Originally published in April 2024

Key Insights

- Corporate bonds offer attractive income, but security selection is imperative as rising headwinds could lead to defaults picking up.

- Credit-intensive research is essential to help identify potential attractive companies and those with elevated risks.

- The three primary components of quality credit research are quantitative and qualitative analysis connected with collaboration between the research teams.

With some of the highest yields available in a decade, credit markets are an attractive income opportunity for investors at present. But with companies facing headwinds from a higher cost of borrowing and a weak global economy, it’s important to choose an investment approach that is risk aware and emphasizes rigorous research. Why? Because it’s not just about picking potential winning companies; avoiding losers is just as important, particularly in the current climate where defaults look set to rise due to the more challenging conditions.

In this second piece of our series on credit markets, we’ll delve into the factors that we see as essential to a quality credit research process. Specifically, what are the features that can help identify potential attractive companies and those with elevated risks.

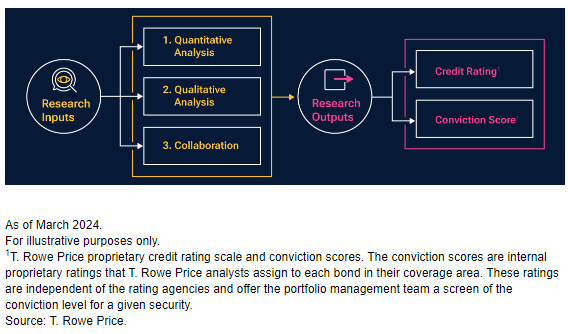

Fundamentally driven bottom‑up research

Credit research must be underpinned by deep analysis across industry, region, and sector. It should feature detailed credit analysis at an individual issuer level that fosters a deep understanding of a company and the potential risks and rewards involved with investing. The three primary components of this include quantitative and qualitative analysis connected with collaboration between the research teams.1

Core components of quality credit research

(Fig. 1) Key research inputs and outputs that help identify credit risks and opportunities

1. Quantitative analysis

The aim of quantitative analysis is to determine the ability of a company to pay its debt obligations. To do this, a range of company financial variables and credit statistics need to be assessed, such as revenues, cash flows, debt, leverage, and profit margins. This should not only be a snapshot in time, but also a look at how the variables change over time. A trend of steady deterioration, for example, could be a sign that a company is struggling.

Modeling future earnings and other variables is also vital. This is to gauge how a company’s risk profile might evolve in the future. Projections should be tested against a range of scenarios, including stressed situations, to illustrate how a company might perform in different market environments. Default scenarios should also be constructed to identify the catalysts that could trigger a credit event, as well as the likely effects thereafter.

2. Qualitative analysis

The aim of qualitative analysis is to determine the willingness of a company to pay its debt obligations. This takes the review process beyond the financial statements, which is important. Why? Because key signals can be gleaned from looking at factors such as quality of management, their strategy, and future plans. For example, is the company looking for acquisitions that could result in taking on more debt? Or is a long‑serving CEO about to retire, increasing the uncertainty about a company’s future direction? Each scenario has the potential to impact the outlook of a company.

Other qualitative factors to evaluate include the dynamics of an industry. Technological changes, for example, can disrupt and impact a company. The economic environment can also influence how a company performs. For instance, a recession could weigh on earnings if a company is operating in a cyclical sector. In all, a multitude of qualitative factors could impact the price of company debt, so it’s critical to evaluate and include them in modeling and forward‑looking projections.

3. Collaboration

Complementing quantitative and qualitative analysis with collaboration between research teams can further enhance the research process. Teams can share information and different perspectives of company risks. For example, an environmental, social, and governance (ESG) analyst could flag a potential ESG risk of a company, while models run by quantitative analysts can provide signals uncorrelated with fundamental research, which can further enhance risk management capabilities. Equity analysts may open up access to company management teams for meetings and site visits to see firsthand the inner workings of a company. Economists and sovereign analysts can give perspectives on the top‑down environment and macro conditions that may affect an industry.

The three‑pronged approach serves to generate a credit rating that indicates a company’s credit quality and default risk. Then to inform whether to buy or sell, a conviction score also must be generated. This requires further quantitative and qualitative research analysis, including looking at:

- How a company compares with peers in the same industry.

- Assessing yield curve dynamics and whether there’s a particular maturity point that offers better value.

- The structure of the bond issue.

- Technicals, such as supply and demand dynamics, i.e., is the company about to bring a new bond issue that could impact the price of its bonds on the secondary market?

- A liquidity assessment of an issuer.

Ultimately, this depth of insight helps identify securities that are trading cheap or rich to fair value and informs the level of conviction in recommending a strong buy to avoiding a bond and company entirely.

In all, this fundamentally driven research approach represents a holistic credit assessment with deep understanding of a company’s risks and opportunities. It helps identify companies that have strong and improving credit profiles within their industries. And, equally important, it can uncover weak companies run by poor management teams or that have elevated default risk. This depth of insight is especially important in the current climate where rising headwinds could lead to credit fundamentals deteriorating and defaults picking up. It is important to be vigilant and prioritize research. Such an approach can help to give investors’ confidence about credit investing this year and empower them to take potential advantage of the attractive yields that are available.

1. T. Rowe Price Associates, Inc.’s (TRPA) research platform is global, T. Rowe Price Investment Management, Inc.’s (TRPIM) is not. TRPA and TRPIM are separate investment advisor entities and do not collaborate on research.

Additional Disclosure

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Important Information

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

The views contained herein are those of the authors as of April 2024 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

This information is not intended to reflect a current or past recommendation concerning investments, investment strategies, or account types, advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Please consider your own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. Fixed-income securities are subject to credit risk, liquidity risk, call risk, and interest-rate risk. As interest rates rise, bond prices generally fall. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Investment Services, Inc.

© 2024 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

202405-3593352

A message from Advisor Perspectives and VettaFi: Dive into alternative investment opportunities at our upcoming Alternatives Symposium on May 30, and gain insights into diversifying portfolios beyond traditional equities and fixed income.

© T. Rowe Price

Read more commentaries by T. Rowe Price