Ex-Factor: Housing Holds Some Economic Keys

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsHousing has been a frustrating segment of the economy to analyze, both since the pandemic first erupted and the Federal Reserve embarked on an aggressive rate-hiking cycle two years ago. So-called "traditional" housing indicators—which typically act as signals for where the broader economy is headed—have misfired in this unique, pandemic-driven economic cycle, telling us time and again that a broad-based recession is imminent, when it has in fact failed to materialize. A dearth of home supply (a phenomenon that preceded the pandemic), record-high home prices, and an inflationary surge have put immense pressure on homeowner affordability over the past few years—thus putting commensurate downward pressure on consumer confidence metrics.

That said, despite the misfire from key leading indicators, there are signs that the sector is recovering. There are also signs that the affordability crisis is abating, albeit slowly. As housing was the first sector to kick off the rolling recessions we've pointed out for more than two years, it now looks like it's participating in the start of rolling recoveries. That comes with an important distinction, though: A recovery is not synonymous with a booming expansion.

Still recessionary?

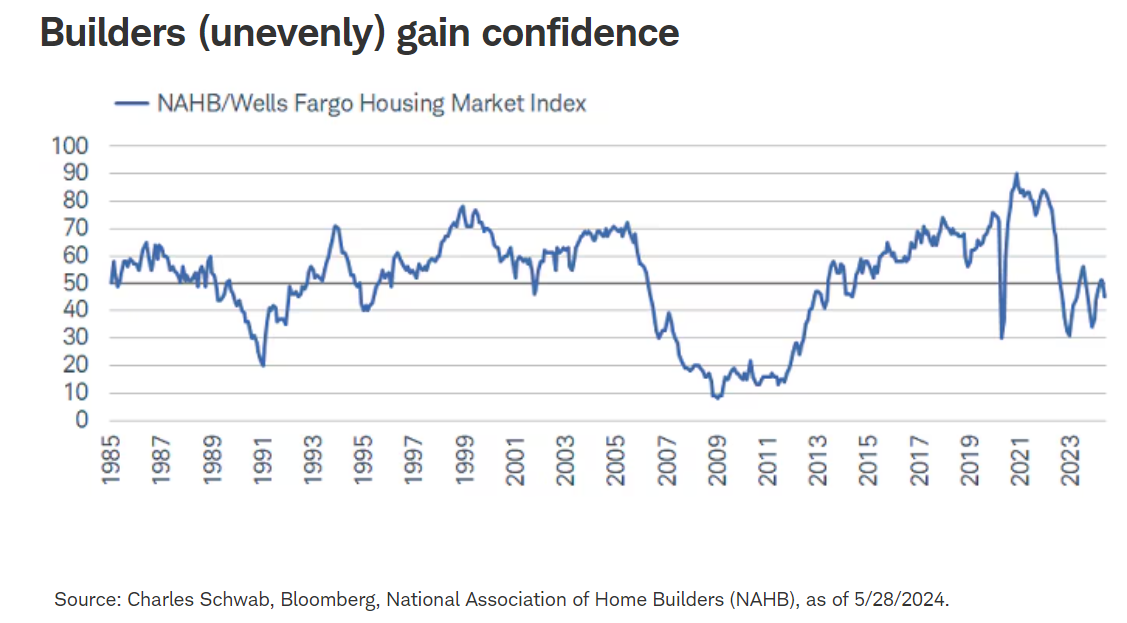

One of the most relied-upon leading economic indicators is the Housing Market Index (HMI) from the National Association of Home Builders (NAHB), which tends to peak well in advance of a recession, giving a firm warning sign that a slowdown is coming. As shown below, the HMI peaked in 2021, undergoing a mild initial descent and then a waterfall decline that accelerated in 2022.

After hitting a trough in December 2022, the HMI bounced sharply, entering what looked at the time like a durable recovery. That proved to be a head fake, though; since that bounce, the HMI has been chopping around in a rather wide range.

