Home ownership is a widely-shared financial goal. Among other benefits, homeowners can expect a much greater degree of wealth accumulation. With rare exceptions, residential real estate gains value steadily. In recent years, the pandemic-driven demand surge pushed U.S. home values up at an outsized rate of over 15% per year in 2021 and 2022; they have since held those gains.

But for all their benefits, our homes are not liquid assets. They sometimes feel quite the opposite, requiring homeowners to continually shell out for maintenance and taxes. We may feel wealthy for owning an appreciating asset, but with no cash flow to show for it. Gains in value are only realized after a sale—perhaps to move to a retirement destination, perhaps a windfall bequeathed to our next of kin.

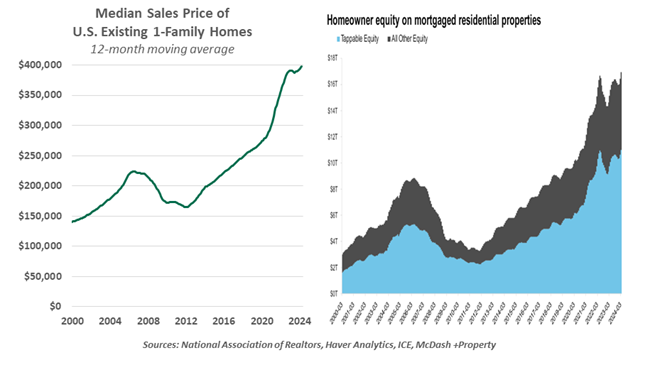

RECENT INCREASES IN HOME VALUES HAVE PRODUCED A SURGE IN HOUSEHOLD WEALTH.

If home equity were more freely realized, the potential benefit to consumption could be tremendous. The ICE Mortgage Monitor Report estimates that Americans have over $11 trillion of tappable home equity, the value that homeowners could borrow without exceeding an 80% loan-to-value ratio. Approximately 48 million mortgage holders have tappable equity, averaging $206,000.

Products are available to extract value from our real estate holdings. Mortgages can be refinanced, with additional cash borrowed in excess of the old loan’s principal. Refinancing, with or without cash taken out, is common in a falling-rate environment. Today, these deals are moribund. Borrowers are not eager to let go of their low fixed-rate mortgages.

Borrowers can instead leave their first mortgage intact and take on a second obligation against their available equity, structured either as a closed-end installment loan or a home equity line of credit (HELOC). By pledging the home as collateral, borrowing limits and interest rates are more favorable on these products than could be obtained from a credit card or unsecured personal loan. However, they carry the costs and difficulty of underwriting a mortgage and perfecting a second lien on a property. For that reason, products that access home equity are typically taken out by borrowers intending to finance major expenses like home improvement.

Hoping to enhance consumers’ ability to tap their equity, mortgage guarantor Freddie Mac has proposed a new offering to purchase second mortgages. Traditionally, Freddie Mac and Fannie Mae have been the two government-sponsored entities (GSEs) that purchase and repackage residential mortgages into mortgage-backed securities. They have always dealt in first-lien mortgages, but they have not touched second mortgages since reforms were made in the wake of the 2008 global financial crisis (GFC).

Borrowers would benefit from the new initiative by keeping the favorable rate on their existing primary mortgage, while taking out additional cash. The proposed structure of a 20-year installment loan would keep payments low, and the security of GSE sponsorship would keep interest rates in check. Originators and servicers could earn fee revenue selling and managing these loans. The GSEs would gain a broader view of market risk, as current second mortgage products are typically held on lenders' balance sheets, not in secondary markets.

STIMULATING HOME EQUITY BORROWING HAS ITS DOWN SIDES.

But the risks of property sector leverage are a not-so-distant memory. Easy lending terms and financial products derived from mortgage debt were the fuel for the GFC. As favorable as the housing outlook is at the moment, that experience taught us that homes can indeed lose value. Newly-minted home equity loans would take the first losses in the event of default, and GSE sponsorship puts U.S. taxpayer funds at risk.

Moreover, allowing homeowners to reach into their equity would jeopardize the much stronger financial position that their homes help them attain. Savings that they might need later in their lives would be drained away prematurely. Financial planners often note that houses are not intended to be automated teller machines; families might be advised to use these assets to sustain their standards of living in retirement. And if the program were to see rapid uptake, the sugar rush of additional cash will complicate the effort to contain inflation.

Adding leverage to household finances is a known recipe for stress. We wish that policymakers would devote more effort to improving the availability and affordability of homes; easier borrowing for current homeowners should not be a priority.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust