A highly anticipated rate cut materialized last week, with the Fed delivering an outsized 50 basis point cut. Based on the slate of data, we wrote previously that economic conditions did not warrant the jumbo rate cut, but Fed Chair Powell and the FOMC were determined not to fall "behind the curve" and be too slow to ease.

Parsing through the FOMC data release showed a divided Committee as the median "dot plot" indicated a 25 basis point rate cut at each of the next two meetings through 2024, and almost half of the committee indicated a pause at one or both meetings.

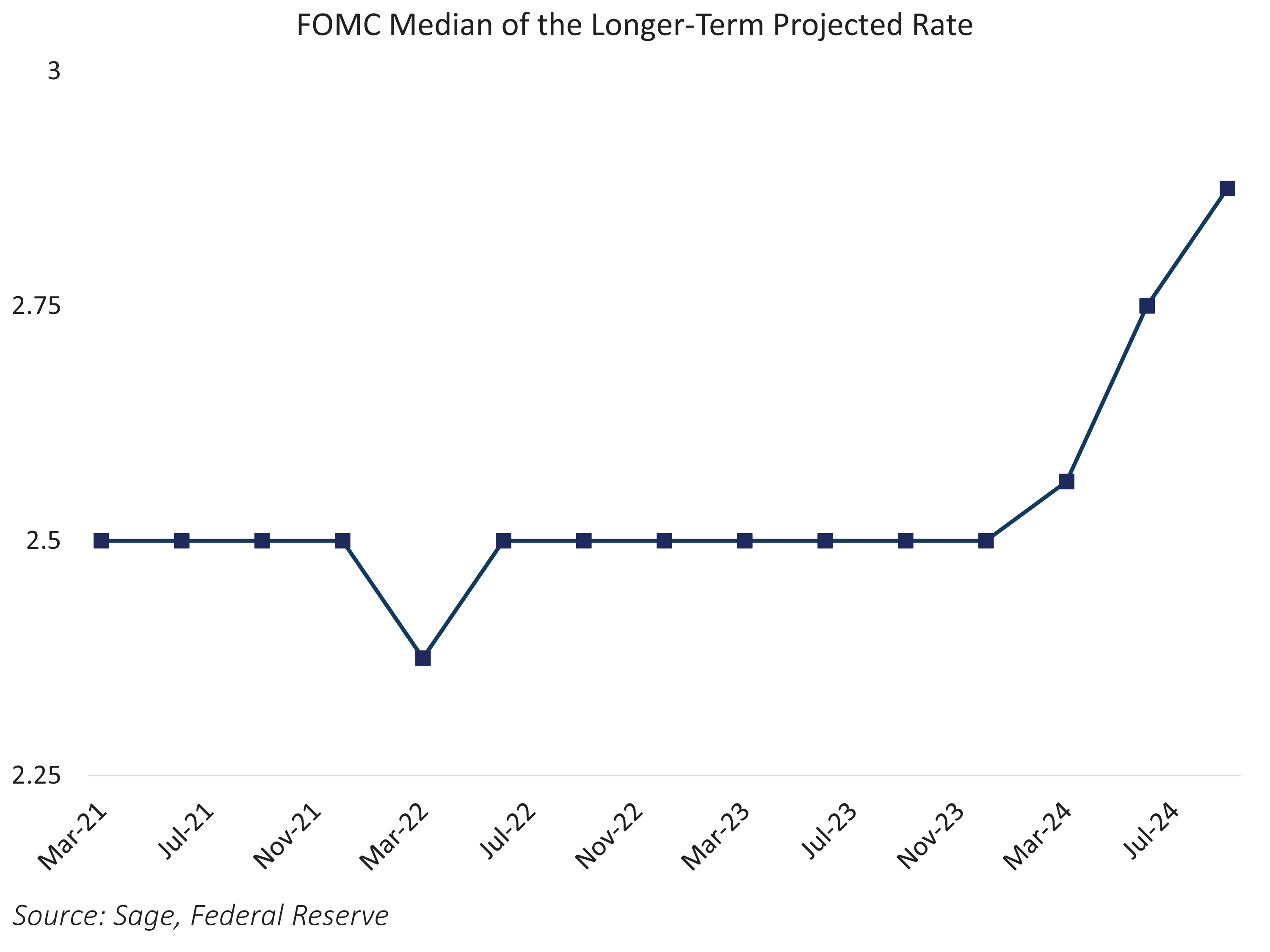

The longer-term neutral rate ticked higher to 2.875%, up from 2.75% in June and 2.5% at the start of the year. In the press conference following the decision, Chair Powell stated: "It feels to me the neutral rate is probably significantly higher than it was back then," referring to the pre-pandemic period of ultra-low interest rates.

The shallower-than-expected dot plot coupled with the notion that the long-term neutral rate is going to settle higher lifted bond yields in a rare "bear steepening" fashion, where longer-term rates rose relative to short-term rates.

The table below shows the change in market-based financial conditions following the Fed meeting. As we've written in the past, financial conditions are a collection of asset prices and interest rates that have the potential to affect the real economy. Policymakers view financial conditions as a measure of the transmission of monetary policy on the real economy.

Outside of the rise in bond yields to reflect a higher neutral rate, the market response was in accordance with an easing of financial conditions; however, it was muted relative to the magnitude of the outsized policy rate cut, which means that the policy action was expected by markets.