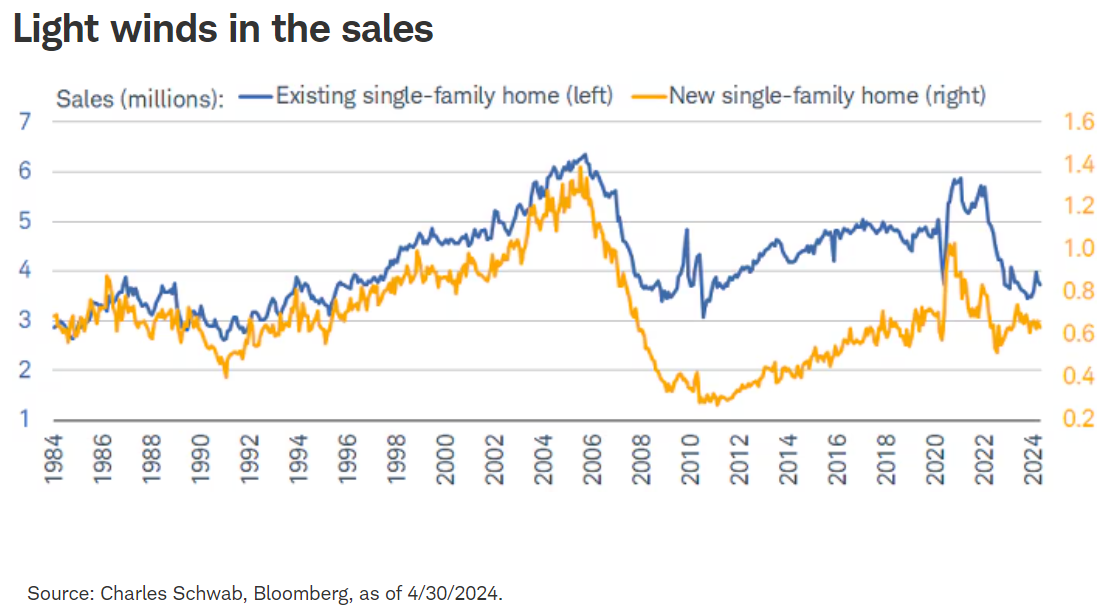

In a similar vein, home sales may have troughed for this cycle but are taking a while to reaccelerate meaningfully. Existing single-family home sales tend to be a larger focus since they make up the majority of the market. As shown below, they plunged over the past couple years, experiencing a maximum drawdown of -41%. While they're still down 36% from their cycle peak, they've increased nearly 9% since the recent trough. New home sales experienced an even worse maximum drawdown of nearly -50%; and while they're still down more than 38% from their cycle high, they've recovered more than 22% from their recent trough.

