“It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity, it was the season of Light, it was the season of Darkness, it was the spring of hope, it was the winter of despair, we had everything before us, we had nothing before us…”

-A Tale of Two Cities, Charles Dickens

The last five years have bombarded investors with a seemingly never-ending array of challenges. A once-in-a-century global pandemic, an extremely toxic political environment, the highest inflation seen in a generation, the largest European war since World War II, and the end of the “free money” era are just some of the obstacles facing investors. Yet despite all these obstacles the S&P 500 is up almost 90% as of this writing. The index ended 2019 at 3231; in July 2024 it set an all-time high of 5667.

Given the seemingly unstoppable march upwards, an investor might reasonably ask “What is the point of hedged equity? If the last five years haven’t derailed the market, what possibly could? Why not just go ‘all-in’ with the bull market?”

This paper will discuss why investors should consider investing in a hedged equity strategy during a bull market. Reasons include:

- Locking in market highs

- Hedging is cheap when investors are bullish

- Risk to the Bull Market Lurk Behind the Headlines

But before we discuss these reasons, it is important to understand what hedged equity is and what it is not.

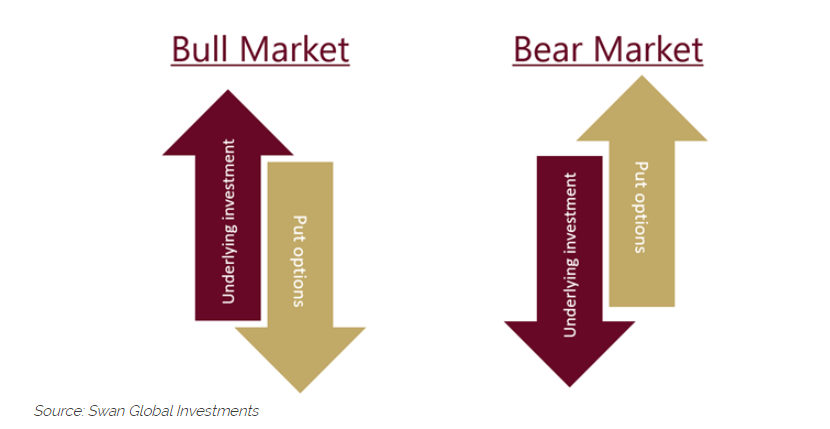

Hedged Equity is NOT Just for Bear Markets

Key to understanding hedged equity is knowing that hedged equity is not just a bear market solution. Hedged equity contains a hedge for down markets but, just as importantly, equity exposure for up markets.

The hedge usually takes the form of put options, which are inversely correlated to an asset. However, the equity allocation typically makes up the majority of a hedged equity’s portfolio. Whether the equity exposure is index-based or comprised of individual stocks isn’t important. What’s important is a hedged equity strategy has long exposure to equities, which should increase in value if the markets go up.

Hedging: Diversification 2.0

In this sense, hedged equity is just another form of the most common portfolio construction and risk-mitigation strategy available- i.e. diversification.

For decades the financial advice industry has preached the wisdom of “not putting all of your eggs in one basket” and spreading one’s investments across multiple, uncorrelated asset classes. By implementing a proper diversification strategy, the investor accepts they won’t capture 100% of the upside of the best or “hottest” asset class.

However, they hope to dampen volatility and downside risk by having a share of their portfolio invested in asset classes that do better in down markets.

Hedged equity can be seen as an advanced diversification technique. This is because put options have stronger correlation benefits than many other traditional, long asset classes.

Alternatively, if one was exclusively interested in bear markets, a hedged equity strategy probably isn’t the best option. If one was 100% convinced that markets would crash, they wouldn’t seek a solution that had balanced exposure to up and down markets.

It’s more likely they would park all their money in cash, gold, or another “doomsday” investment. If they wanted profit from a crash, they could perhaps short the market or purchase put options without a corresponding equity holding.

Unless one had perfect clairvoyance into the timing of the next market sell-off, exclusive bear market strategies are probably unwise. A balanced approach for down markets and up markets would make more sense. That said, why might an investor choose hedged equity if the market is setting all-time highs?

Active Hedge Management: Locking in Gains

If one has been riding the bull market for the last several years, it might make sense to reevaluate and “take some chips off the table.” One can reduce, but not eliminate, their market exposure by rotating to hedged equity.

