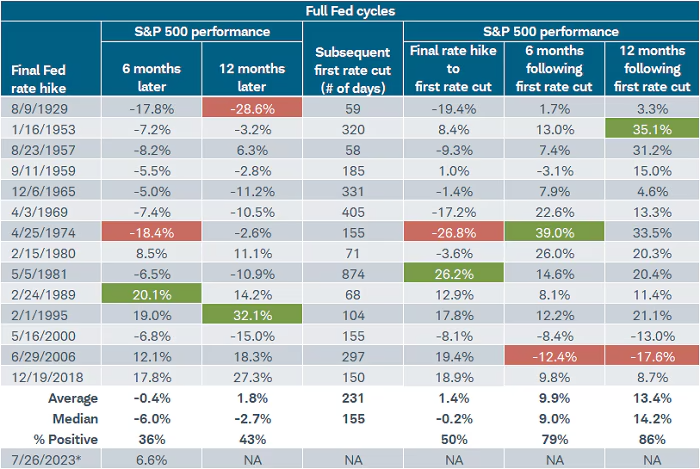

The March Federal Open Market Committee (FOMC) meeting is this week and although there is no expectation the committee will cut interest rates, there will be the release of the updated “summary of economic projections” (SEP) as well as the "dot plot" showing the collective committee member forecasts for the fed funds rate. As of this writing, the probability—per the fed funds futures market—of a rate cut at the May FOMC meeting has fallen from nearly 30% a month ago, to only 10% today. For the June FOMC meeting, the probability is about a coin flip. As such, for now, the Fed remains in "pause" mode (the period between the final hike in a cycle and the first cut). We debuted the table below in our 2024 outlook report, and it's chock-full of stock-market-related performance throughout historical (and full) Fed cycles.

Source: Charles Schwab, Bloomberg, Federal Reserve, 1929-3/15/2024.

*Assumes terminal hike for current rate hike cycle occurred on 7/26/2023. Green shading represents best S&P 500 performance and red shading represents worst S&P 500 performance. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance does not guarantee future results.

Warning: Beware of generalities in terms of market behavior when it comes to Fed cycles. There are only 14 historical cycles—a.k.a. a small sample size. In addition, as shown via the red and green boxes, there are wide ranges historically. A small sample size, along with a wide range of outcomes, evokes the old adage, "analysis of an average can lead to average analysis."

Many assume that once the Fed has finished hiking rates in a cycle, it's smooth sailing for stocks. But history shows that in the six-month period following the final hike in a cycle, the S&P 500 was up only 36% of the time, had average and median returns in negative territory; but importantly, showed a range from -18% to +20%. The odds improved a year after the final hike, but only jumped to 43%; and although the average return bumped into positive territory, the range was enormous, from -29% to +32%.

Moving to the middle column in the table above, the range of days during which the Fed was in pause mode was as short as 58 days in the late 1950s and as long as 874 days in the early 1980s. As such, an average of 231 days tells us nothing (especially given that only one historical range even had a 2-handle on it). More remarkable is the following column, showing the S&P 500's performance during the pause period. The average and median showed flattish returns, but that's largely useless information. The percentage positive was exactly 50%, meaning there were seven up moves and seven down moves, with a massive range from -27% to +26%.

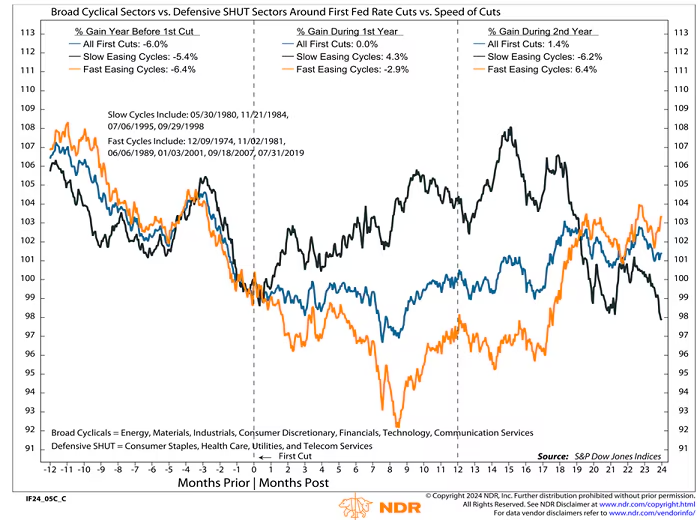

Cyclicals vs. defensives

Perhaps helping to explain the obsession with the timing of the initial rate hike, you can see in the table above that it wasn't until the Fed started cutting, that the averages/medians/ranges were more compelling. That said, as we've noted before, the exact timing of the cut isn't as important as the nature of the cut—notably, whether it's the start of a fast or slow cutting cycle. Barring any major economic shifts, as of now, the Fed has telegraphed—and the economic data have been supportive of—a slow cycle. In particular, that likely bodes well for cyclically oriented sectors.

