Navigating the Investment Landscape: Insights and Warnings

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsHope all is well with you, my readers, and your family and friends. Here’s my latest.

NOT LOOKIN’ SO GOOD

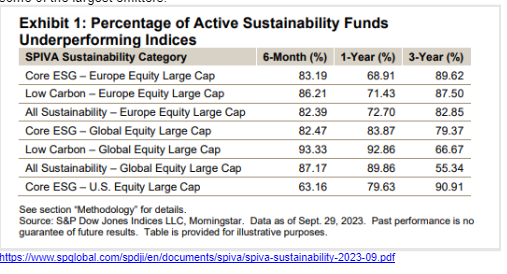

Sustainable funds (e.g., ESG funds) are investments graded using ESG (environmental, social and governance) principals or general active managers on an absolute or risk-adjusted return measures.

Asset owners around the globe have been increasing their allocations to investment strategies that incorporate sustainability considerations… Sustainability-focused active funds and indices typically have investment objectives aimed at improving their sustainability profile relative to their underlying broad equity benchmark. For example, if one of the investment objectives is to reduce carbon emissions, an active fund or index may tilt toward less carbon-intensive companies or even exclude some of the largest emitters.

I think my partner Deena’s observation is worth keeping in mind “it’s hard to spread ideals on a cracker.”

Same ‘not lookin’ so good goes for all active funds …

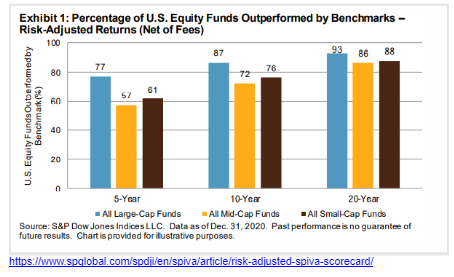

NOT SUCH A PRETTY PICTURE

FINGERS CROSSED

The Final DOL Fiduciary Rule Has Arrived. Here’s What It Means for Investors:

Needless to say, many wire houses and insurance firms are not too excited about this new rule and the legal challenges have already begun. My fingers (and toes) are crossed hoping they lose their challenges.

The Retirement Security Rule addresses investment advice made to retirement savers. Financial professionals who hold themselves out as providing individualized, reliable recommendations will be held as fiduciaries, and will have to give “prudent, loyal, honest advice free from overcharges.” According to industry firms that object to the rule, “millions of consumers will lose access to the professional financial guidance of their choice and to products and strategies to help them achieve a financially secure retirement.”

Although admittedly biased, it’s not clear to me how requiring advisors to “to give prudent, loyal, honest advice free from overcharges” will result in consumers losing access to any professional financial guidance to any products or strategies “other than those that are NOT prudent or honest or free from overcharges.” Investor savings can be astronomical.

While the rule would have potential qualitative benefits for investors (e.g., greater assurance that the financial professional sitting across the table from them is operating under a fiduciary standard when it comes to retirement account rollovers and other major decisions), analysts estimate the potential aggregate quantitative benefits for investors could save $55 billion over the next 10 years in fees (in part because plan advisors would be less likely to be able to recommend high-fee funds for plan investment menus while abiding by the new fiduciary rule), and that investors rolling over retirement account assets to purchase annuities could save another $32.5 billion during the same period.

SCRATCHING MY HEAD

I’m constantly reading articles about top performing fund managers in our professional publications and wonder why their stories never compare the fund’s performance to a low-cost ETF that invests in the same sandbox. For example, from a recent Morningstar announcement, “Morningstar Names Clare Hart (manager of the JP Morgan Equity Income Fund) “Outstanding Portfolio Manager” for 2024 U.S. Morningstar Awards for Investing Excellence.”

1 Year (5/10/2024)5 Year (5/10/2024)

JP Morgan Equity Income (OIEIX) 15.5% 57.1%

S&P 500 (IVE) 23.6% 78.8%

Go figure……

Next time you’re thinking about picking your own stock, consider who you’re competing against…

Remember, it’s not just other retail investors or even domestic investors that you’re competing with. Even an investor with $100 million portfolio is pocket change compared to institutions (and not just in the U.S.).