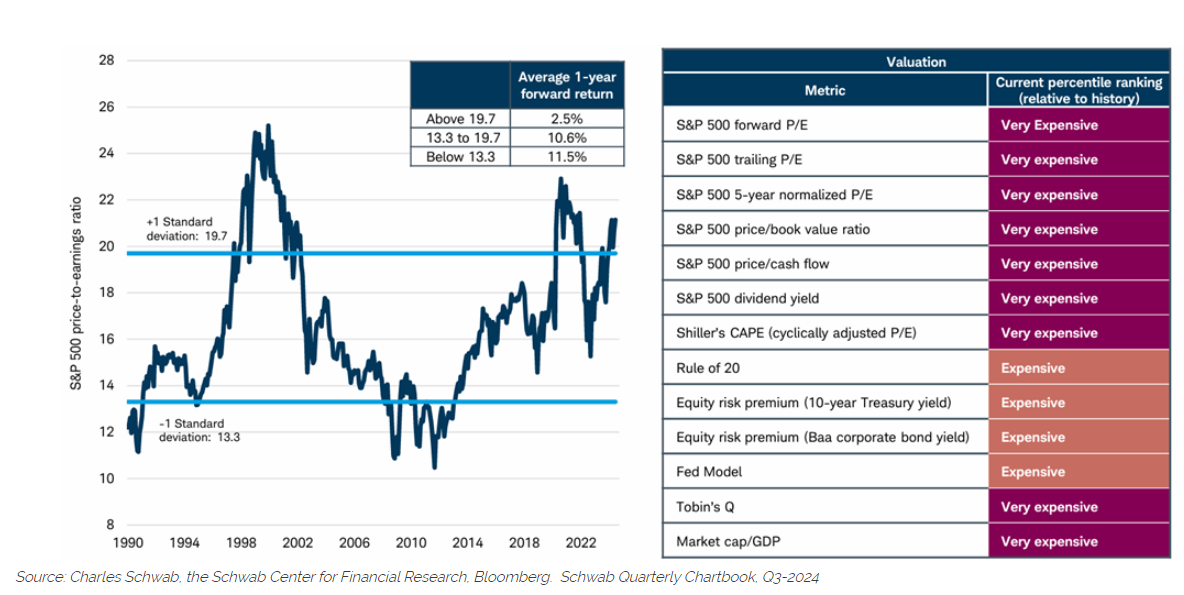

Given the state of the market, this is worth considering. The flip side of the market’s record-setting run is that valuations have become quite stretched. Depending on which metrics one chooses to analyze, US equity markets have only seen higher valuation levels twice before- just prior to the 1929 crash and during the Dot-Com Boom of 1999.

Even if a historic crash isn’t forthcoming, it is likely that at these elevated valuation levels the forward-looking returns could be muted. According to research from Charles Schwab, current S&P 500 valuation ratios are more than one standard deviation away from their long-term averages. Historically when such environments have occurred, the average 12-month forward return has been a measly 2.5%.

In short, a sober assessment of the market suggests there is more downside risk than upside potential, based on current valuations. If one is playing with “house money”, it might make sense to add a hedge to the equity.

When Hedging is Cheap? When Investors are Bullish

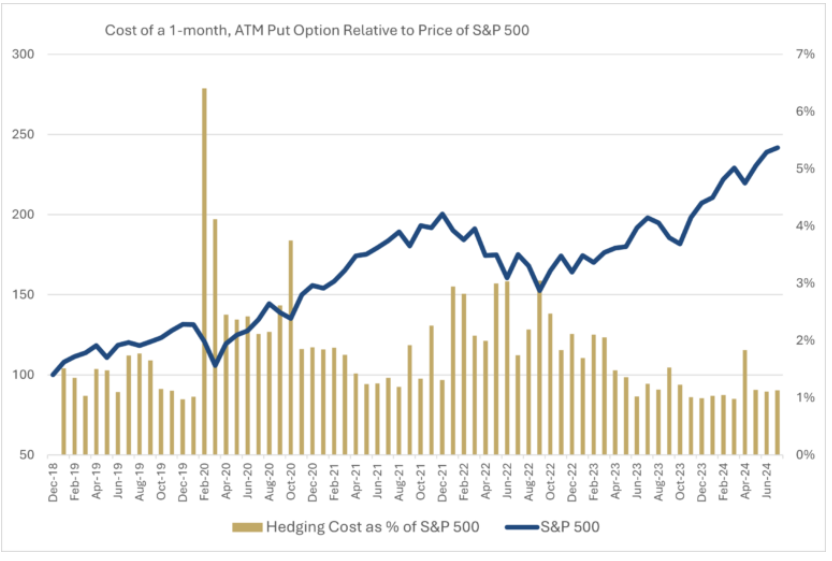

The price of put options is just like everything else in life - it is dictated by supply and demand. What drives the demand for options are the expectations or fears of a sell-off.