Financial Conditions Indicators – Change Since September 18th

| Asset |

Change |

| 2Y Treasury Yield |

0.01% |

| 10Y Treasury Yield |

0.14% |

| 30Y Treasury Yield |

017% |

| 2Y Real TIPS Yield |

-0.07% |

| 10Y Real TIPS Yield |

0.08% |

| 10Y TIPS Breakeven Inflation |

0.06% |

| IG Corporate Spreads |

-0.02% |

| HY Corporate Spreads |

-0.11% |

| DXY Index (US Dollar) |

-0.01% |

| S&P 500 |

1.50% |

Source: Sage, Bloomberg

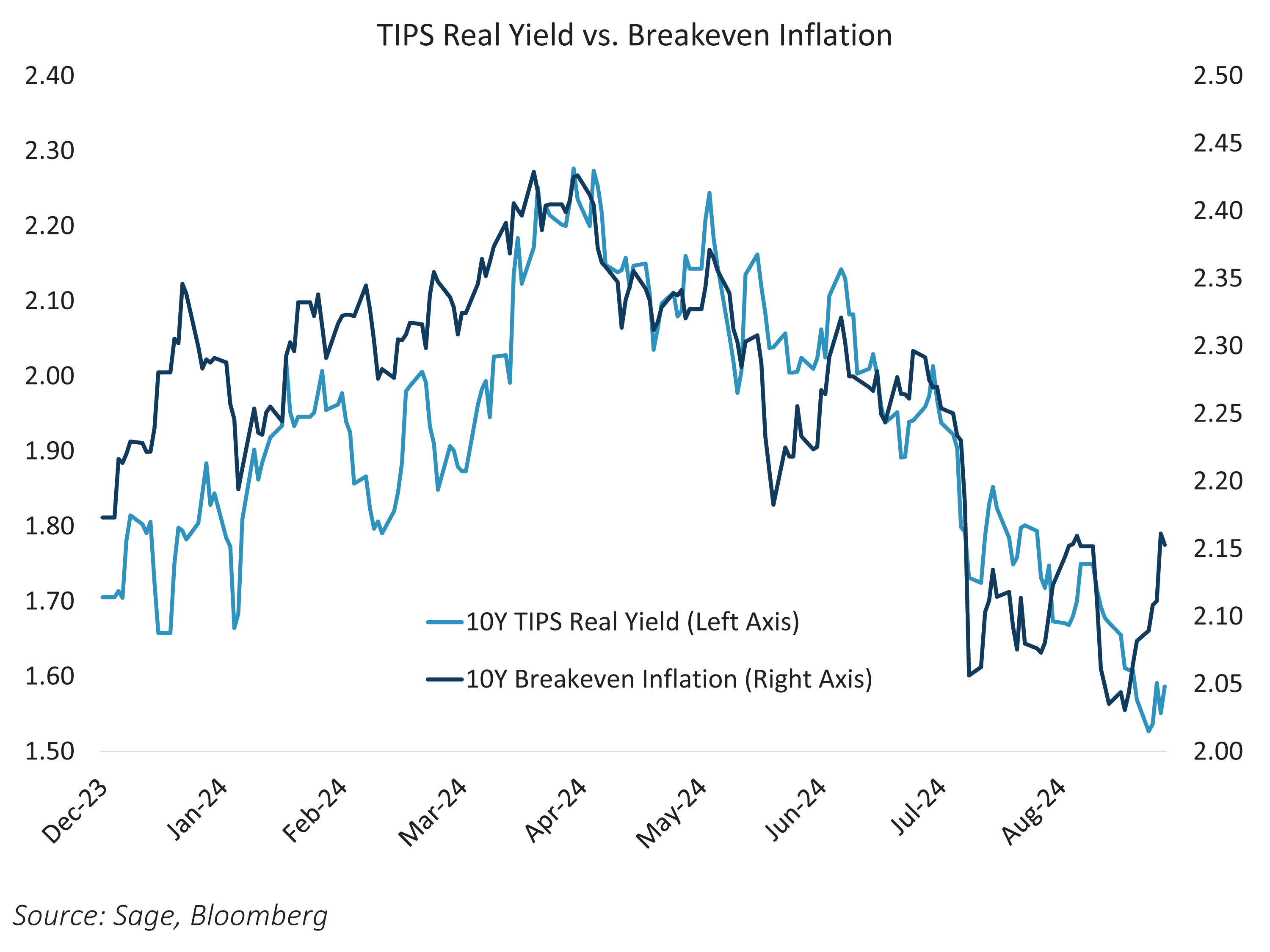

Notably, TIPS breakeven inflation expanded in response to the Fed's aggressive rate cut. Since April, real interest rates and breakeven inflation have been moving in lockstep as markets priced in disinflation coupled with an economic slowdown. The Fed cut has resulted in breakeven inflation shifting higher as the markets price in a Goldilocks growth/policy scenario in which the Fed eases into a "strong enough" economy.

Source: Sage, Bloomberg

We believe the Fed's aggressive rate cut signals a proactive stance to support a non-recessionary environment rather than responding to an imminent downturn. With financial conditions easing and breakeven inflation rising, markets seem to be embracing the Fed’s outlook for a “strong enough” economy that can sustain moderate growth without overheating. Despite the Committee’s divided views, this policy move suggests confidence in a soft landing scenario, where easing is meant to bolster the economy rather than rescue it.

Originally published September 23, 2024

For more news, information, and analysis, visit the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by Sage Advisory