For example:

Government Pension Fund, Japan…. $1,381,820,000,000

National Pension Service, South Korea … $790,738,200,000

APG, Netherlands ……………………….... $552,414,500,000

Canada Pension Plan., ………………….…...$632,300,000.000

Central Provident, Singapore …………..… $580,000,000,000

California State Teachers………….……… . $337,900,000,000

And keep in mind (go back and look at the “Not Lookin’ So Good” at the beginning of my NewsLetter), the pros (average work week is 50-60 hours, credentials coming out of their wazoo and salaries range from $200m+ to million $+) don’t do so well themselves.

I’M PREJUDICED BUT THAT DOESN’T MEAN IT’S NOT TRUE

“Consumers who work with CFPs live better lives, study finds.”

“…people who work with a certified financial planner enjoy life more, have a better understanding of their finances and are more confident about their finances.”

WHO KNEW?

- A million seconds is about eleven days, while a billion seconds is just under thirty-two years.

- Hippopotomonstrosesquipedalian-phobia is the fear of long words.

CAVEAT EMPTOR

Most excellent article by Tara Siegel Bernard of the New York Times

Who Can Be Trusted for Retirement Advice? New Rules Strengthen Protections.

The regulation redefines who is considered an investment fiduciary. Before the changes, financial professionals had to meet a five-part test before they were held to that standard — and one part stated that the person making the recommendation must provide the advice on a regular basis. That means one-time recommendations were not necessarily included, which left 401(k) rollover guidance at risk…

The new rule aims to level the playing field for all financial professionals — including investment brokers and insurance salespeople — who describe themselves as trusted advisers when providing advice about your retirement money. It doesn’t matter whether they’re recommending mutual funds, stock investments, insurance products like annuities, illiquid real estate investments — it’s all covered. Investment brokers selling retirement plans to businesses would also be held to the fiduciary standard…”

What questions should I ask when choosing an adviser?

There are several, but the most important: Are you a fiduciary who promises to put my interests ahead of yours 100 percent of the time with 100 percent of my money? How do you get paid — and will you get paid more for recommending one investment over another? What’s your investment philosophy — does it involve mostly low-cost index-based investments?

https://www.nytimes.com/2024/04/23/business/fiduciary-rules-retirement-money.html

Oh, and by the way, will you sign this fiduciary pledge? If they refuse, find a new adviser who will.

This is a link to our Committee for the Fiduciary Standard who designed the “pledge”: http://www.thefiduciarystandard.org/fiduciary-oath/

MORE CAVEAT EMPTOR

Depressing if true:

Fidelity Whistleblower Claims FAs Were ‘Pressured’ to Push High-Fee Products

An ex–Fidelity Brokerage Services financial advisor has filed a whistleblower lawsuit alleging that he was fired for resisting pressure to steer clients toward higher-fee investment products.

I JUST LOVE “LONG TERM” PERFORMANCE PROJECTIONS

All of these Vanguard ETFs [all large cap GROWTH funds] have jumped at least 11.6% year to date.

Somehow 6 months doesn’t seem like a very good standard for predicting long-term performance. In addition, comparing large cap growth funds to the core S&P is akin to comparing the taste of apples to bananas.

We're nearly halfway through 2024, and the great news for investors is that the S&P 500 is on track for another strong performance. After soaring 24% in 2023, the widely followed index is up around 10.5% year to date.

However, investors could have obtained even better returns from some exchange-traded funds (ETFs). These six Vanguard ETFs are beating the S&P 500 so far in 2024.

https://www.fool.com/investing/2024/06/06/these-6-vanguard-etfs-are-beating-the-sp-500-so-fa/

MORE PROJECTIONS

https://moneywise.com/news/investing/this-famed-us-market-expert-warns-of-a-bigger-crash-than-2008

I have no idea where the claim “famed market expert” came from.

Check out some of his past prognostications…

His 2011 book (The Great Crash Ahead) goes on to suggest consumer spending will begin to plummet in 2012 with the Dow bottoming out somewhere between 3,000 and 5,600 in 2014. After hitting bottom, stocks will experience a mini-rally in 2015–2017 before falling into a final bottom during the 2019–2023 period, when the 45–50 age group troughs because the U.S. birth rate reached its own low in 1973. The Dow Jones ultimately doubled in that timeframe.

https://en.m.wikipedia.org/wiki/Harry_Dent

Dent predicted in 2011 that the Dow would have a tough 2012 and eventually crash to 3,000 in 2013; the index has not been that low since the early 1990s.

