High-yield bonds have been one of the best-performing bond investments this year, but we continue to maintain a neutral view on the asset class. Investors with long-term investing horizons and who are willing to ride out the ups and downs can consider high-yield bonds, but from a tactical standpoint there may be better entry points down the road. With the economy showing signs of slowing down, it's important to highlight the risks that slower growth—or worse, a recession—could pose to the high-yield bond market.

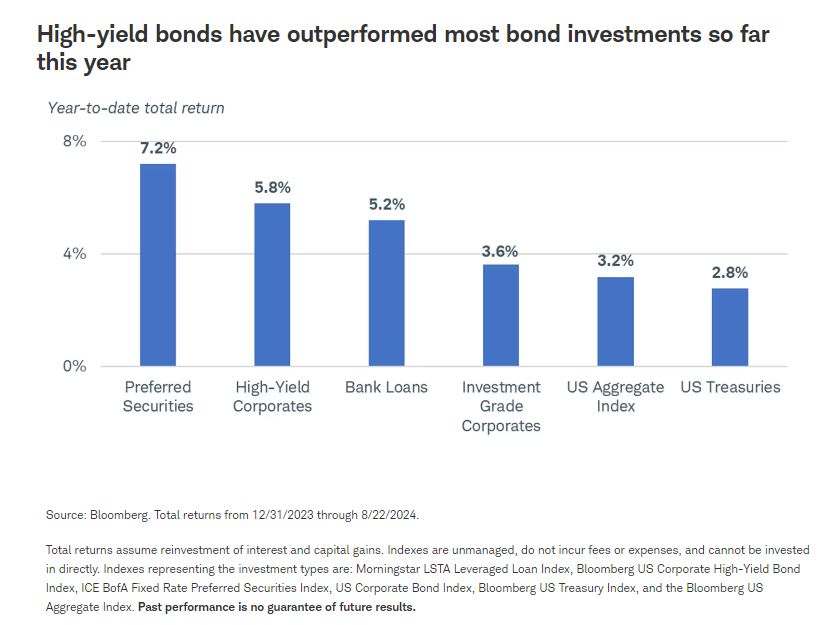

Despite those risks, performance has been positive lately. High-yield bonds have generally outperformed high-quality investments like U.S. Treasuries, investment-grade corporate bonds, and the overall US Aggregate Index this year, but that pace of outperformance may be difficult to replicate going forward.

Yields are high, but risks remain

With the economy showing signs of slowing down, investors should be aware of the risks that a decline in economic growth, or an outright contraction, could pose to the high-yield bond market. While a near-term recession is not our base case, risks are rising. The labor market has continued to come into balance, with August's jobs report weakening much more than expected; consumer confidence remains relatively low; and the leading economic index has continued to suggest a weakening economy. The triggering of the "Sahm rule" with the July U.S. employment report, suggesting we're in a recession, also has grabbed headlines.1 We'll only find out after the fact once we're officially in a recession, but these indicators support our "up in quality" bias with fixed income investments. Below we'll lay out what investors need to know about high-yield bond investing today.

