on a Freddie Mac 30-year Fixed Mortgage of 7.79% in October 2023 to as low as 6.20% recently. This should help to stabilize the MBS market, but we will likely see limited spread tightening relative to Treasuries. The Fed’s rate cutting cycle may not go low enough to fully unlock the mortgage market’s potential, given that nearly 60% of homeowners have mortgage rates lower than 4%. Additionally, much like the Treasury market the MBS market has front run rate cuts.

Corporate Bonds: Not getting paid to extend: We favor maturities inside of 10 years. The corporate bond market was resilient during the Fed’s rate hiking cycle and now that the Fed has begun to cut rates, we believe the trend will continue. Corporate bonds will likely remain stable as we do not expect the economy to enter recession, and thus access to credit for the issuers should remain readily available. Given that borrowing costs will be lower due to the Fed cutting rates, corporate bonds may see a slight improvement in overall credit worthiness. However, there is very little room for additional spread tightening relative to Treasuries. Since spreads are tight and the yield curve is relatively flat for maturities shorter than 10 years, we do not see a need to extend out on the yield curve as the additional risk is not justified by the incremental return.

Conclusion: Rate cuts are good for the economy but mixed for the fixed income investor. We believe that the major sectors of the Bloomberg US Aggregate are fully priced and thus we will continue to underweight fixed income across our portfolios, since we think that the Fed rate cutting cycle will be better for the economy and for stocks. For the pure fixed income investor, the results will be mixed - they will benefit from falling rates on their short maturing bonds, while longer maturing bonds may not have the desired outcome that bond bulls are anticipating. That said, for investors looking for income, we think locking in current rates via longer-maturity bonds is still a better strategy than remaining in cash.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of ourvideos.