Since the second quarter of the year it has become apparent that there’s been a significant deterioration in consumer sentiment in China and we have seen a growing trend among the public to downgrade the value of their spending across categories. Meanwhile, real estate challenges seemed to be getting worse; with month-on-month declines in property prices pressuring household finances. It was also becoming clear, in our view, that the government was at risk of missing its target for GDP growth of 5% for this year.

On September 24, the People’s Bank of China (PBOC) along with financial regulators announced a wide-ranging stimulus package that included interest rate cuts, more liquidity for banks, additional property reforms as well funding initiatives for the stock market.1The package was welcomed by investors. Markets on the mainland and in Hong Kong climbed, with the CSI 300 Index—a benchmark of onshore stock exchanges—recording its biggest gain since July 2020.

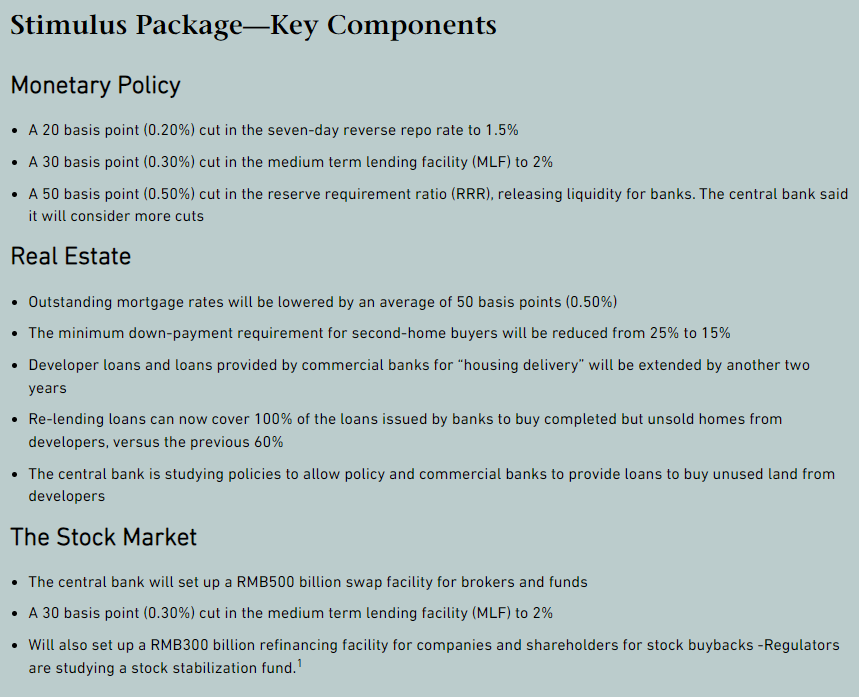

Monetary Policy

The central bank cut key lending rates and also its reserve requirement ratio (RRR), which determines the amount banks have to hold against their lending. They are significant moves. But while these changes are welcome, they are not addressing the key problem, in our view. These measures free up liquidity for the banks to lend but the challenge has been a lack of demand by consumers in the economy. The effectiveness of these measures may be limited if there's low demand for loans or if banks remain hesitant to lend. So we shouldn’t place too much emphasis on the monetary changes in this package.

The Stock Market

The government announced RMB800 billion of liquidity support for the stock market, with a RMB500 billion swap facility for brokers and funds and a RMB300 billion refinancing facility for companies and shareholders for stock buybacks. It will be available for all types of financial institutions and that will help sentiment in the local stock market. It's really a facility via the PBOC for companies and major shareholders to borrow at a very cheap interest rate to allow them to buy back stock and we know that the stock market in China is very cheap.

There will also be upcoming measures from the China Securities Regulatory Commission (CSRC) aimed at encouraging mergers and acquisitions. Taken together the measures signal a clear intent to support the stock market, which has been underperforming.

Real Estate

The property measures in the package more fundamentally address the problems in the economy. First, there is an average 50 basis points (0.50%) cut for existing mortgage rates which benefits current homeowners in China in terms of saving on their loan repayments. Second, the minimum down-payment requirement for second-home buyers will be reduced from 25% to 15%. This is somewhat of an incremental move and follows prior changes including for primary homes. Nonetheless, it is welcome as it aims to stimulate demand in an area of the property market that has been particularly struggling.

But the key measure in our view is the adjustment to the initiative announced in May which made government-backed loans available for local entities to purchase unsold housing inventory. The change will now provide 100% of the principal of bank loans for such purchases, up from the earlier announced 60%. The take-up of the earlier proposal had been poor and we think this change is significant as it doesn’t require local governments to use any of their own money to go into the market to buy the inventory. It’s a move that could potentially alleviate the oversupply problem that has been plaguing the property market. The lending facility remains at RMB300 billion but is that enough? It's obviously not sufficient to clean up all the inventory today but we think it’s more the messaging behind this that is important. It is a lot more forceful in terms of signaling what the government is willing and committed to do. We've always had that thought that this is not a matter of money. This is a matter of intent and willingness.

Sectors These Measures May Help

In the immediate wake of these announcements, financials did well mainly because of the RRR cut and existing mortgage rates coming down. The stock market-boosting measures also supported life insurers and brokers. These measures, we believe, should also help consumption and the consumption power of Chinese citizens. So in the near term, we think financials and consumer discretionary will benefit. But the package is pretty broad. Even the policies related directly to the stock market in terms of encouraging more participation by financial institutions and buybacks, that affects lots of companies, not just discretionary and financial institutions.

In Summary

In terms of the success of this package, we will have to wait and see. It would seem to us that the government is showing more determination to turn things around. For us, it is the broadest, most aggressive set of moves that we've seen in three and a half years.

We also believe that Chinese equities, despite all the macro negativity, have been priced too cheaply. We have seen earnings upgrades this year but they have not been reflected in stock market pricing. So we don't think drastic improvements in the economy are needed for the market to do quite well. Going forward, we believe a lot of these measures have the potential to aid China’s recovery and provide positive support to its equities.

Sources: 1Bloomberg, Reuters, Sept. 24-25, 2024

IMPORTANT INFORMATION

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Investing in small- and mid-size companies is more risky and volatile than investing in large companies as they may be more volatile and less liquid than larger companies. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Matthews Asia

Read more commentaries by Matthews Asia