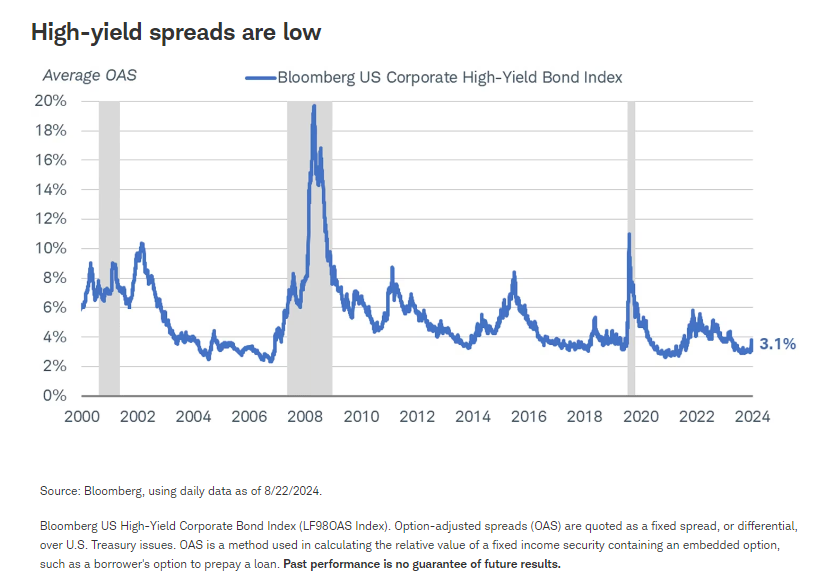

The yield advantage that high-yield bonds offer above comparable Treasuries—known as a "spread"—is low. At just 3.1%, the average spread of the Bloomberg US Corporate High-Yield Bond Index isn't far off its cyclical low and is well below its since inception average of almost 5%.2 In fact, spreads have only been 3.1% or lower just 11% of the time since August 2000. With spreads so low, investors simply aren't being compensated very well to take outsized risks today.

During recessions, as the gray columns below indicate, or during periods of general market volatility, high-yield spreads tend to rise sharply. That can be painful for high-yield bond investors because rising spreads pull down the prices of high-yield bonds relative to Treasuries. That also means there may be better entry points down the road to tactically add to positions.

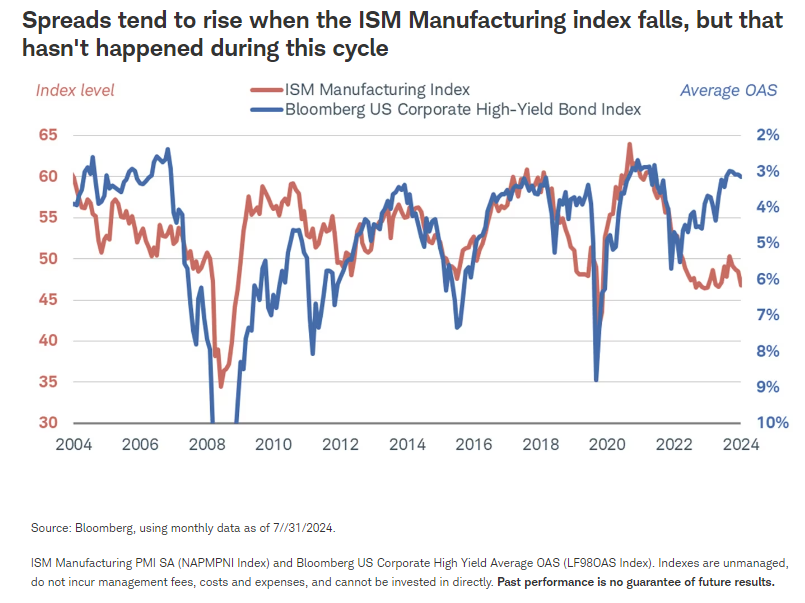

Other indicators suggest spreads should be higher as well. Historically, there tended to be a relationship between the trend in the ISM® Report On Business® Manufacturing index and the spread of the Bloomberg US Corporate High-Yield Bond Index. The ISM manufacturing index is based on a survey of manufacturers and tends to be an indicator of monthly economic activity—a reading above 50 represents expansion and below 50 represents a contraction. Through July 2024, the index has been below that 50 reading for 20 of the last 21 months.

Historically, when that index has declined spreads have risen; the blue spread line is inverted in the chart below. Instead, spreads remain near cyclical lows while the ISM Manufacturing index is flashing warning signs about the economy.

