Across Europe, ruling parties are under pressure. Bond investors should stay active and invested, in our view.

Europe’s voters are rejecting the status quo. On July 4, UK electors handed the Conservative government the worst defeat in its history. The incoming Labour government won a huge majority and—happily for bondholders—is committed to balancing the UK’s budget over time.

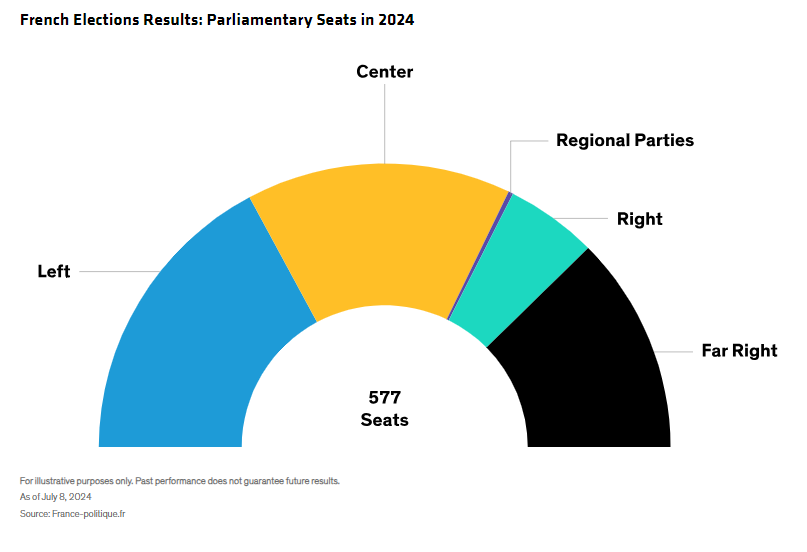

The final vote in France’s parliamentary elections on July 7 saw another defeat for the incumbent, President Emmanuel Macron’s centrist Renaissance party. However, this time there was no outright majority (Display), no immediate prospect of a stable coalition—and no clear route to managing France’s deficit.

Source: France-politique.fr

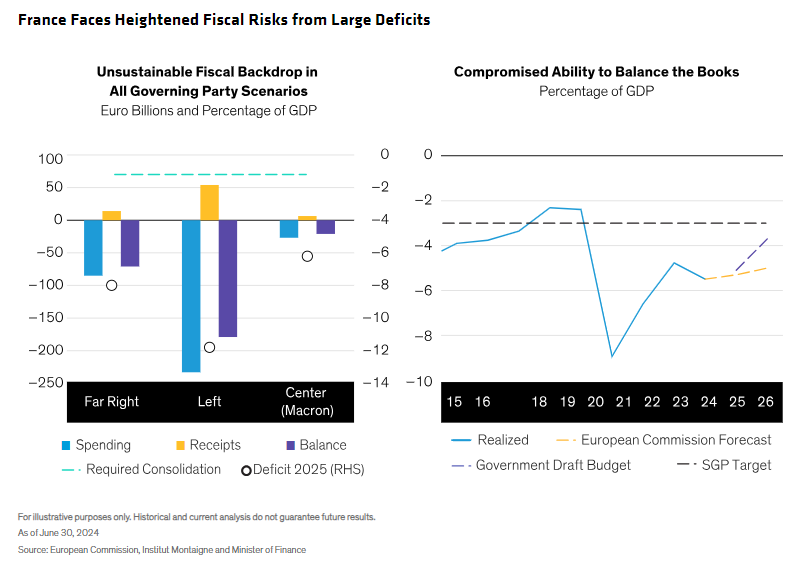

That’s a problem, considering that France’s deficit exceeds the European Union (EU) Stability and Growth Pact (SGP) limit, which triggered corrective action recently via the European Commission’s (EC’s) Excessive Deficit Procedure (EDP). In the final parliamentary election vote, parties of the left and far right were unable to break through, averting the worst-case outcome for markets, given that budget strains could have intensified. But we think France remains on an unsustainable financial course (Display), facing a politically uncertain and volatile period. That’s worrisome for the EU, because France’s economy is the second largest of the member states.

A Bumpy Path Lies Ahead

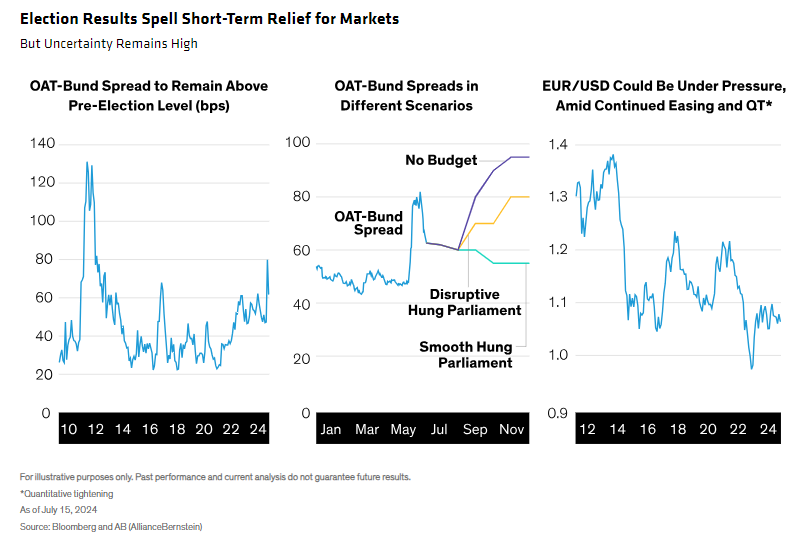

Markets reacted to the results by pushing spreads on French sovereign bonds (OATs) up to 80 basis points above German Bunds, the widest level since the European sovereign debt crisis of 2010. Spreads later narrowed slightly to the current level of around 65 basis points. Franco-Bund spreads will likely stay volatile, given several political uncertainties:

- While the new Parliament officially convened on July 18, the old government will remain in place for the time being, albeit with no legislative powers.

- If and when a coalition emerges, major legislation is unlikely to pass in the next Parliament; however, Macron could dissolve the Parliament again next summer.

- The risks of France leaving the EU (popularly labelled “Frexit”) remain low, but could increase if momentum behind the far-right National Rally party continues to strengthen.

- Several EU countries—including Italy—are also running excessive fiscal deficits and face EDP actions. If markets lose faith in the French government’s ability to reduce the deficit, OAT spreads could widen further, threatening to make France’s debt dynamics unsustainable and creating further instability across euro-area deficit countries.

- The European Central Bank (ECB) could, in theory, step in to help beleaguered euro-area governments by activating the Transmission Protection Instrument (TPI), which is designed to calm markets by purchasing euro sovereign bonds. However, the TPI wasn’t intended to include countries that face EDP action—an obstacle that could delay intervention and increase contagion risks across the eurozone.

- Considering further election uncertainties and the small probability of much-needed fiscal deficit reduction, rating agencies are likely to have a less favorable outlook on French sovereign bonds. If that outlook is downgraded further in autumn, it could push OAT spreads wider.

- Potential hot spots include the submission of France’s five-year budget plan to the European Commission (due at the end of September) and the parliamentary vote on the bill for the 2025 budget (probably in October or November).

Volatility Could Spell Opportunity for Active Investors

For active bond managers—particularly those with multi-sector, multi-regional strategies—volatility may create new relative-value opportunities.

For instance, the surprise result of the French elections widened the spread of OATs over Bunds to a level that was unlikely to be sustained, presenting an opportunity for investors to trim their Bund holdings in favor of OATs. It also highlighted a value opportunity in Spanish government bonds, which in our view have much better fundamentals, were trading attractively versus OATs and have outperformed since the election.

Going forward, we still see value in corporate bonds of multinational companies that sold off post-election, where we think the impact of French politics has been overdiscounted. Likewise, we think French bank bonds likely represent an opportunity too.

We also continue to favor European investment-grade credit bonds, which were caught up in the post-election sell-off. They offer attractive yields in a higher-for-longer rate environment, and we expect their default risk to remain very low. They may also enjoy capital gains, as the ECB resumes rate cuts later this year. By contrast, we think the weakest CCC-rated credits remain vulnerable.

For UK investors, the new government’s commitment to following the fiscal compact suggests that the longest-term gilts could be undervalued. We believe that the risk premium embedded in the long end of the UK yield curve (highlighted by its relative steepness versus other markets) will likely decline, favoring the 30-year segment over the 10-year segment.

Risks Look Contained—for Now

Given the absence of Frexit risk, the recent French parliamentary elections seem much less risky for corporate credit than were the presidential elections of 2017, as this time very few sectors faced immediate threats.

In the year ahead, political stability is likely to remain fragile in France. We think French sovereign bond spreads are unlikely to return to their pre-election levels—but other euro sovereign bonds should recover. ECB rate cuts will support European bonds generally, and we expect euro sovereign bonds that trade with a yield spread to Germany to remain attractive to investors.

From a credit perspective, we believe the election result neutralizes several European credit risks, and we expect spreads to grind tighter given strong summer technical factors and benign underlying fundamentals. European credit is still attracting inflows, yields remain mostly unchanged year to date and supply is drying up given the earnings-season blackout. We expect to see more value opportunities arise as political developments trigger intermittent sell-offs, and we think investors will likely find attractive yield opportunities in the months ahead.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: Join us on July 25 for the Q3 Fixed Income Symposium, where advisors will gain insights into essential fixed income strategies and market trends to navigate 2024's challenges.

© AllianceBernstein

Read more commentaries by AllianceBernstein