During docile or upward trending times in the market investors are less willing to pay for put options, and put option prices decrease.

The graph [below] compares the S&P 500 and the price of a one-month, at-the-money put option on the S&P 500 over the last five years.

The price of the option is expressed as a percentage of the S&P 500’s value. There is clearly an inverse relationship between the direction of the S&P 500 and the price of put options.

During the 2020 Pandemic and the 2022 bear market it would cost anywhere between 2.5% to 6% of the S&P 500’s value to purchase a one-month put option. During bull markets, the cost is much less. Throughout most of 2024’s record-setting run put options have been their cheapest since the Covid pandemic.

One of the golden rules of investing is to “buy low, sell high.” During bull markets it makes sense to purchase put options while they are cheap, then capitalize after a market sell-off.

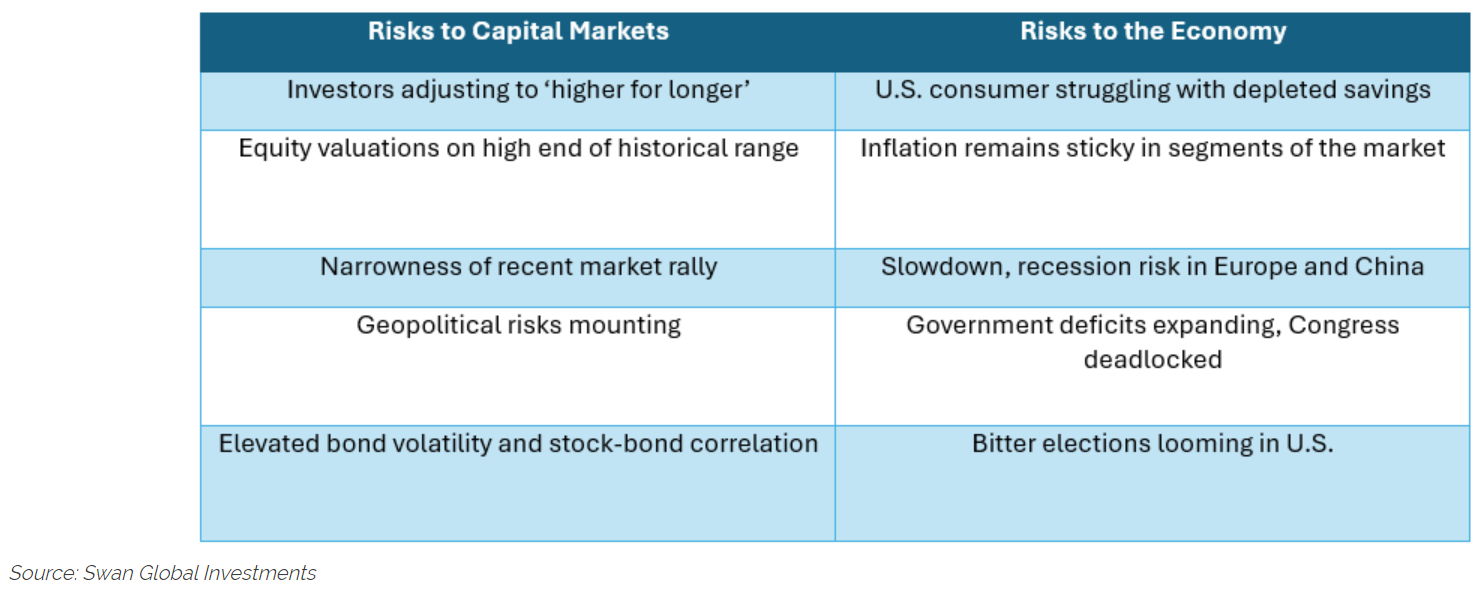

Risks to the Bull Market Lurk Behind the Headlines

Finally, investors should acknowledge that risks are ever-present in the market. Headlines and optimistic narratives have been driving the market to its all-time highs, but nothing goes on forever. A complete discussion of risks to the capital markets and the economy is beyond the scope of this short piece, but here is a summary of things that could potentially harm or end the bull market.

