The middle of the year is a time to wait for the seeds planted in the spring to reach full fruition. Patience is a key ingredient during the long, hot days of summer.

While some central banks have planted the seeds of easier policy, others are remaining patient. Growth, underlying price pressures and wage developments have all come in firmer than expected in the West, while activity remains soft in Asia. The path of interest rates across markets remains data dependent.

Elections are a risk in an otherwise positive growth backdrop for major economies. Markets are bracing for adverse outcomes as France, the U.K., and the U.S. head to polls in the months ahead. The outcomes so far in 2024 are pointing at a difficult cycle for incumbents.

The European Central Bank (ECB) made its first rate cut in June. This month's edition focuses on the circumstances that led to that decision, and what the ECB will consider to gauge its next steps.

Eurozone

-

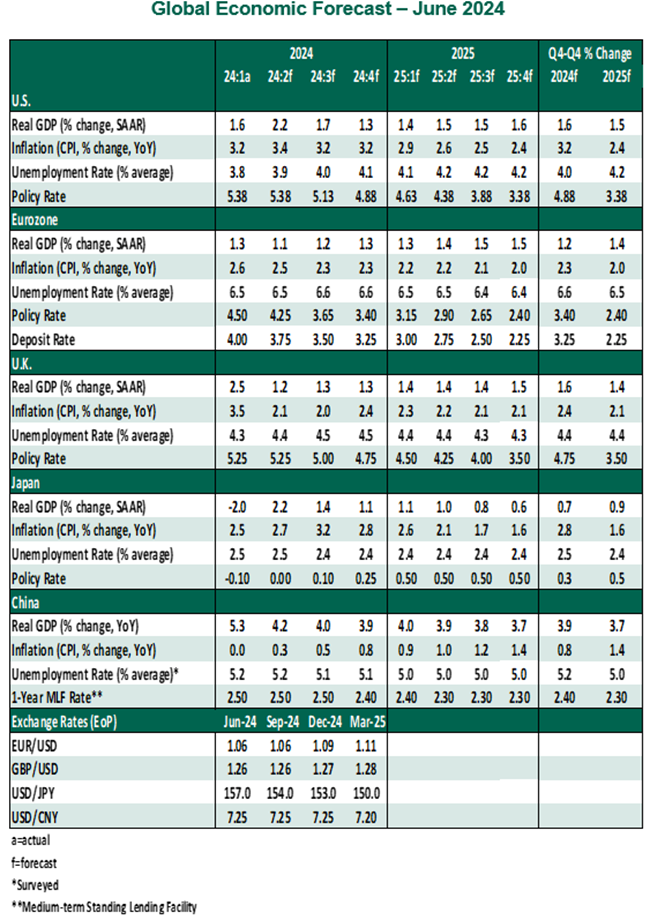

- First quarter real gross domestic product (GDP) growth was confirmed at 1.3% annualized, following a 0.2% contraction in the fourth quarter of 2023. Positive contributions from trade and consumption partially offset declines in investment and inventories. Though activity improved in the first quarter, the divergence in performance among member states and sectors persists. Services remain the sole driver of growth, visible in the growing gap between services and manufacturing Purchasing Managers’ Indexes (PMI).

While growth is poised to continue in the second quarter, the drop in the PMI and the Ifo index are adding to uncertainties surrounding the strength of the euro area economy. We expect a bumpy recovery, not a spectacular rebound.

-

- Inflation in the eurozone surprised to the upside in May, with both headline and core measures rising two-tenths to 2.6% and 2.9% year over year. The 0.4 percentage point rebound in services inflation led to the overall increase. While this latter component remains the main inflationary force, the breadth of inflationary pressure is more moderate in the eurozone than elsewhere.

- Disinflation from a peak of 10.6% in October 2022 to 2.6% in May 2024 was deemed by the European Central Bank (ECB) enough to begin easing at the June meeting. But the path forward is uncertain. The sticky nature of domestically-generated price pressures has raised the risk that the last mile of the journey to target could take longer to run, preventing the central bank from providing any hints of its future course of action. We expect only two additional cuts this year, with the next action coming in September.

- Wage growth In the euro area reaccelerated in the first quarter, but moderation is in store in the second half. Forward-looking pay indicators are weakening; businesses are absorbing the impact of a larger wage bill, limiting increases in final prices. The European Commission’s (EC) survey of selling price expectations has been trending down, despite the rise in unit labor costs.

- Signs of slack in the labor market are starting to appear, though conditions are still far from being labeled as weak. Employment has continued to grow, but at a slower pace. The job vacancy rate has been falling but is still above pre-pandemic levels. Firms’ employment expectations are trending down.

- Credit and lending conditions in Europe are improving, but remain fragile. The ECB’s April Bank Lending Survey showed a lower share of banks reporting tightening in credit standards. This was consistent with the recent improvement in lending volume growth and the EC’s survey of households' major purchase intentions. While loans to households and non-financial corporations are exhibiting weak momentum, lending is likely to recover as interest rates moderate.

- The election season has arrived sooner than expected in Europe. The outcome of the recent European Parliament election offered some surprises, but the status quo is likely to prevail at the European Commission. The real impact of this election outcome is being felt in France, with President Macron announcing snap elections to be held on June 30 and July 7.

The announcement has increased uncertainty and market volatility as a range of outcomes are plausible. A hung parliament will not allow any political group to pass meaningful reforms and tax or spending measures, leading to policy paralysis. A far-right majority will likely have the most profound impact on the French economy and put the country on a confrontation path with the European Union (EU) on a range of matters including immigration, defense and economic policy.

The eurozone is returning to fiscal prudence as the EC recently took the first step towards placing seven member states into an Excessive Deficit Procedure over their fiscal situations. France is among them; this will leave little room for the increases in public spending that the opposition party favors. France’s sovereign bond yields are trading at an increased spread to German equivalents.

- Europe exited the 2023-24 winter with a record level of gas stocks and is already preparing for the next winter. The EU’s gas storage facilities are 75% full, set to hit 100% well in advance of the self-imposed November 1 deadline. A winter energy crunch looks unlikely. However, risks to supply remain as reflected in the recent spikes in gas prices on the back of unplanned outages in Norway and increasing demand for liquified natural gas in Asia.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

© Northern Trust

Read more commentaries by Northern Trust