As shown in the chart below, courtesy of our friends at Ned Davis Research, broad cyclicals (Energy, Materials, Industrials, Consumer Discretionary, Financials, Technology, and Communication Services) tended to outperform defensives (Consumer Staples, Health Care, Utilities, and Telecom Services) in slow cutting cycles—shown via the black line. Conversely, the opposite occurred in fast cutting cycles, as cyclicals didn't start doing well until about nine months after the first cut—shown via the orange line.

Slow cutting favors cyclicals

Source: ©Copyright 2024 Ned Davis Research, Inc.

Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/. 1974-3/18/2024. The chart and embedded tables show broad cyclical and defensive sector performance around first Fed rate cuts. Y-axis is indexed to 100 at start of first rate cut. An index number is a figure reflecting price or quantity compared with a base value. The base value always has an index number of 100. The index number is then expressed as 100 times the ratio to the base value. A fast cycle is one in which the Fed cuts rates at least five times a year. A slow cycle has less than five cuts within a year. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance does not guarantee future results.

Interestingly, since the Fed's last hike in July 2023, cyclicals have been outperforming, with Communication Services up the most (+22.3%), followed by Information Technology (+20.2%) and Financials (+14.4%). The only sector that has fallen is Utilities (-8%). That's not in keeping with what has historically happened leading up to the first cut, as shown in the far-left panel in the chart above.

We continue to remind investors that fast cutting cycles are often due to recessions. The three most recent Fed cutting cycles—which started in 2019, 2007, and 2001—were all fast in nature and followed by both bear markets and recessions. Barring any major deterioration in the economy (especially on the services side), we continue to think the market can digest the start of the cutting cycle, especially if it's not accompanied by a significant deterioration in economic growth.

Election

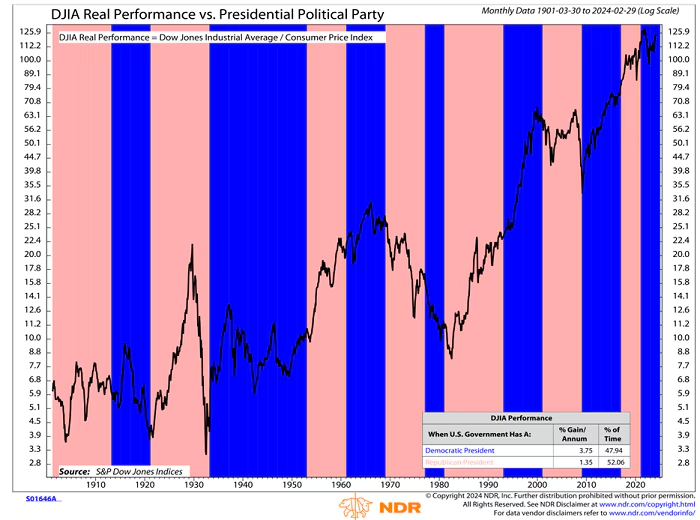

Aside from Fed policy, the other significant uncertainty this year surrounds the November elections. We are not political prognosticators, so we'll keep this section short and fact-based (imagine that). There are so many ways to slice and dice stock market behavior around election outcomes, but here are a few charts that lay out the history of stock-market gains (and/or losses) throughout the post-1900 history of elections.

The charts below are courtesy of Ned Davis Research and use the Dow Jones Industrial Average vs. the S&P 500 because the former has a longer history. Starting with presidential elections, the stock market has performed slightly better under Democratic presidents.

Dow vs. Presidential party

Source: ©Copyright 2024 Ned Davis Research, Inc.

Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/. 1901-2/29/2024. The chart shows the Dow Jones Industrial Average real (inflation-adjusted) performance. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance does not guarantee future results.

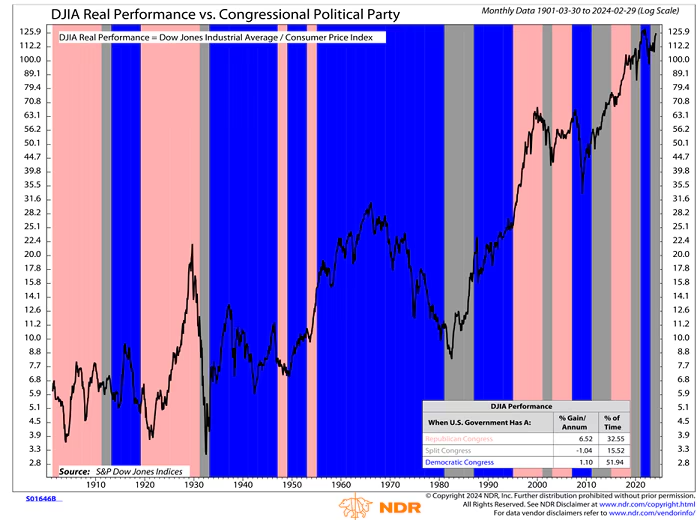

Dow vs. congressional party

Source: ©Copyright 2024 Ned Davis Research, Inc.

Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/. 1901-2/29/2024. The chart shows the Dow Jones Industrial Average real (inflation-adjusted) performance. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance does not guarantee future results.

