The Federal Reserve just wrapped up another policy meeting, and markets continue to push back their expectations of a first rate cut. As of Wednesday, the federal funds futures market is pricing in 60% odds of a first cut in September. Barring another major pivot in Fed policy, many advisors agree it’s a prudent time to increase bond exposure – and that’s precisely what investors have done, albeit in a rather blunt fashion.

Treasury yields are hovering around their highest levels since the Global Financial Crisis of 2008. The yield on the benchmark 10-year Treasury note has risen 80 basis points this year but will likely start to plateau amid anticipated rate cuts. Meaning, that reinvestment risk is rising and there’s a good chance of capital appreciation over the next few years when cuts finally do kick in.

Tale of Two Bond Markets

Plain-vanilla bond funds are generally seeing the bulk of this year’s inflows. The iShares Core U.S. Aggregate Bond ETF (AGG) and the Vanguard Intermediate-Term Treasury ETF (VGIT) comfortably took the top spots – taking in $7.9 billion and $5 billion, respectively – followed by total bond market ETFs issued by the same two asset managers.

Topping the flow charts are largely long-duration, high-quality funds predominantly comprised of Treasuries and investment-grade securities across a range of maturities. Markets have been somewhat overzealous in their expectations of policy easing. Stronger growth data coupled with stickier inflation have caused long-duration bonds to cheapen.

But from a share performance standpoint, bond ETFs have taken a hefty beating this year.

The Case for High Yield

More than two-thirds of total bond market ETFs are down this year. As a result, many advisors are starting to consider sharpening their fixed income tools and narrowing their focus to non-core segments of the bond market.

High-yield bond ETFs have held up best (excluding leveraged and inverse products) on a total return basis. More than 80% of high-yield bond ETFs have seen positive returns for the year – despite many of them suffering net outflows in 2024.

Investment grade bonds are yielding roughly 6%, while high yield index’s yield to worst is close to 8% – offering a good 3% chunk on top of Treasuries, a tempting reward in exchange for more credit risk.

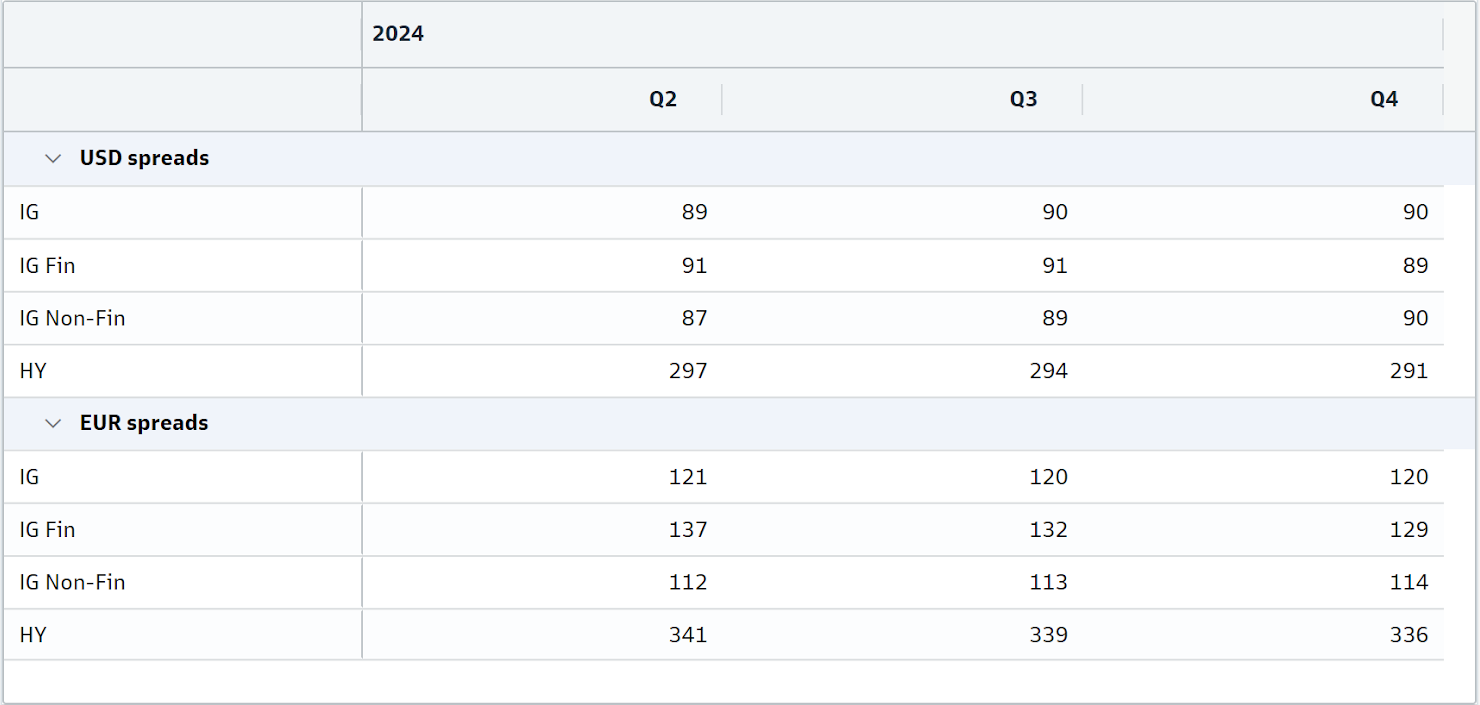

Credit spreads are already sitting near historically tight levels, but experts posit high yield spreads still have more room to tighten throughout the year as economic data continues to surprise to the upside.

Source: Goldman Sachs

Credit Spread Forecasts

Additionally, many advisors VettaFi surveyed at last month’s Fixed Income Symposium said they believe high-yield corporate bonds will perform best among fixed income securities in the next 12 months.

Following the Flows: Risk Appetite Widens

We’ve seen notable inflows into active high yield, like the BlackRock Flexible Income ETF (BINC), and in several lower-cost high-yield ETFs, like the SPDR Portfolio High Yield Bond ETF (SPHY) – which is among the cheapest products of its kind, charging a mere 0.05%.

There has also been strong interest in bank loan ETFs, a lesser-known pocket of the high-yield bond market. Such loans are typically considered below investment grade with low duration and relatively high yield exposure. Due to a lack of liquidity and name recognition, some advisors feel they provide better value for investors.

Now that the so-called soft landing has materialized, investors are willing to take on more credit risk. Both the VanEck Fallen Angel High Yield Bond ETF (ANGL) and the iShares Fallen Angels USD Bond ETF (FALN) have seen net inflows as a result. Both ETFs contain bonds that were previously rated investment grade but have since been downgraded. Yet they still exhibit historically higher average credit quality than the broader high-yield bond universe.

Two decades ago, investors were in the dark about what their bond funds held. But they’re becoming more educated on what’s below the hood of bond ETFs – and advisors are determined to help them fine-tune their fixed income exposure with newer products.

For more news, information, and analysis, visit the Beyond Basic Beta Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

More ETF Topics >