Key Takeaways

- The buyers of bonds today are different from the buyers of bonds during the QE era. Today’s buyers are price-sensitive, and the burden has mostly fallen on households.

- As long as the Fed is expected to cut rates, there will be plenty of buyers for U.S. Treasurys.

- When conditions change, prices can quickly change.

Investors have been obsessed with when the Fed will cut and how many rate cuts there will be this year and over the entire cycle.

And rightly so! We have shown several times that 10-year Treasury yields tend to peak 2-3 months before the first rate cut, and don’t do much afterward, on average.

While Powell all but ruled out another rate hike, which pleased investors, there were several other developments last week that we thought were noteworthy.

The FOMC announced that it will slow the pace of Treasury runoff to $25 billion a month from $60 billion – more than expected. Yet not one reporter bothered to ask why they went with a bigger reduction. This action will help market liquidity.

The Treasury expects to keep its nominal coupon and floating rate note auction sizes stable for the next several quarters. We’re less certain about the next several quarters since we don’t know what the outcome of the elections will be. Nevertheless, as we noted last week, last year’s term premium peak near 50 bp and 10-year Treasury yield peak around 5.00% should hold for the next six months (or until the elections).

The Treasury also announced buyback plans of $14 billion for off-the-run longer-term securities to improve market liquidity. To offset these purchases, Treasury will issue more bills by converting the current 6-week Cash Management Bill into a benchmark bill. This will continue to put modest downward pressure on the slope of the yield curve.

Who’s buying bonds?

The buyers of bonds today are different from the buyers of bonds during the QE era. Today’s buyers are price-sensitive, and the burden has mostly fallen on households, as shown on the chart. There will always be a price to clear the market. So now we are just haggling over the price.

If the economy is slowing, unemployment rising, inflation receding, and the Fed is expected to cut rates, there will be plenty of buyers for U.S. Treasury notes and bonds. But make no mistake. When conditions change, prices can change too – and quickly!

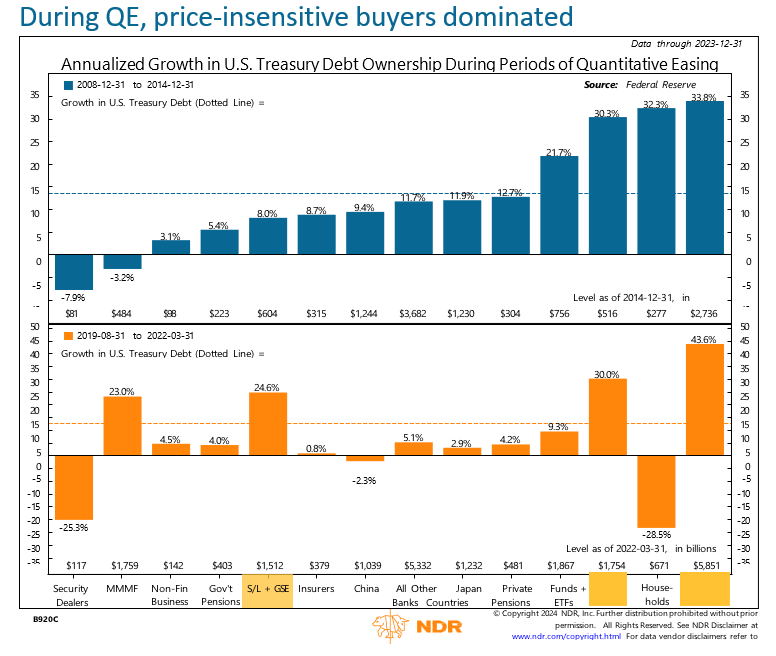

Buyers during QE were price insensitive and either government or quasi-government entities (the Fed, banks, state and local governments, and foreign investors).

Speaking of foreign investors, while politicians in Washington D.C. think it’s a good idea to slap a bunch of tariffs on China to shrink our trade deficit with them, the Chinese were recycling that money by buying U.S. Treasurys, since they don’t have good alternatives to Treasurys. But as the trade deficit shrinks with China and expands elsewhere, not all that money will stay in the U.S., putting upward pressure on U.S. Treasury yields.

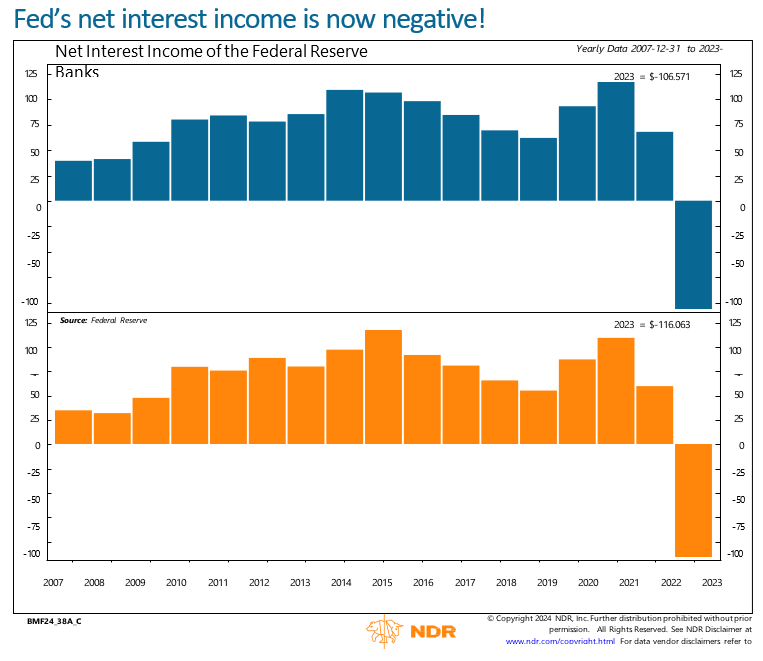

Finally, although the Fed will never admit it, lowering rates and restoring a positive yield curve will help the Fed reduce its deficit with Treasury. Last year the Fed incurred net interest income deficit of $106.6 billion. As a result, the Fed’s remittances

to Treasury were a record deficit of $116.1 billion. Since the Fed pays interest on reserves, negative net interest means the Treasury has to borrow even more to cover those payments!

Joe Kalish is the Chief Global Macro Strategist at Ned Davis Research. To learn more about Ned Davis Research, please visit www.ndr.com

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more commentaries by Ned Davis Research