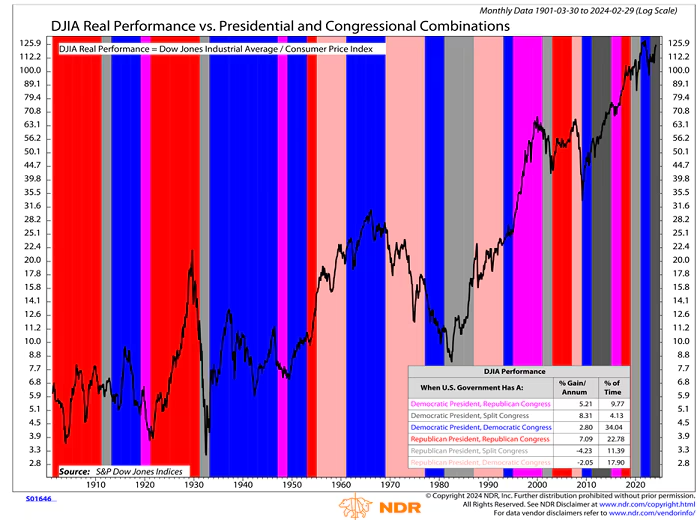

Combining the two, the chart below looks at the six possible combinations in terms of the presidential and congressional party breakdown. The best performance has occurred when there was a Democrat in the White House and a split Congress (the current configuration), but full Republican control a close second. The two worst (both with negative annualized returns) outcomes historically were under Republican presidents and either a split Congress or a Democratically controlled Congress. As an aside, the two most common outcomes (last column in the table below) were when there was full party control, a very unlikely outcome this year.

Dow vs. party combinations

Source: ©Copyright 2024 Ned Davis Research, Inc.

Further distribution prohibited without prior permission. All Rights Reserved. See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/. 1901-2/29/2024. The chart shows the Dow Jones Industrial Average real (inflation-adjusted) performance. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance does not guarantee future results.

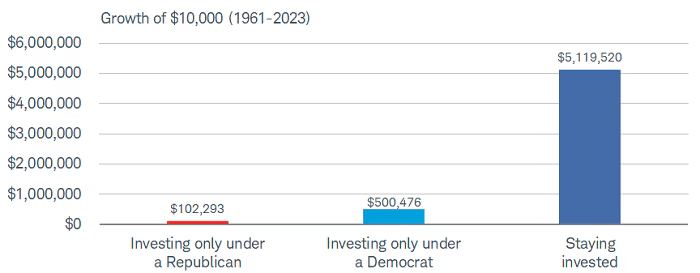

The real moral of the story

The final chart comes from Schwab's own chart library and frankly sends the most appropriate message for investors who think trading around election outcomes makes sense. Covering the modern period for the S&P 500, investing only when a Republican was in the White House, a $10K initial investment in 1961 would have grown to more than $102K by 2023. On the other hand, the same $10K initial investment would have grown to more than $500K, investing only when a Democrat was in the White House. Some might stop the analysis there and conclude that staying out under Republican presidents and being in under Democratic presidents is a winning strategy. But the real moral of the story is told with the final bar. The same $10K initially invested in 1961 would have grown to more than $5.1M by just staying invested, without regard for the political party in power.

Stay invested

Source: Schwab Center for Financial Research with data provided by Morningstar, Inc.

The above chart shows what a hypothetical portfolio value would be if an investor invested $10,000 in a portfolio that tracks the Ibbotson U.S. Large Stock Index on 1/1/1961 under three different scenarios. The first two scenarios are what would occur if an investor only invested when one particular party was president. The third scenario is what would occur if an investor had stayed invested throughout the entire period. Returns include reinvestment of dividends and interest. The example is hypothetical and provided for illustrative purposes only. It is not intended to represent a specific investment product. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested indirectly. Past performance is no guarantee of future results.

In sum

This is going to be an emotional year, certainly as it relates to a contentious and unprecedented election, but also uncertainty around inflation and Federal Reserve policy. There is no more important place to keep emotions out of the mix than with regard to investing. This is a time for discipline, as well as trying to assess whether there is a narrow or yawning gap between your financial risk tolerance and your emotional risk tolerance. The psyche of investors can overwhelm rational thinking during periods of stress in the markets, or stress in our own views. Stay the course.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

0324-S2ME

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co., Inc. ("Schwab") (Member SIPC), is registered by the Securities and Exchange Commission ("SEC") in the United States of America and offers investment services and products, including Schwab brokerage accounts, governed by U.S. state law. Schwab is not registered in any other jurisdiction. Neither Schwab nor the products and services it offers may be registered in your jurisdiction. Neither Schwab nor the products and services it offers may be registered in any other jurisdiction. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products. Access to Electronic Services may be limited or unavailable during periods of peak demand, market volatility, systems upgrade, maintenance, or for other reasons.

This site is designed for U.S. residents. Non-U.S. residents are subject to country-specific restrictions. Learn more about our services for non-U.S. residents, Charles Schwab Hong Kong clients, Charles Schwab U.K. clients.

© 2024 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. Unauthorized access is prohibited. Usage will be monitored.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Charles Schwab

Read more commentaries by Charles Schwab