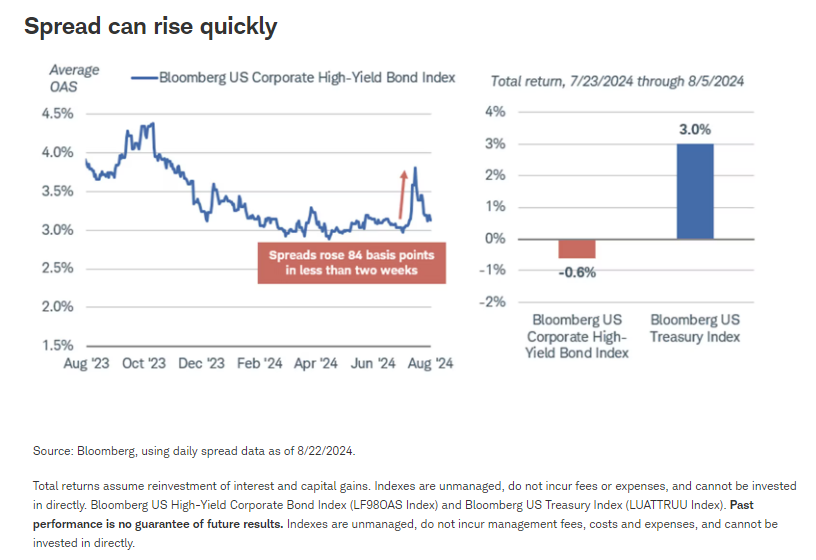

Spread increases can happen fast. We saw this a few weeks ago when concerns about the unwinding of the yen carry trade (borrowing at very low interest rates in Japan and investing in assets with higher expected return) sent risk assets sharply lower. The average spread of the Bloomberg US Corporate High-yield Bond Index rose by 84 basis points (0.84%) in less than two weeks. As bond prices and yields move in opposite directions—and because spread is a component of yield—that pulled prices down relative to Treasuries.

The chart below compares the performance of the high-yield index with the Bloomberg US Treasury index, highlighting the impact of rising spreads on total returns. Keep in mind this was a small sample size of just nine trading days, and spreads have since fallen again, pulling high-yield prices back up. But if spreads were to rise by a larger amount, like a 300-basis-point increase or more, which has occurred in the past, the negative impact could be much larger.

Finally, high-yield issuer fundamentals should deteriorate if the economy slows. At a very high level, U.S. corporate fundamentals have remained strong despite the aggressive Federal Reserve rate hikes and accompanying rise in borrowing costs. In aggregate, corporate profits are high and the amount of liquid assets held on corporate balance sheets continues to hit new record highs.

But "aggregate" numbers aren't necessarily indicative of high-yield issuers. High-yield issuers have those high-yield ratings for a reason, and it's usually due to a high level of debt relative to earnings. With high debt levels, rising borrowing costs tend to sting high-yield issuers more than their investment-grade counterparts.