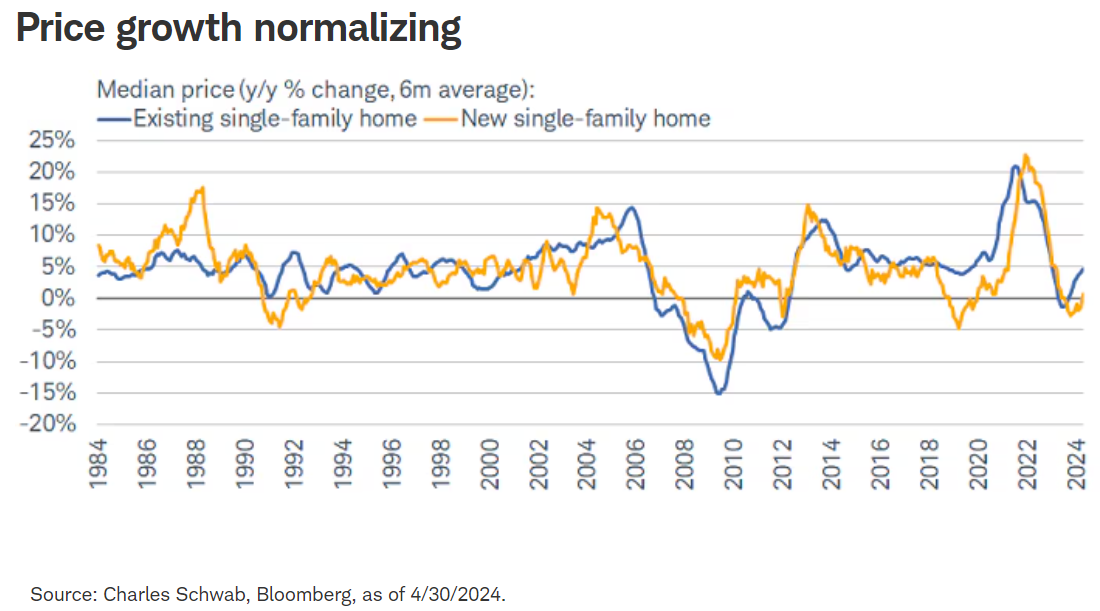

Against conventional wisdom and unlike a normal cycle, home price growth accelerated sharply as home sales fell precipitously. As shown below, median prices for new and existing single-family homes grew at a breakneck pace in 2022 and 2023, outpacing anything we've seen in the past four decades.

Growth eventually came back down to earth, but prices are back in positive territory; and this time, it's happening as sales are improving. Given that brief decline, prices in level terms are still elevated; in fact, the median price of an existing home is back up to $412K (near an all-time high). The median price for a new single-family home is $433K (also near an all-time high).

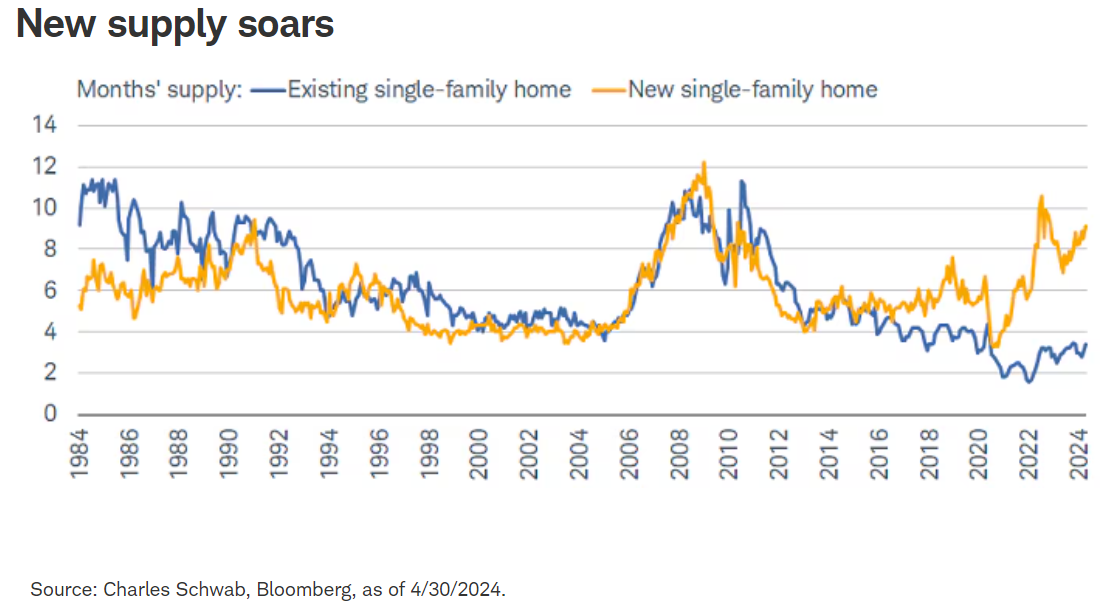

Price growth has been faster—and the recovery in sales has been slower—for the existing home market, mostly because of depressed supply. Shown below is monthly supply for both existing and new homes. A huge gap has opened between them over the past few years, with the recovery in new home prices outpacing existing by a significant degree. This is one of the key, if not main, drivers of the recovery in new home sales. Buyers who haven't been able to find what they're looking for in the existing market have effectively been pushed into the new market.

As that has happened, the recovery in existing home supply has been sluggish. That has mostly been the case for the past decade, though. After the Global Financial Crisis (GFC), the housing market experienced an anemic recovery, defined by a chronic under-building of homes.

The shortage of homes wasn't a huge issue leading up to the pandemic, not least because we didn't have the dynamics we have today: a larger chunk of the population working from home, a significant increase in mortgage rates, and (at one point) a 40-year high in inflation, among other things.

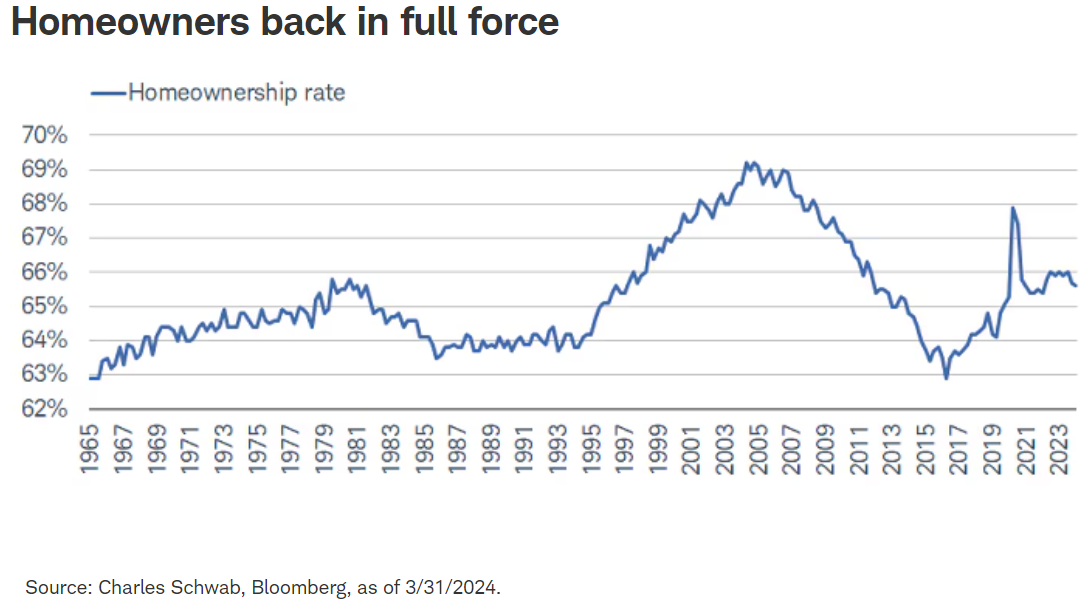

Not only that, but the homeownership rate had been in a significant decline before, during, and after the GFC. Now, we find ourselves looking back at a major rise in ownership over the past handful of years. That's certainly a positive, but it has also added to the pressure on home availability and affordability.

Gimme (affordable) shelter

For any recent or aspiring homeowner, it's no surprise that affordability is significantly constrained in this cycle. This has prevented individuals and families from purchasing a home, forced them into intense bidding wars, or caused them to make more painful financial tradeoffs in order to purchase a home.

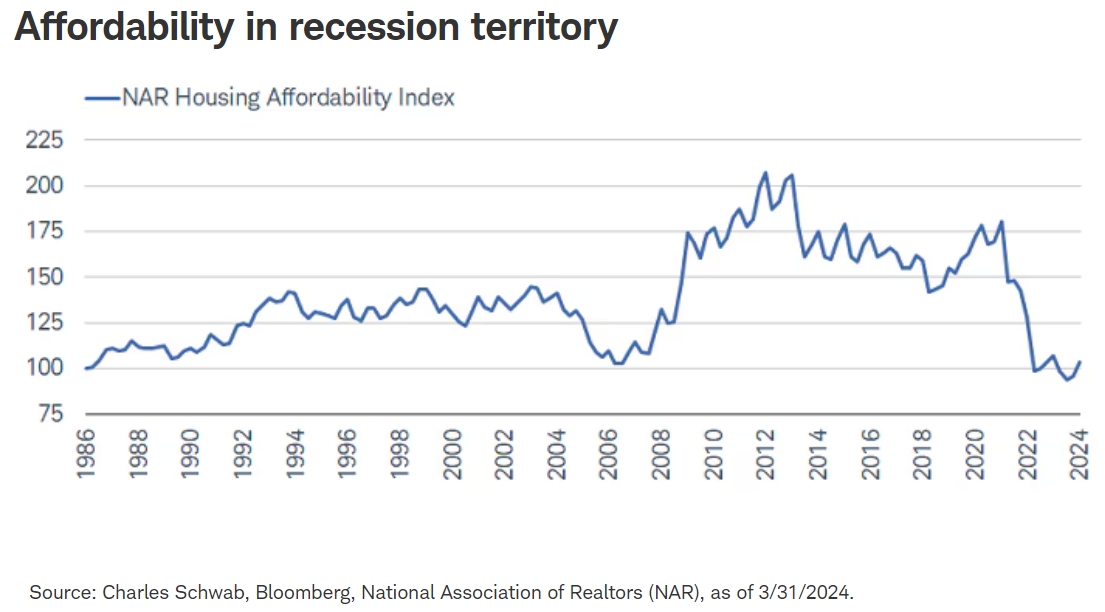

In fact, the Housing Affordability Index (HAI) from the National Association of Realtors (NAR) fell to an all-time low in the third quarter of 2023, as shown below. Like some of the data shown at the beginning of this report, the HAI seems to be carving out a bottom, but investors should again note that the ensuing climb might be sluggish—especially if consumers take longer to adjust to a higher-for-longer interest rate world.