In 2012 the "Dent Tactical Advantage ETF," symbol DENT, was de-listed* having consistently under-performed the market for three years.

*https://en.m.wikipedia.org/w/index.php?title=Listing_(finance)&diffonly=true#Delisting

It's worth mentioning that this isn't new for Dent. As an October 2023 article from ThinkAdvisor noted, "For several years now, Dent has been forecasting 'the crash of a lifetime.' Now, he says, 2024 will be the year it hits — 'two years later than it should have,' according to his calculations. But 'it’s starting now,' he insists.

https://www.dividend.com/how-to-invest/10-hilariously-wrong-bullbear-calls/

RISK IS AS IMPORTANT AS RETURN

A good lesson from my friend Dr. Dorman

It's interesting that Valley Forge Capital Management … claims to be smarter than the S&P 500. .. However, the fundamentals are missing from his analysis and the article. That is the fundamental understanding of risk vs return.

If anyone is wondering what the holdings are in Friend B's portfolio, feel free to contact Dr. Dorman - he'd be more than happy to educate you on the fundamentals of investing. You can reach him at [email protected].

HOT TIP FROM SEEKING ALPHA

4 Big Dividends For Retirement In June 2024

Companies that meet these four basic requirements:

- A durable and defensive business model that will stand the test of time as well as economic and technological disruption.

- A solid investment-grade balance sheet that can support the company and its payout through thick and thin.

- A sufficiently high yield that will enable you to comfortably fund your living expenses with cash flow from your portfolio without needing too large of an initial nest egg, such that you'll have to delay your retirement for a long period of time to accumulate it.

- The prospect for dividend growth that, at least in aggregate, will meet or exceed inflation over the long term.

Using these criteria, we share four of some of the best big dividend growth stocks to fund a retirement with dividends.

#1 CHOICE

EPD excels on all four of these fronts. Its business model is definitely defensive and durable, as its energy infrastructure is strategically located, well diversified across energy asset types and geographies, and has proven to be extremely resilient by delivering stable cash flows and returns on invested capital north of 10% through all sorts of market and energy sector conditions. Additionally, with an A- credit rating from S&P and a very low 3.0 times leverage ratio, along with significant liquidity and a well-laddered debt maturity calendar, it has a very strong balance sheet.

Good story but no bananas. Current Return vs Total Return.

5 Year Return

(May 31,2024)

EPD 50.8%

S&P 500 (iShares IVV) 107.8%

https://seekingalpha.com/article/4696964-four-big-dividends-for-retirement-in-june-2024

BITCOIN

Following bitcoin news is like riding a rollercoaster without the safety bar. No shortage of predictions. As always, you need to ask yourself, if they’re so smart, why are they working for a living? Also, remember, a stopped clock is right twice a day. Here’s the latest for the last month or so.

THE OPTIMIST

Bitcoin could overtake this important price mark and continue to grow further, potentially hitting $75,245.53 by June 30, 2024, according to the advanced algorithms deployed by the crypto analytics and forecasting platform” (PricePredictions).

https://finbold.com/machine-learning-algorithm-predicts-bitcoin-price-for-june-30-2024/

If you want my personal opinion, it's $90,000 in the next month or month and a half, and then by year end we're at $130,000 [vice president of digital asset management at Marathon Digital Holdings]…Nelson [Roundtable anchor] highlighted the commonality in forecasts, noting a consensus among experts for a year-end figure ranging between $110,000 to $130,000.

Prediction: Bitcoin Will Top $100,000 in 2024

https://247wallst.com/investing/2024/03/24/prediction-bitcoin-will-top-100000-in-2024/

Quigley [venture capitalist] suggested that Bitcoin’s price could potentially increase by three or four times its current value, reaching over $300,000 if it regains the $70,000-level by 20 April…

Popular analyst Michael van de Poppe shared a similar view, with Poppe predicting a potential surge to $80,000, before the halving in April…

Rich Dad, Poor Dad author Robert Kiyosaki predicted BTC could hit $100K by September. Similarly, for BitGo CEO Mike Belshe, a conservative BTC price target of $80K was likely by May.

https://eng.ambcrypto.com/bitcoin-tether-co-founder-makes-300k-price-prediction-if-by-20-april/

The price of bitcoin may spike to $90,000 by the end of the year, with the upcoming bitcoin halving in April having marginal impact on the price of the world's leading cryptocurrency, research firm Bernstein said in a new research note.

Analysts at the firm increased their price prediction for bitcoin by $10,000, predicting a climb from $80,000 to $90,000. Bernstein expects 2025 to see bitcoin jump all the way to $150,000

$100,000 MAY BE BTC’S NEXT STOP AFTER THIS PHASE

Based on price predictions made by several crypto analysts, Bitcoin will likely climb to $100,000 once this period of consolidation is over. One of these analysts is Pseudonymous crypto analyst PlanB, who claimed that BTC hitting this price level this year is “inevitable.” Tom Dunleavy, Partner and Chief Investment Officer (CIO) at MV Capital, had also predicted earlier in the year that Bitcoin would reach $100,000 after the halving.

CLAUDE 3 OPUS

“Anthropic recently unveiled Claude 3 Opus, its new artificial intelligence (AI) model deemed a superior tool to OpenAi’s ChatGPT-4.”

“Claude AI predicts Bitcoin will trade between $120,000 and $150,000 by the end of 2024.”

https://finbold.com/claude-opus-ai-predicts-bitcoin-price-for-the-end-of-2024/

BITCOIN TO $350,000?

Bulls say the current rally is just the beginning

Lender Standard Chartered anticipates bitcoin will reach $100,000 by the end of the year. Research firm Fundstrat has a target range of $116,000 to $137,000. Hedge fund SkyBridge predicts $170,000 by April 2025.

BTC PRICE PREDICTION

Refreshing the S2F model with new data that places an average price of Bitcoin for the 2024-2028 halving cycle at $500,000, with the following cycle, 2028-2032, looking at a whopping $4 million.

In terms of Bitcoin’s price this year, the analyst has expressed confidence in the flagship decentralized finance (DeFi) asset hitting $100,000 in the second half of 2024, driven by the tendency of mining revenue to recover following the halving event, with the market peak expected in 2025.

https://finbold.com/crypto-expert-planb-reveals-when-bitcoin-will-go-vertical/

WHY BITCOIN WILL RISE TO $420,000, AND WHAT IT MEANS FOR PORTFOLIOS

AllianceBernstein says bitcoin’s price will be $150,000 by next year; JP Morgan says it will reach that price by the end of the decade, and Cathie Wood predicts $1.5 million, while Michael Sayler says bitcoin will reach $5 million.

TOO MUCH MONEY TO PASS UP

While I remain a skeptic regarding Bitcoin, the big Wall Street gorillas are jumping in with both feet. It certainly could be based on their market due diligence, but it is probably too good of a business opportunity for them to pass up.

BlackRock, the world’s largest asset manager, recently conducted a private event focused on Bitcoin, signaling a potentially transformative moment for cryptocurrency within traditional financial circles. The insights from this event were shared by Steven Lubka, the Managing Director and Head of Private Clients & Family Offices shedding light on BlackRock’s approach towards BTC and its implications for investors.

Overall, Lubka highlighted four “big ideas” that BlackRock shared during the event. The first key takeaway, according to Lubka, is that BlackRock hosted an exclusive event for its “top clients” to promote the spot Bitcoin ETF. “This supports the view that BlackRock is gearing up to use its marketing and sales machine to promote Bitcoin and their ETF product,”…

The recommendation from BlackRock’s quantitative analyst regarding portfolio allocation to Bitcoin is perhaps the biggest revelation [it certainly is to me]. Advocating for a 28% allocation to Bitcoin in an investor’s portfolio is not just a bold statement; it represents a seismic shift in how traditional investment firms view cryptocurrency’s role in asset diversification.

https://bitcoinist.com/blackrock-private-bitcoin-event/

MASSIVE RALLY WITH A CAVEAT

All things considered, numerous indicators suggest Bitcoin is in for a massive rally in the next few months, perhaps even surpassing the $200,000 price point and proving the expert right. However, it is important to keep in mind that things in this sphere can change on a whim, so caution is warranted.

https://finbold.com/bitcoin-on-parabolic-trajectory-on-track-to-hit-200k-soon/

AI PREDICTIONS

ChatGPT-4o predicts Bitcoin’s price if NYSE approves BTC trading

ChatGPT-4o believes in a 20% to 30% price increase following the recent announcement as an immediate reaction. This would put Bitcoin at $82,000, which aligns with a reported analysis on Finbold from a veteran cryptocurrency trader.