Moreover, long-time investors know when crises hit, they tend to be very sudden. For example, during the Covid-19 panic in early 2020 it took less than five weeks for the S&P 500 to lose over a third of its value. The shift from record highs to panic-selling was so abrupt it seems unlikely that most investors would have been nimble enough to avoid those losses. It’s better to have one’s defenses in place before, not after, a crisis hits.

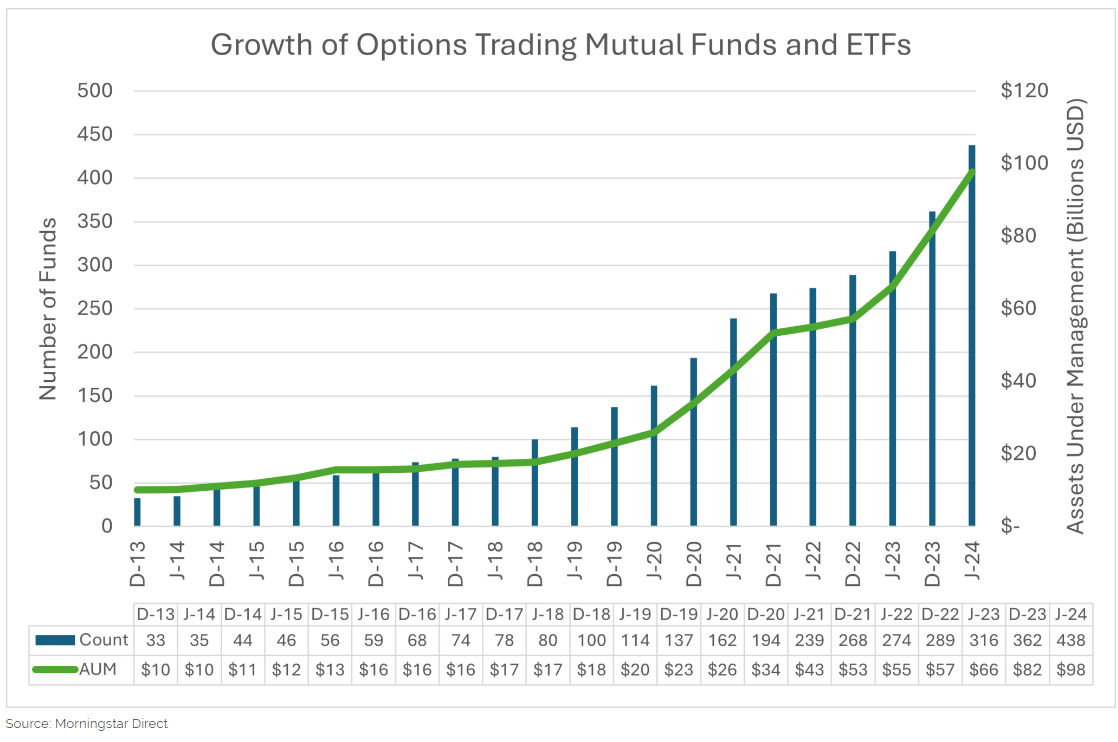

Follow the Money

The explosive growth in hedged equity products clearly illustrates there is both an understanding and an appetite for defensive investing. The number of investment products and assets under management pursuing a hedged equity approach has skyrocketed over the last several years.

The graph below shows how options-based mutual funds and ETFs have grown to almost $100bn.

Conclusion

Swan Global Investments has been an evangelist for hedged equity for decades. Long before the recent boom in options-based hedging strategies, Swan has lived by the motto, “Always Invested, Always Hedged.”

Our active approach to hedged equity seeks to mitigate the worst of down markets that can ruin a financial plan, while seeking to take advantage of major sell-offs to unlock the value of the hedge to acquire more equity shares at low prices. Combined with the active resetting higher of the hedge in upward-trending markets, investors have a strategy that also seeks to optimize upside capture for capital appreciation through full market cycles.

Having successfully weathered the Dot-Com Bust (2000-03), the Global Financial Crisis (2007-09), the Covid Pandemic (2020) and the bull markets separating those sell-offs, Swan’s hedged equity approach has demonstrated the case for active hedged equity as an all-weather investment solution.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Swan Global Investments

Read more commentaries by Swan Global Investments