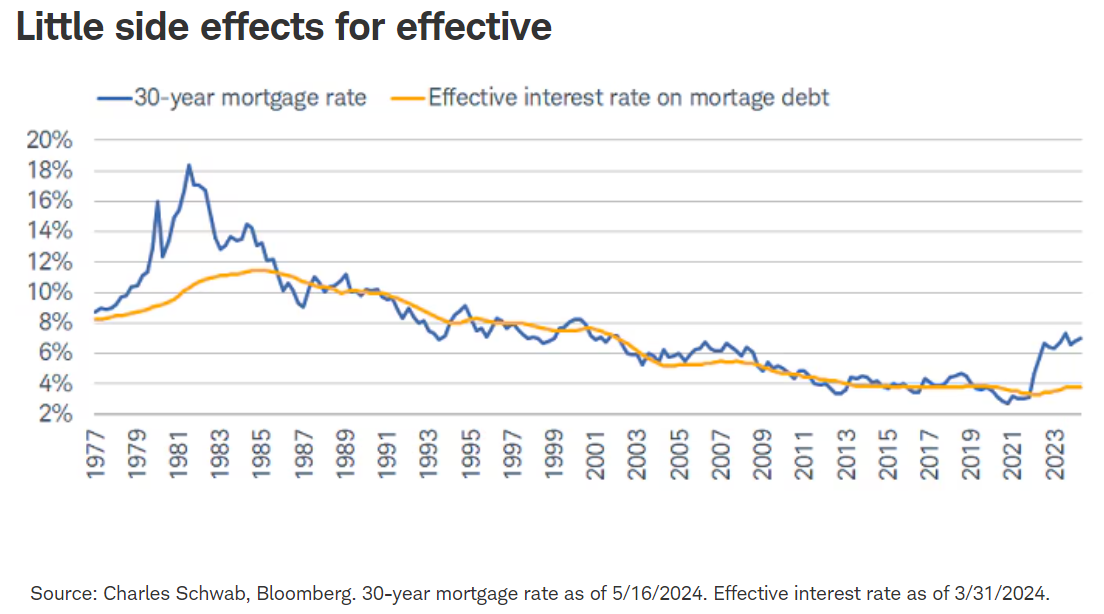

Assuming the Fed doesn't take rates back to zero in this cycle—which officials have been adamant about—one of those adjustments will likely be higher mortgage rates. As shown in the chart below, the average 30-year mortgage rate has soared to multi-decade highs—not yet in the atmosphere of the 1970s and 1980s, but still quite high relative to to the post-GFC and pre-pandemic average. Key to focus on is the yellow line, which shows the effective interest rate on mortgage debt. At sub-4%, it reflects the rate that most existing homeowners have today, which means a huge chunk of the population has been insulated from the sharp increase in mortgage rates over the past couple years. The widening spread between the lines in the chart has helped drive the narrative that Fed policy has had little effect on the housing market thus far. That's not entirely true; policy has been effective, just for a much smaller portion of the market.

We expect the upward drift in the effective mortgage rate to continue as interest rates normalize from its pre-pandemic low. As such, we think consumers will slowly adjust to higher rates over time. Higher rates in and of themselves do not preclude people from buying homes; there are several other factors at play.

Sweet and sour

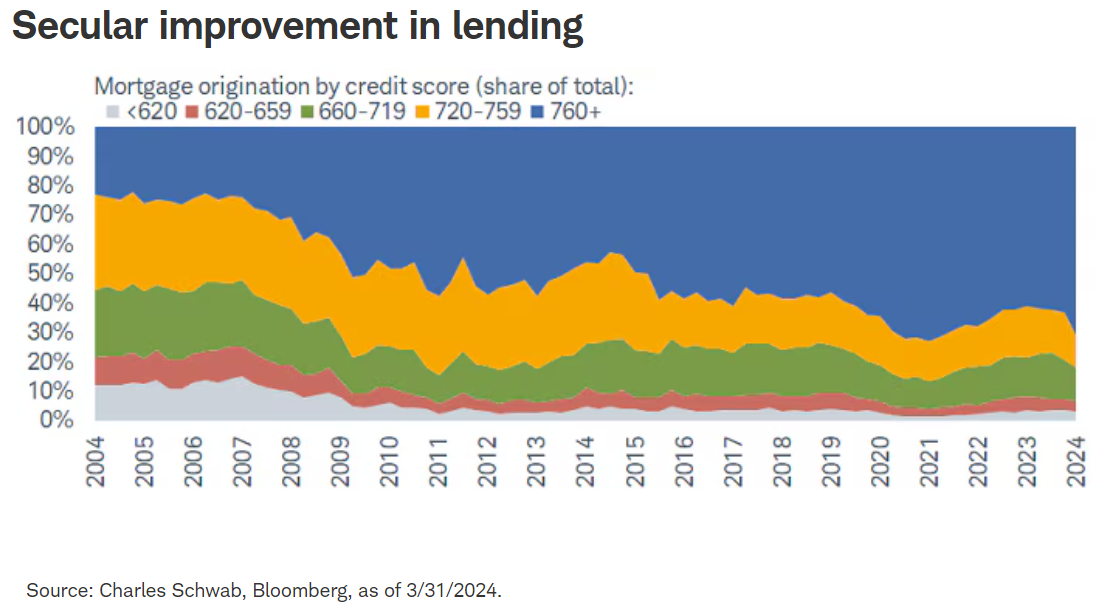

While housing's choppy recovery has been slow, it hasn't been marked by speculative practices or low-quality lending. As shown below, the majority of mortgage originations are currently concentrated in individuals with exceptional credit scores. That's the "sweet" part and quite a shift from the pre-GFC era, when nearly half of originations were in cohorts with scores less than 720.