Second, OpenAI’s flagship product is expected to be priced between $100,000 and $120,000 in the mid-term. This is considering the combined effect of new investor inflows, increased legitimacy, and broader acceptance within six to 12 months.

Finally, the long-term BTC price prediction puts the leading cryptocurrency in a price range between $150,000 to $200,000.

https://finbold.com/chatgpt-4o-predicts-bitcoins-price-if-nyse-approves-btc-trading/

AND THE WINNER IS FOR THE MOST OPTIMISTIC PREDICTION

BITCOIN COULD SOAR 5,453% BY 2030

Ark Investment Management and its tech-investing leader, Cathie Wood, believe Bitcoin is destined to go much higher. Ark's research suggests the cryptocurrency could soar 2,115% to almost $1.5 million by 2030—but Wood herself came out with an even more bullish estimate recently, saying Bitcoin could rocket 5,453% to $3.8 million.

https://www.fool.com/investing/2024/06/01/bitcoin-could-soar-5453-2030-cathie-wood-realistic/

THE NEXT RICHEST MAN IN THE WORLD

How this crypto trader turned $50 into $11,000 in two hours.

“A cryptocurrency trader turned $50.98 into approximately $10,900 in two hours, speculating in a recently created token.”

Forget a few hours, give him a week. His $10,900 would be worth about $23 million, a week later $48 BILLION! Imagine what he’ll be worth in a year. It’s amazing what a little compounding can do (21,000%).

Bezos, Musk Zuckerberg, Ellison and Buffett plan on stepping aside pretty soon. It won’t be long before he makes them look middle class.

https://finbold.com/how-this-crypto-trader-turned-50-into-11000-in-two-hours/

THE PESSIMIST: I AM WORRIED

Fed president issues ‘incredible’ bitcoin price prediction amid shock inflation warning

"You already said on record that you have an unlimited supply of dollars, doesn't it make sense to trade some of them in for a currency with a hard cap," Jennifer Ablan, editor in chief of Pensions & Investments, asked Kashkari during a LinkedIn Live event on behalf of an audience member and referring to bitcoin's fixed supply of a 21 million bitcoin. "What is that hard cap," Kashkari, the president of the Federal Reserve Bank of Minneapolis, responded. "The hard cap could be zero for bitcoin, it could go down to zero. Just replace the word bitcoin with Beanie Babies. Should the Fed buy Beanie Babies, because Beanie Babies were a fad for a while?"

Kashkari said that like Beanie Babies, bitcoin has "no actual utility in the economy, other than being a nice toy that some people enjoy owning and trading," adding the only use for bitcoin is "trying to subvert banking regulations, get around either marijuana banking or illicit activities."

WILL 'GO TO ZERO SOMEDAY

Veteran investor Jim Rogers, who co-founded the Quantum Fund with billionaire investor George Soros, expects all cryptocurrencies, including bitcoin, to disappear someday. Anticipating bitcoin going to “zero,” he stressed: “I’m very skeptical of crypto. I don’t expect it to last … I do not see any long-term value in cryptocurrency.”

AS I CLOSE OUT THIS ISSUE

On 7/4 at 2PM, bitcoin was trading at $58,056.53

Important Disclosure Information

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Evensky & Katz/Foldes Wealth Management [“EKF]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from EKF. EKF is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of the EKF’s current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.evensky.com. Please Remember: If you are a EKF client, please contact EKF, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your EKF account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your EKF accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Note: Limitations: Neither rankings and/or recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any professional designation, certification, degree, or license, membership in any professional organization, or any amount of prior experience or success, should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if EKF is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (see link as to participation criteria/methodology, to the extent applicable). Unless expressly indicated to the contrary, EKF did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of EKF by any of its clients. ANY QUESTIONS: EKF’s Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Evensky & Katz / Foldes Financial Wealth Management

Read more commentaries by Evensky & Katz / Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All