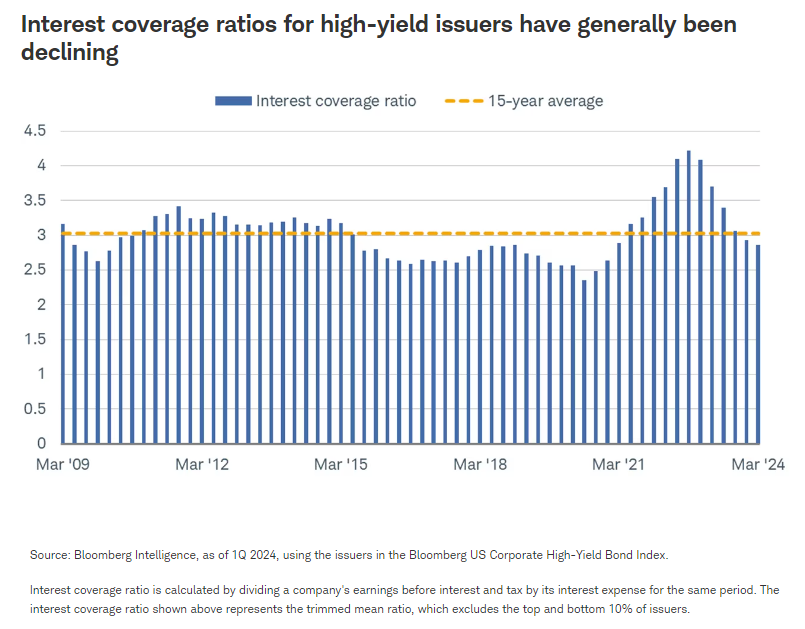

Interest coverage ratios are an indicator of corporate health, measuring an issuer's earnings before interest and taxes relative to its annual interest expense. In short, it shows how capable an issuer may be to make timely interest payments. The average interest coverage ratio of the issuers in the Bloomberg US Corporate High Yield Bond Index has declined for six straight quarters and is now below the 15-year average. Digging deeper shows a more worrisome trend, as many companies aren't earning enough to pay off that interest expense. Roughly one third of the companies in the Russell 2000 stock index are what are sometimes described as "zombie companies," or those whose three-year average earnings before interest and tax is lower than the average annual interest expense. Corporate profit growth could slow should the economy slow more than expected, making it more difficult for many issuers to make timely interest payments.

Investors can still consider high-yield bonds in moderation

Despite the rising risks and low spreads, investors don't need to abandon or avoid high-yield bond investments. Rather, we suggest that investors who are considering high-yield bonds today should understand those risks and have a more long-term investing time horizon to ride out the potential ups and downs.

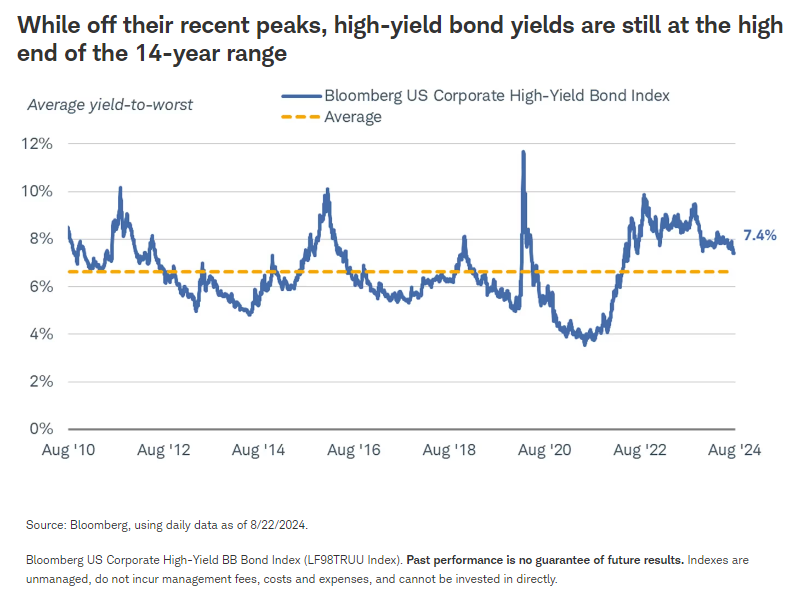

While spreads are low, the yields that high-yield bonds offer are still high. Much of that has to do with the level of Treasury yields, but average yields of 7% or more are still above the recent post-financial crisis average.

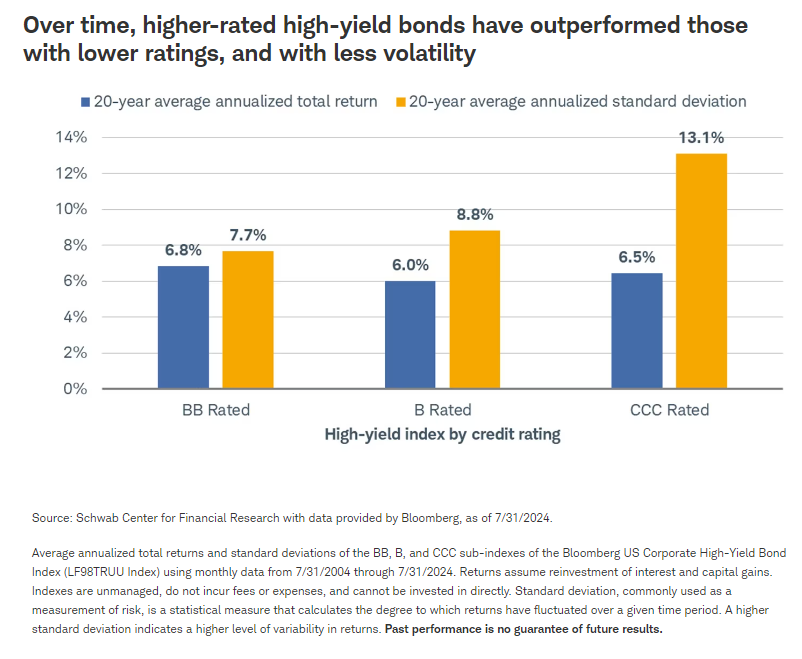

Our "up in quality" focus can apply to high-yield bonds as well. Corporate bonds rated B and CCC tend to have the highest default rates over time, so we prefer high-yield bonds rated BB today. While we prefer a defensive approach to high-yield bonds for now, over time BB rated bonds tend to outperform B and CCC rated bonds, and with less volatility.3

What to do now

Slower economic growth and rising recession risks make us a bit cautious on high-yield bonds over the short-run. It usually makes sense to take risks if you're compensated well, but that's not the case today with spreads so low.

Long-term investors willing to ride out the ups and downs can still hold high-yield bonds (or bond funds) in moderation considering yields are still north of 7%. However, there may be better opportunities down the road should economic growth slow—or worse, a recession hits—pulling spreads to a more attractive level.

1 The Sahm rule, created by economist Claudia Sahm, states that the U.S. economy is likely in recession when the three-month average of the unemployment rate rises by at least a half-percentage point above its low during the previous 12 months.

2 Average spread of the index from January 1994 through August 2024 was 4.92%. using monthly data.

3 The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

Investors should consider carefully information contained in the prospectus, or if available, the summary prospectus, including investment objectives, risks, charges, and expenses. You can request a prospectus by calling 800-435-4000. Please read the prospectus carefully before investing.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness, or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results, and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal. International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Supporting documentation for any claims or statistical information is available upon request.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Preferred securities are a type of hybrid investment that share characteristics of both stock and bonds. They are often callable, meaning the issuing company may redeem the security at a certain price after a certain date. Such call features, and the timing of a call, may affect the security's yield. Preferred securities generally have lower credit ratings and a lower claim to assets than the issuer's individual bonds. Like bonds, prices of preferred securities tend to move inversely with interest rates, so their prices may fall during periods of rising interest rates. Investment value will fluctuate, and preferred securities, when sold before maturity, may be worth more or less than original cost. Preferred securities are subject to various other risks including changes in interest rates and credit quality, default risks, market valuations, liquidity, prepayments, early redemption, deferral risk, corporate events, tax ramifications, and other factors.

Bank loans typically have below investment-grade credit ratings and may be subject to more credit risk, including the risk of nonpayment of principal or interest. Most bank loans have floating coupon rates that are tied to short-term reference rates like the Secured Overnight Financing Rate (SOFR), so substantial increases in interest rates may make it more difficult for issuers to service their debt and cause an increase in loan defaults. A rise in short-term references rates typically result in higher income payments for investors, however. Bank loans are typically secured by collateral posted by the issuer, or guarantees of its affiliates, the value of which may decline and be insufficient to cover repayment of the loan. Many loans are relatively illiquid or are subject to restrictions on resales, have delayed settlement periods, and may be difficult to value. Bank loans are also subject to maturity extension risk and prepayment risk.

Small-cap stocks are subject to greater volatility than those in other asset categories.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The information and content provided herein is general in nature and is for informational purposes only. It is not intended, and should not be construed, as a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own professional tax and investment advisors or other professionals (CPA, Financial Planner, Investment Manager) to help answer questions about specific situations or needs prior to taking any action based upon this information.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or 'Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

0824-MXF4

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Charles Schwab

More Emerging Markets Topics >