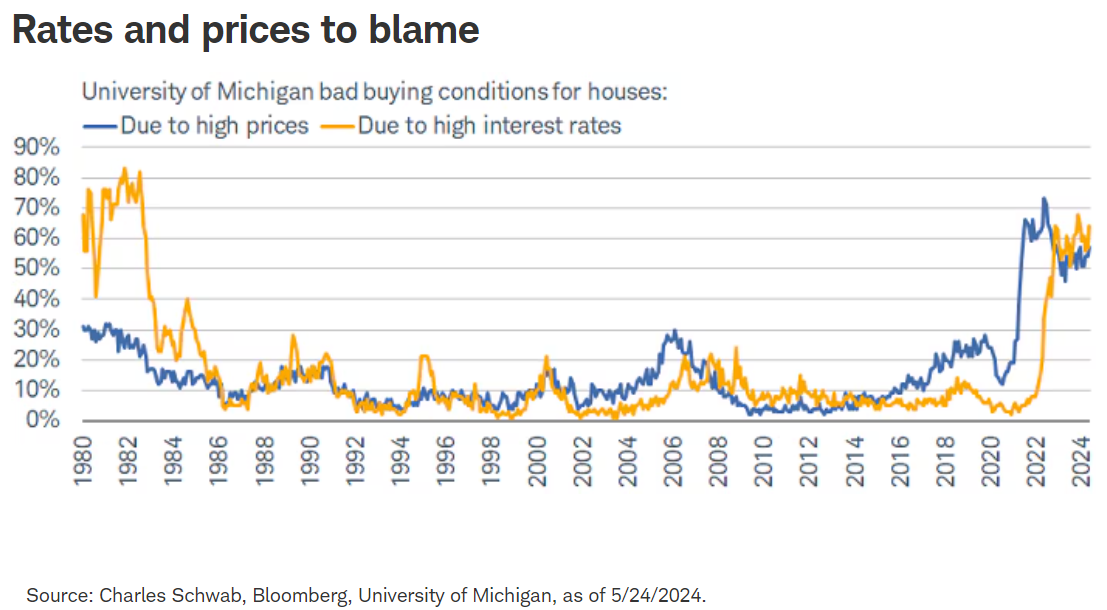

Yet, the "sour" aspect is that most consumers aren't taking much comfort in these bright spots; evident when looking at confidence (or lack thereof) when it comes to housing. As shown below, the University of Michigan's Consumer Sentiment Index is still showing dour sentiment when it comes to home buying conditions. A significant percentage of consumers continue to cite poor conditions due to both high prices and interest rates; a marked difference from the 1980s, given high rates were the main driver of weaker sentiment back then. This time, consumers are feeling the pinch on both ends.

In sum

Naturally, this all begs the question of what can alleviate the pain consumers and aspiring homeowners face, and right now, time increasingly looks like a viable answer. It takes time for consumers to adjust to rising price and interest rate levels—especially when increases are large in magnitude and occur in a short period of time—and for home supply to recover.

Regarding the cyclical indicator that is the housing market, it's also taking time for housing to give accurate signals as to what the economy's path ahead looks like. Typical relationships haven't been reliable this time around, evidenced by the collapse in the HMI yet no subsequent spike in the unemployment rate, or the plunge in home sales yet only mild easing in home prices. The upside is that housing's own recession hasn't been nearly enough to tip the rest of the economy into a contraction. The downside is that with a recovery in housing now seemingly in play, it's hard to extrapolate and fully understand the signal that sends for the rest of the economy.

We think it's a net positive that housing seems to be exiting its own recession, but it's not doing so without some significant scarring. An entire investor and consumer base has been burned by the significant level shift for both home prices and interest rates over the past few years. That doesn't mean housing can only fully recover if prices and rates come down dramatically, given there are other (perhaps stronger) factors at play, such as supply. Yet, a stabilization in activity, price growth, and interest rate volatility will likely provide a more stable foundation for the sector.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

All names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

National Association of Homebuilders (NAHB) Wells Fargo Housing Market Index (HMI)- Based on a monthly survey of NAHB members designed to measure homebuilder sentiment in the single-family housing market. The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next 6 months as well as the traffic of prospective buyers of new homes. It is a weighted average of separate diffusion indices for these three key single-family series.

National Association of Realtors (NAR) Housing Affordability Index- Measures whether or not a typical family could qualify for a mortgage loan on a typical home. A value of 100 means a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home. An index above 100 signifies that family earning the median income has more than enough income to qualify for a mortgage loan on a median-priced home, assuming a 20 percent down payment.

0524-4TWK

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All