Nobel laureate Harry Markowitz famously asserted that diversification is the only free lunch in investing. His insight was simple yet profound: by diversifying across assets, investors can achieve higher returns without necessarily increasing risk.

We'll use this insight to highlight this month's updates to Asset Allocation Interactive (AAI), where we have a new and improved portfolio builder together with several newly modeled assets. We'll provide a demonstration of these features by building and analyzing a toy portfolio, which, in a nod to Harry Markowitz, we'll playfully dub "Free Lunch."

We caution readers to not interpret the toy portfolio in our example as investment advice (the countries in our example represent only 7% of world GDP!), but rather to demonstrate the essence of Markowitz's renowned insight on diversification.

Introducing AAI's New Assets

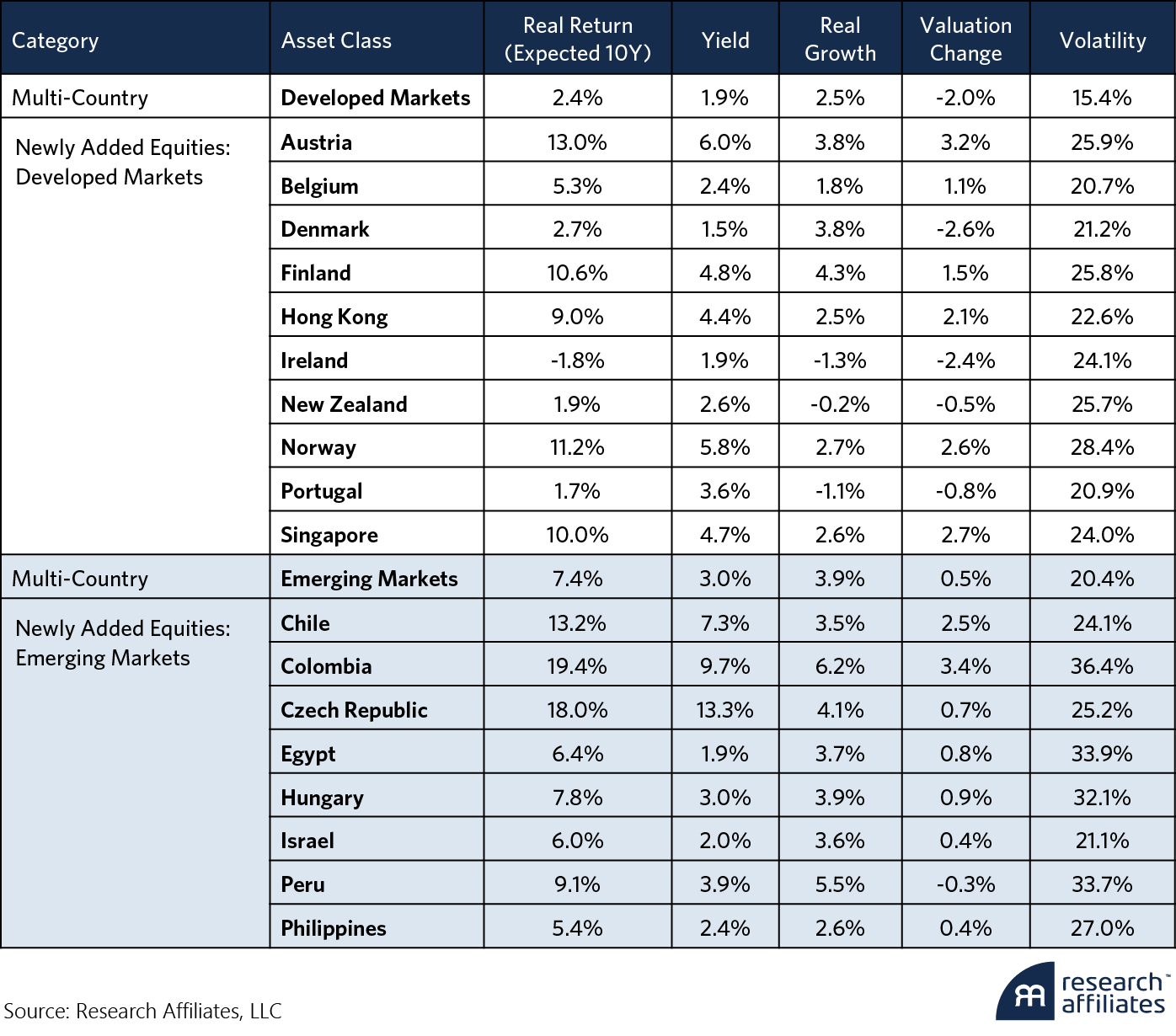

The table below shows the expected returns and volatility for our 18 newly added public equity assets. Notice that in general, the newly added assets, across both developed and emerging markets, show substantially higher levels of risk than their corresponding multi-country market capitalization weighted equity indices. Note also that many of these markets offer double-digit expected returns, with dividend yields over 5%. For example, an investor seeking to capture the 11% expected return from Norway would be subject to 28% volatility, nearly double the 15% volatility of the Developed Markets index.

