Economic readings to start this year were hotter than expected, with inflation proving persistent and job creation exceeding levels we associate with a steady labor market. In the range of potential economic outcomes, this is not an altogether bad scenario. Inflation may hold higher than we were accustomed to in prior cycles, but if a strong job market allows wage gains to keep pace, it’s survivable.

But these circumstances are not ideal. A runup in inflation is a greater risk from a higher starting point, and the Fed will hesitate to ease as long as inflation holds above the 2% target. We can do better, and we expect the momentum to soften. The labor market is moderating, and inflation is cooling, albeit unevenly. High interest rates are helping to limit excessive spending, while financial conditions more broadly remain favorable to investors.

Following are our thoughts on recent data and developments.

KEY ECONOMIC INDICATORS

Influences on the Forecast

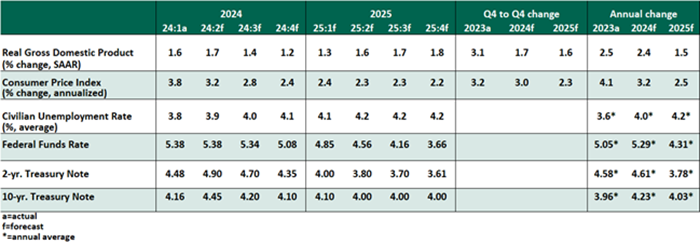

- The April employment report offered a welcome reprieve from the hot start to the year, with a more temperate 175,000 jobs created. Continued growth in the labor force brought the unemployment rate up to 3.9%. Markets welcomed the news, as this more moderate pace is needed for the Fed to contemplate rate cuts this year.

Average hourly earnings cooled to a gain of 3.9% year over year, its slowest pace since the inflationary surge of spring 2021. A moderation in wages is needed to contain services inflation.

The Sahm Rule flags a recession when the unemployment rate’s 3-month rolling average increases by five tenths from its prior-year low. Unemployment’s trough was 3.4% in April 2023. As that lowest reading ages out, the Sahm threshold will rise; unemployment can reach 4.1% this year without triggering the rule.

- The April reading of the Consumer Price Index (CPI) showed marginal improvement, with headline inflation falling a tenth to 3.4% over the past year, and core (excluding food and energy) improving by two-tenths to 3.6%. A further normalization of anomalous categories like apparel and motor vehicle insurance will help to calm core inflation further, but shelter costs (+5.5% on the year) are the biggest obstacle to reaching targeted inflation rates.

The March reading of the personal consumption expenditures (PCE) price index, the basis of the Fed’s 2% target, showed reacceleration to 2.7% year over year, a two-tenths increase from the prior month. Excluding food and energy, the index was steady at 2.8%. Merely stating that today’s inflation is lower than peaks of in 2022 is no longer sufficient; more improvement across the board is needed.

- First quarter real gross domestic product grew at an annualized rate of 1.6%, a step down from 3.4% in the prior quarter. However, the volatile categories of inventory accumulation and net trade together provided a -1.2 percentage point drag on the reading. Final domestic demand (the sum of personal consumption, private investment and government purchases) showed more encouraging growth of 2.8%, a slightly slower pace than was seen in 2023.

- At its May meeting, the Federal Open Market Committee acknowledged a “lack of further progress” on inflation. However, the tone was not maximally hawkish, with Chair Powell pushing back against when questioned about rate hikes. Firm data in the first quarter did not deter the committee from its intended path of rate cuts this year. We expect cuts in September and December; the election will not forestall a live meeting in September.

The FOMC also announced the beginning of the taper of quantitative tightening. Starting in June, the pace of the rundown of the Fed’s U.S. Treasury holdings will fall by more than half to $25 billion per month, from $60 billion. The announcement included no further guidance or key metrics to gauge the next steps toward a neutral balance sheet; governors are watching liquidity and bank reserves closely.

- The 10-year U.S. Treasury yield rose nearly 50 basis points from the end of March to the end of April as markets calmed from the first quarter risk rally. Yields have subsequently declined in the month to date. The duration of the yield curve’s inversion continues to set records, unlikely to abate until the Fed proceeds with cuts to lower yields on the short end.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Northern Trust

Read more commentaries by Northern Trust