What happens when we build a new “Free Lunch” portfolio using these assets?

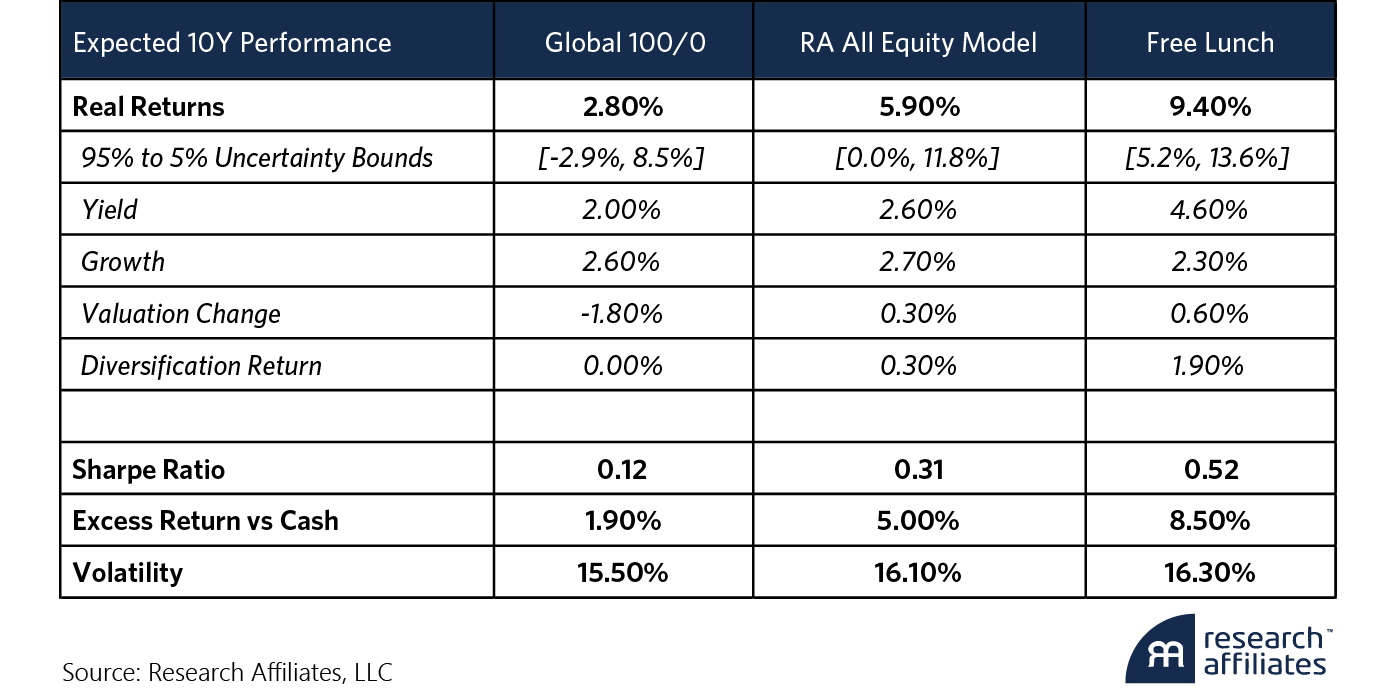

The “Free Lunch” portfolio has an allocation of 5% to each of the 18 new asset equity markets, leaving 10% uninvested as US cash. We compare this new portfolio to Global 100/0 and the RA All Equity Model.

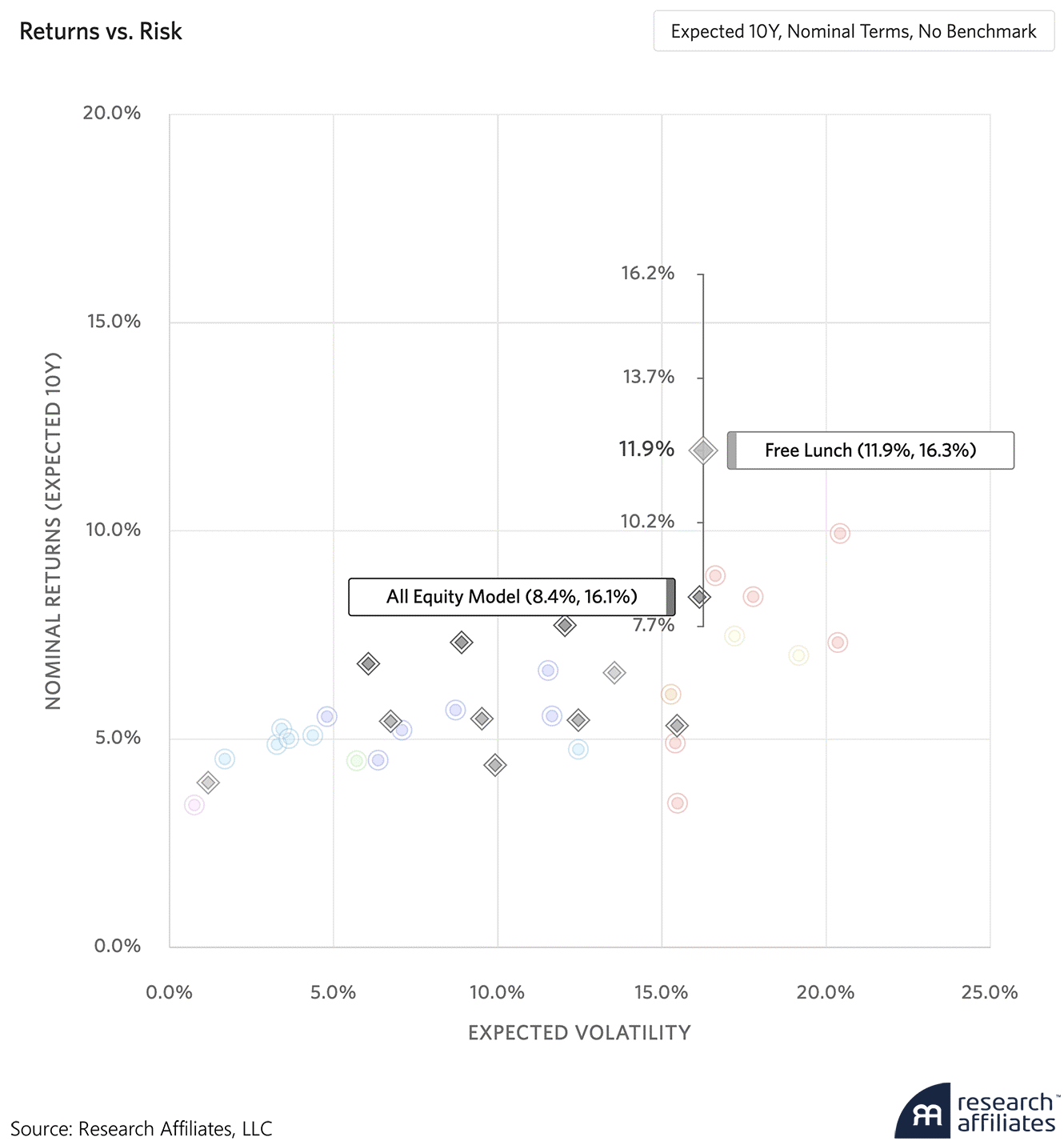

First, even though our Free Lunch portfolio was constructed with highly volatile assets, it has roughly the same 16% volatility as the Global 100/0 and RA All Equity Model portfolios. Why? The new countries have relatively low cross-correlations due to the high degree of idiosyncratic risk. In a broadly diversified portfolio, the idiosyncratic risks are diversified away, leaving a total portfolio volatility largely driven by systematic equity risk.

Second, we see that our Free Lunch portfolio has an expected return that is about 6.5% higher than the Global 100/0, and 3.5% higher than the RA All Equity model. Digging into the drivers of return, we see that in the Free Lunch portfolio, a large portion of the increased return expectation is due to the portfolio's higher Yield and expected Valuation Change. But the Free Lunch portfolio has one additional tailwind to returns relative to the other portfolios: the nearly 2% Diversification Return. This is the rebalancing premium we can harvest by rebalancing a portfolio of highly volatile assets with low correlations.

Takeaway

While the purpose of the exercise was to introduce our new asset classes and portfolio builder, we hope that it also provided an example of Harry Markowitz' key insight. We encourage readers to explore alternative portfolio allocations to see the effects of diversification in their own portfolios. While there are no guarantees in the financial markets, broad diversification and rebalancing can provide us an opportunity to enhance returns while decreasing risk. No wonder Harry Markowitz called it a free lunch!

Please read our disclosures concurrent with this publication: https://www.researchaffiliates.com/legal/disclosures#investment-adviser-disclosure-and-disclaimers.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

© Research Affiliates

Read more commentaries by Research Affiliates